- Table of Contents

- What Is Activity-Based Costing?

- The Benefits of Activity-Based Costing

- Accurate Cost Allocation

- Enhanced Decision-Making

- Product and Service Profitability Analysis

- Resource Optimisation

- Better Pricing Strategies

- Improved Cost Visibility

- Enhanced Resource Efficiency

- Facilitation of Continuous Improvement

- Disadvantages of Activity-Based Costing

- Complex Implementation

- Data Requirements

- Costly Implementation

- Resistance to Change

- Time-Consuming Process

- Potential Overhead

- Activity-Based Costing Process

- 1- Identify Activities

- 2- Assign Resource Costs

- 3- Identify Cost Drivers

- 4- Calculate Activity Costs

- 5- Allocate Costs to Products/Services

- 6- Analyse and Interpret Results

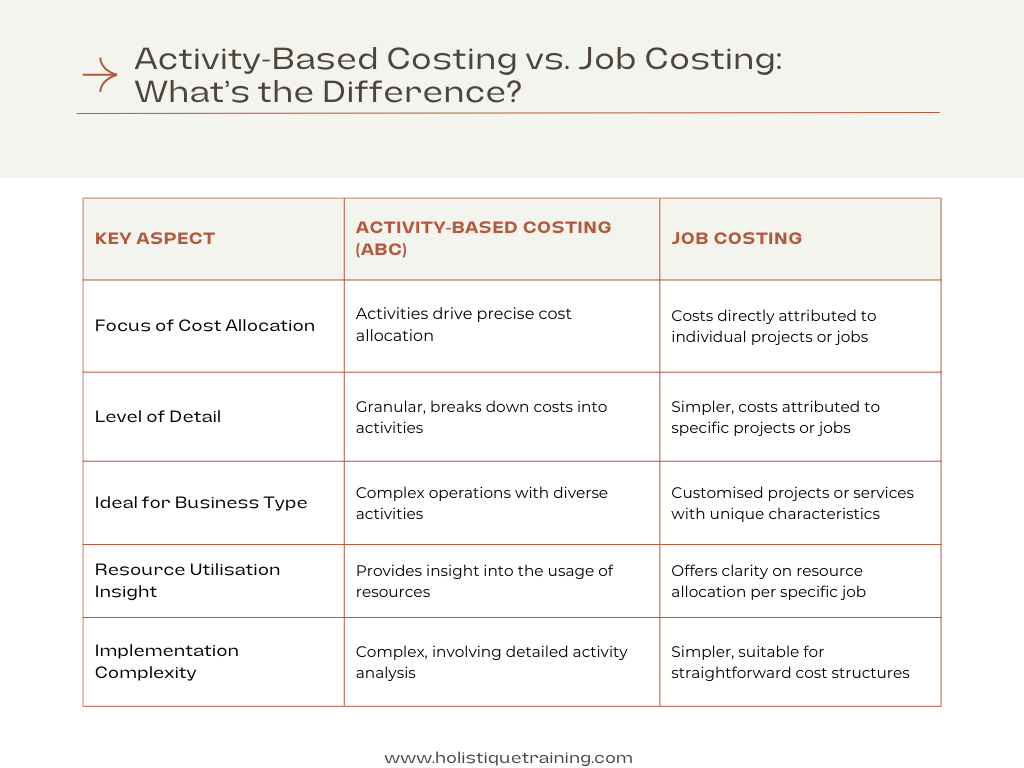

- Activity-Based Costing vs. Job Costing: Unveiling Distinctions and Making Informed Choices

- Activity-Based Costing (ABC): A Holistic Perspective

- Key Features of Activity-Based Costing:

- Job Costing: Tailoring Costs to Specific Jobs

- Key Features of Job Costing:

- Which One Is Better? The Context Matters:

- Conclusion

In the complex world of business, accurate cost allocation is not only a necessity but a strategic advantage. Traditional cost allocation methods often fall short in providing a clear picture of where resources are truly utilised. This is where Activity-Based Costing (ABC) emerges as a game-changer. ABC has gained significant prominence over the years as a dynamic and precise cost allocation methodology that sheds light on hidden cost drivers and enables organisations to make informed decisions. In this comprehensive blog post, we will delve into the intricacies of Activity-Based Costing, exploring its definition, benefits, disadvantages, and the step-by-step process involved.

What Is Activity-Based Costing?

Activity-Based Costing, commonly referred to as ABC, is a sophisticated cost allocation technique that assigns costs to specific activities within an organisation's operations. Unlike traditional costing methods, which often use broad cost pools and distribute expenses based on a single cost driver such as labour hours or machine usage, ABC focuses on identifying and measuring various activities that drive costs. These activities can encompass anything from setting up machinery, processing orders, handling customer inquiries, to quality control processes.

The Benefits of Activity-Based Costing

Accurate Cost Allocation

Activity-Based Costing (ABC) excels in precision when it comes to cost allocation. By identifying numerous cost drivers associated with specific activities, organisations can allocate expenses with a level of accuracy unparalleled by traditional costing methods. This meticulous approach ensures that costs are assigned to products, services, or customers in a way that truly reflects their consumption of various activities. The result is a more equitable distribution of costs, providing decision-makers with a clearer and more realistic understanding of the profitability of different facets of the business.

Enhanced Decision-Making

One of the key advantages of ABC lies in its ability to empower businesses with insightful information about their cost structures. Traditional costing methods often provide a high-level overview of costs without delving into the specifics of how different activities contribute to those costs. ABC, however, unveils a deeper understanding of the nuances involved. Armed with this information, managers can make more informed decisions regarding cost reduction, process improvement, and strategic resource allocation. The detailed insights derived from ABC enable organisations to navigate the complex landscape ofdecision-making with greater confidence.

Product and Service Profitability Analysis

Traditional cost allocation methods may mask the true profitability of products and services, leading to suboptimal decision-making. ABC, on the other hand, allows organisations to drill down into the specific activities and resources associated with each product or service. This level of granularity enables a precise analysis of the profitability of individual offerings. By considering the real costs involved, organisations can identify high-margin products and services, as well as areas that may be contributing less to the bottom line. This clarity is invaluable for strategic planning and resource optimisation.

Resource Optimisation

Identifying activities that consume excessive resources or add little value is a cornerstone of ABC. By shining a spotlight on these activities, organisations can streamline their operations effectively. This streamlining process involves either eliminating non-value-added activities or optimising resource-intensive processes. In doing so, businesses can enhance overall efficiency and ensure that resources are allocated where they generate the most value. This aspect of ABC aligns with the broader goal of continuous improvement, fostering agility in response to evolving market conditions.

Better Pricing Strategies

Accurate cost data derived from ABC becomes a guiding beacon for organisations in setting competitive yet profitablepricing strategies. One of the pitfalls of traditional costing methods is the potential to underprice products or services due to an incomplete understanding of the true costs involved. ABC mitigates this risk by providing a comprehensive view of resource utilisation. Armed with this knowledge, businesses can establish pricing structures that not only remain competitive in the market but also reflect the actual investment of resources. This strategic approach ensures a healthier bottom line and sustainable growth.

Improved Cost Visibility

Activity-Based Costing brings transparency to the often complex web of costs within an organisation. By breaking down costs into specific activities, ABC provides a detailed view of how resources are utilised at every level. This enhanced visibility allows management to identify cost drivers and understand the factors influencing overall costs. Consequently, organisations gain a comprehensive understanding of their cost structure, enabling them to pinpoint areas for improvement and make strategic decisions based on a more nuanced comprehension of their operational expenses.

Enhanced Resource Efficiency

ABC serves as a catalyst for enhancing resource efficiency by honing in on activities that either contribute significantly to costs or fail to add substantial value. Through the identification and analysis of these activities, organisations can reallocate resources more efficiently. This not only streamlines operations but also ensures that resources are deployed in ways that align with strategic objectives. Consequently, ABC contributes to a more agile and adaptable organisational structure, capable of responding swiftly to market dynamics and changing customer demands.

Facilitation of Continuous Improvement

Activity-Based Costing is inherently linked to the concept of continuous improvement. By scrutinising individual activities and their associated costs, organisations are prompted to assess the efficiency and effectiveness of their processes continually. This continuous evaluation fosters a culture of improvement, encouraging teams to find innovative ways to optimise activities, reduce costs, and enhance overall performance. ABC, therefore, acts as a catalyst for a dynamic and proactive approach to organisational development, ensuring that businesses remain resilient and responsive in the face of evolving market conditions.

In essence, the benefits of Activity-Based Costing extend beyond mere cost allocation; they permeate through various aspects of organisational functioning. From strategic decision-making to product profitability analysis and resource optimisation, ABC stands as a multifaceted tool that equips organisations to navigate the intricacies of the business landscape with greater clarity and precision.

Maintaining financial understanding is crucial for any business's success. Executives and other senior positions need to be able to effectively communicate the current state of finances with other employees with financial control. A non-finance manager developing the skillset required to manage

Disadvantages of Activity-Based Costing

While Activity-Based Costing (ABC) offers a nuanced and accurate approach to cost allocation, it is not without its challenges. Implementing ABC requires careful consideration of certain drawbacks that organisations may encounter during the process. Understanding these disadvantages is crucial for organisations contemplating the adoption of ABC, as it allows for strategic planning to mitigate potential hurdles. Here are the disadvantages of Activity-Based Costing:

Complex Implementation

Implementing Activity-Based Costing is a complex endeavour that demands a significant investment of time, effort, and resources. Organisations need to thoroughly understand their processes, identify activities accurately, and measure their costs with precision. The complexity intensifies when dealing with a multitude of activities across diverse operational areas. This intricate process can strain the capabilities of organisations, particularly those with limited resources or less well-defined processes.

Data Requirements

The success of ABC hinges on the availability and accuracy of comprehensive data. Organisations must gather detailed information about activities, resource costs, and cost drivers. However, obtaining this data can be a challenging task, particularly in industries with complex operations or when dealing with intangible activities that are difficult to quantify. Insufficient or unreliable data compromises the accuracy of the ABC model, potentially leading to misguided decisions based on flawed information.

Costly Implementation

The initial costs associated with implementing Activity-Based Costing can be substantial. These costs encompass not only the acquisition of specialised software but also training employees to understand the new methodology and collecting the necessary data. For smaller businesses with limited financial resources, the upfront costs of adopting ABC may be prohibitive. This financial burden can act as a deterrent, limiting the accessibility of ABC to larger enterprises with more substantial budgets.

Resistance to Change

Shifting from traditional costing methods to ABC often necessitates a fundamental change in organisational mindset. Employees and management accustomed to existing systems may resist this change due to the complexities and additional efforts involved. The resistance to change can manifest in various forms, from reluctance to embrace new methodologies to challenges in adapting to the detailed and granular nature of ABC. Overcoming this resistance requires effective change management strategies and clear communication about the long-term benefits of ABC.

Time-Consuming Process

The implementation of ABC is a time-consuming process. From identifying activities to calculating costs and allocating them to products or services, each step demands careful attention. In fast-paced industries where agility is paramount, the time required for ABC implementation may be perceived as a disadvantage. This extended timeline can potentially delay the realisation of benefits and make it challenging for organisations to adapt swiftly to changing market conditions.

Potential Overhead

While ABC is designed to provide a more accurate representation of overhead costs, there is a risk of inadvertently increasingadministrative overhead. The meticulous tracking of numerous activities and cost drivers may necessitate the creation of additional administrative structures to manage the complexity of the ABC system. This added administrative burden could offset some of the efficiency gains expected from the implementation of ABC.

Understanding these disadvantages allows organisations to approach the implementation of Activity-Based Costing with a realistic perspective. By proactively addressing these challenges, businesses can optimise the benefits of ABC while minimising potential drawbacks, ensuring a smoother transition and long-term success in leveraging this sophisticated cost allocation methodology.

Table 1: Metrics to Measure the Effectiveness of Activity-Based Costing

Metrics for ABC Effectiveness | Description | Key Insights |

Cost Allocation Accuracy | Precision in assigning costs to activities. | Reveals accuracy in resource allocation. |

Decision-Making Impact | Improved decisions based on detailed insights. | Indicates the practical value of ABC. |

Resource Utilisation Optimisation | Efficiency gains from streamlined operations. | Reflects the impact on resource efficiency. |

Profitability Analysis Precision | Accuracy in assessing the profitability of products. | Measures the success of ABC in revealing true profitability. |

Process Improvement Impact | Identification and optimisation of resource-intensive activities. | Evaluates the effectiveness in enhancing overall process efficiency. |

Activity-Based Costing Process

1- Identify Activities

The foundation of Activity-Based Costing lies in identifying all activities that contribute to the production of goods or services. These activities can be categorised as either value-added (directly contributing to the final product or service) or non-value-added (necessary for operations but not directly contributing). This initial step requires a thorough understanding of the organisation's processes, from production to customer service, to create a comprehensive list of activities.

2- Assign Resource Costs

Once the activities are identified, the next step is to assign resource costs to each activity. Resources include labour, materials, and overhead. Determining the cost of resources consumed by each activity is essential for accurately assessing the true cost of production. This step often involves a detailed analysis of the time and materials required for each activity.

3- Identify Cost Drivers

For each activity, identifying the cost drivers is crucial. Cost drivers are the factors that cause activities to incur costs. These can include machine hours, number of setups, customer orders, or any other variable that significantly influences the consumption of resources for a particular activity. Choosing appropriate and relevant cost drivers is essential for the accuracy of the subsequent calculations.

4- Calculate Activity Costs

With the cost drivers identified, the next step is to calculate the cost of each activity. This involves multiplying the resource cost per unit by the quantity of the cost driver consumed by that activity. The result is a more accurate reflection of the actual cost of each activity compared to traditional costing methods, which may rely on arbitrary allocations.

5- Allocate Costs to Products/Services

Having determined the cost of each activity, the next stage is to allocate these costs to the products or services that utilise these activities. This step involves determining the extent to which each product or service consumes the various activities. The goal is to attribute costs based on the actual utilisation of resources, offering a more precise understanding of the cost structure associated with each product or service.

6- Analyse and Interpret Results

Once costs are allocated, organisations can analyse the data obtained through ABC to gain valuable insights. This analysis goes beyond traditional costing methods, providing a detailed understanding of cost structures, profitability, and areas for improvement. By comparing results with traditional costing methods, organisations can identify any discrepancies and begin to appreciate the advantages that ABC offers in terms of accuracy and strategic decision-making.

In adopting Activity-Based Costing, organisations must recognise that this process is not a one-time event but rather an ongoing cycle. Continuous monitoring and refinement of the identified activities, cost drivers, and resource costs are essential for maintaining the accuracy and relevance of the ABC model over time.

In short, the Activity-Based Costing process demands a meticulous approach, requiring organisations to delve into the intricacies of their operations to derive meaningful insights. While it may involve a significant initial investment of time and resources, the benefits in terms of accurate cost allocation and improved decision-making position ABC as a valuable tool for organisations seeking a deeper understanding of their cost structures and a strategic edge in the competitive business landscape.

Having accurate and efficient accounting and finance processes, employees, and systems are essential to any business. Without good record upkeep, policies designed to keep track of spending and overheads, and competent employees who are prepared to identify issues and risk areas, your business could fall

Activity-Based Costing vs. Job Costing: Unveiling Distinctions and Making Informed Choices

In the realm of cost accounting, Activity-Based Costing (ABC) and Job Costing are two distinct methodologies that organisations often consider for understanding and allocating costs. Each approach serves unique purposes and caters to different business structures. Here, we'll explore the key differences between Activity-Based Costing and Job Costing, shedding light on their characteristics and when one might be considered more advantageous than the other.

Activity-Based Costing (ABC): A Holistic Perspective

Activity-Based Costing is a comprehensive cost allocation methodology that traces costs to specific activities within an organisation. Unlike traditional costing methods, ABC recognises that not all activities contribute equally to the incurrence of costs. It identifies various activities across different departments, assigns costs to each activity based on the resources consumed, and then allocates these costs to products or services based on the extent of their utilisation of these activities.

Key Features of Activity-Based Costing:

Granular Allocation

ABC breaks down costs into finer categories, providing a more detailed and accurate representation of how resources are utilised.

Focus on Activities

Cost allocation in ABC is centred around various activities, allowing for a more nuanced understanding of cost drivers and their impact on the overall cost structure.

Complex Implementation

ABC demands a detailed analysis of activities, making it a more intricate and time-consuming process compared to simpler costing methods.

Job Costing: Tailoring Costs to Specific Jobs

Job Costing, on the other hand, is a more straightforward method particularly suited for industries where products or services are customised based on specific customer requirements. In Job Costing, costs are assigned to specific jobs or projects, allowing organisations to track the expenses associated with each individual job. This method is commonly employed in construction, custom manufacturing, and service industries where each project has unique characteristics.

Key Features of Job Costing:

Job-Specific Cost Allocation

Costs are directly attributed to individual jobs or projects, providing a clear understanding of the financial implications of each undertaking.

Simplicity

Job Costing is simpler to implement compared to ABC, making it suitable for businesses with straightforward cost structures.

Ideal for Customised Products/Services

Job Costing is particularly effective when dealing with products or services that vary significantly in terms of customer requirements.

Which One Is Better? The Context Matters:

Determining whether Activity-Based Costing or Job Costing is better depends on the nature of the business and the specific information needs of the organisation.

a) For Complex Operations and Diverse Activities

Activity-Based Costing shines in industries where numerous activities contribute to the overall cost structure. It is especially beneficial when there is a need for a detailed breakdown of costs to identify specific areas for improvement and optimisation.

b) For Customised or Unique Projects

Job Costing is preferable when dealing with unique, customised projects. It allows for a straightforward attribution of costs to specific jobs, enabling organisations to understand the profitability of individual projects.

c) Consider a Hybrid Approach

In some cases, organisations might benefit from a hybrid approach, combining elements of both Activity-Based Costing and Job Costing to tailor the methodology to their specific requirements. This approach allows for a nuanced understanding of both activities and job-specific costs.

In short, the choice between Activity-Based Costing and Job Costing depends on the organisation's structure, industry, and specific information needs. While Activity-Based Costing provides a detailed and granular view of costs, Job Costing offers simplicity and direct attribution of costs to individual projects. Ultimately, the best approach is one that aligns with the organisation's goals, operations, and the level of detail required for effective cost management.

Conclusion

In the dynamic landscape of modern business, Activity-Based Costing has emerged as a powerful tool for organisations to gain a more precise understanding of their cost structures. By focusing on activities and their associated costs, ABC provides unparalleled accuracy in cost allocation, leading to better decision-making, optimised resource allocation, and improved profitability analysis. While the complexities and challenges of implementation should not be overlooked, the benefits of Activity-Based Costing make it a valuable addition to the strategic toolkit of any forward-thinking organisation.

Finally, as you strive for precision in cost allocation and strategic decision-making, make sure you check out our course, ‘Accounting Basics for Department Managers.’ Tailored for forward-thinking professionals, this course not only demystifies the complexities of Activity-Based Costing but also equips you with foundational accounting knowledge crucial for effective departmental management. Seize the opportunity to enhance your skills, elevate your financial acumen, and propel your organisation towards sustainable growth. Enrol now and embark on a transformative journey to become a strategic leader in the ever-evolving world of business finance. Your success begins with a click—unlock the doors to financial mastery!

In any department, it’s important to have an overview and understanding of accounting procedures to remain within budget and make important financial decisions. Understanding how your finances can affect wider business performance and change is crucial to staying ahead of the market and remaining competitive.