- Table of Contents

- Introduction

- What Is Financial Ratio Analysis?

- What Are the Different Uses of Financial Ratio Analysis?

- a) Investors

- b) Managers

- c) Creditors and Lenders

- d) Financial Analysts

- Why Is Financial Ratio Analysis Important?

- Assessing Financial Health and Performance

- Informing Strategic Decision-Making

- Facilitating Comparative Analysis and Benchmarking

- Enhancing Transparency and Stakeholder Confidence

- Facilitating Risk Management and Mitigation

- Types of Financial Ratios

- 1) Liquidity Ratios

- 2) Solvency Ratios

- 3) Profitability Ratios

- 4) Efficiency Ratios

- 5) Market Value Ratios

- How to Apply Financial Ratio Analysis

- Step 1: Gather Financial Statements

- Step 2: Calculate Financial Ratios

- Step 3: Interpret Ratio Results

- Step 4: Compare and Benchmark

- Step 5: Draw Conclusions and Recommendations

- An Example of Ratio Analysis

- Limitations of Financial Ratio Analysis

- Limited Scope:

- Industry Variability:

- Accounting Practices:

- Data Integrity:

- Dynamic Nature:

- External Influences:

- Conclusion

Introduction

Understanding a company's financial health is akin to deciphering a complex puzzle. Revenue, expenses, assets, or liabilities contribute to an organisation's stability and growth potential. Financial ratio analysis is the key to unlocking this puzzle, offering investors, managers, and stakeholders valuable insights into a company's performance, liquidity, solvency, and profitability. This comprehensive guide'll delve into the depths of financial ratio analysis, exploring its uses, importance, types, applications, an illustrative example, and inherent limitations.

What Is Financial Ratio Analysis?

Financial ratio analysis is a systematic evaluation of a company's financial performance, conducted by analysing relationships between various financial variables. These ratios serve as quantitative indicators, offering a snapshot of a company's operational efficiency, liquidity, leverage, profitability, and overall financial health. Stakeholders can gauge a company's performance trajectory and make informed decisions by comparing different ratios over time, against industry benchmarks, or with competitors.

What Are the Different Uses of Financial Ratio Analysis?

Financial ratio analysis serves a myriad of purposes across diverse stakeholders:

a) Investors

Financial ratio analysis is a compass for investors in navigating the complex landscape of investment decisions. By dissecting financial statements and scrutinising key ratios, investors gain invaluable insights into a company's financial health, operational efficiency, and growth potential. Here's how investors leverage financial ratios:

Assess Investment Value:

Investors use financial ratios to assess a company's intrinsic value and determine whether it is undervalued, fairly valued, or overvalued in the market.

Evaluate Growth Potential:

By analysing profitability ratios such as return on equity (ROE) and earnings per share (EPS) growth, investors gauge a company's ability to generate sustainable growth and deliver long-term shareholder value.

Mitigate Risk:

Liquidity ratios such as the current and quick ratios help investors evaluate a company's ability to weather economic downturns, manage short-term obligations, and mitigate liquidity risk.

Diversify Portfolio:

Comparative analysis of financial ratios across different industries and sectors enables investors todiversify their investment portfolio , mitigate sector-specific risks, and optimise risk-adjusted returns.

b) Managers

Within organisations, financial ratio analysis is a vital tool for managerial decision-making, performance monitoring, and strategic planning. Managers across departments and functions utilise financial ratios to assess operational efficiency, allocate resources effectively, and drive performance improvements. Here's how managers leverage financial ratios:

Monitor Performance:

Managers use financial ratios to monitor key performance indicators (KPIs), track progress toward organisational goals, and identify variances that require corrective action.

Allocate Resources:

By analysing efficiency ratios such as inventory turnover and asset turnover, managers optimise resource allocation, streamline production processes, and enhance operational efficiency.

Set Benchmarks:

Financial ratios are benchmarks for setting performance targets, establishing budgetary controls, and measuring departmental performance against industry standards and best practices.

Strategic Decision-Making:

Solvency ratios such as the debt-to-equity ratio inform strategic decisions related to capital structure, financing options, and investment priorities, ensuring alignment with long-term organisational objectives.

c) Creditors and Lenders

For creditors and lenders, financial ratio analysis forms the foundation for evaluating creditworthiness, assessing repayment capacity, and mitigating credit risk. Whether extending loans, issuing credit lines, or negotiating lending terms, creditors rely on financial ratios to make informed lending decisions. Here's how creditors and lenders leverage financial ratios:

Evaluate Credit Risk:

Solvency ratios such as the interest coverage ratio and debt ratio help creditors assess a company's ability to service debt obligations, manage financial leverage, and maintain adequate debt coverage ratios.

Determine Loan Terms:

Lenders can evaluate a company's short-term liquidity position by analysing liquidity ratios such as the current and cash ratios, assessing its ability to meet near-term obligations, and structuring loan terms accordingly.

Manage Risk Exposure:

Market value ratios, such as the price-earnings (P/E) ratio and dividend yield, provide insights into a company's market performance, investor sentiment, and risk-adjusted return potential. They enable lenders to manage credit risk and optimise portfolio diversification.

d) Financial Analysts

Financial analysts play a pivotal role in conducting comprehensive financial analyses, forecasting future performance, and providing investment recommendations to clients and stakeholders. Armed with quantitative tools and analytical frameworks, financial analysts leverage financial ratios to uncover underlying trends, identify investment opportunities, and mitigate risk factors. Here's how financial analysts leverage financial ratios:

Conduct Comparative Analysis:

Financial analysts compare financial ratios across companies, industries, and geographic regions to identify relative strengths, weaknesses, and valuation discrepancies.

Forecast Future Performance:

By extrapolating historical trends and projecting future earnings growth, financial analysts use financial ratios to develop financial models, perform sensitivity analyses, and make forward-looking investment projections.

Provide Investment Recommendations:

Financial analysts use financial ratios to formulate investment theses, recommend buy, hold, or sell decisions, and communicate investment insights to clients, portfolio managers, and institutional investors.

Assess Risk Factors:

Financial analysts assess risk factors such as liquidity, credit, and market risk using a combination of financial ratios, qualitative analysis, and scenario planning techniques, enabling investors to make risk-adjusted investment decisions.

In essence, financial ratio analysis transcends traditional boundaries, serving as a universal language that facilitates communication, collaboration, and decision-making across diverse stakeholders. By understanding the multifaceted uses of financial ratios, stakeholders can unlock hidden insights, mitigate risks, and capitalise on opportunities in an ever-evolving global economy.

Why Is Financial Ratio Analysis Important?

Financial ratio analysis stands as a cornerstone in the realm of financial management and decision-making, providing stakeholders with invaluable insights into a company's performance, stability, and growth prospects. Here's why it holds paramount importance in the financial landscape:

Assessing Financial Health and Performance

Financial ratio analysis offers a window into the inner workings of a company's financial health and performance. By scrutinising key ratios derived from financial statements, stakeholders can assess various aspects of a company's operations, including its profitability, liquidity, solvency, and efficiency. This comprehensive assessment enables stakeholders to gauge the company's ability to generate profits, manage resources, and meet financial obligations in both the short and long term.

Informing Strategic Decision-Making

In an increasingly dynamic and competitive business environment, informed decision-making is paramount to organisational success. Financial ratio analysis equips decision-makers with the quantitative tools and insights needed to make strategic choices regarding resource allocation, investment priorities, and capital structure. By identifying trends, patterns, and areas of improvement through ratio analysis, stakeholders can align strategic initiatives with overarching business objectives, mitigate risks, and capitalise on emerging opportunities.

Facilitating Comparative Analysis and Benchmarking

Financial ratio analysis facilitates comparative analysis and benchmarking, enabling stakeholders to contextualise a company's performance relative to industry peers, historical data, and best practices. By benchmarking key ratios against industry standards and competitors' metrics, stakeholders can identify areas of competitive advantage, diagnose performance gaps, and formulate targeted strategies for improvement. This comparative perspective fosters a culture of continuous improvement and drives organisational excellence in an ever-evolving marketplace.

Benchmarking profits, processes, and procedures is a practice widely used in all industries to determine whether growth and change management are heading in the right direction to increase performance, productivity, and, ultimately, the business's success. Benchmarking can happen in various ways, including against

Enhancing Transparency and Stakeholder Confidence

Transparency and accountability are essential pillars of corporate governance and stakeholder trust. Financial ratio analysis promotes transparency by providing stakeholders with objective measures of a company's financial performance and health. Companies foster trust and confidence among investors, creditors, regulators, and other stakeholders by adhering to standardised accounting principles and disclosing relevant financial information. This transparency enhances the credibility of financial reporting and instils confidence in the company's management and governance practices.

Facilitating Risk Management and Mitigation

In today's interconnected and volatile business environment, risk management is critical for organisations across industries. Financial ratio analysis is a powerful risk management tool, enabling stakeholders to identify, assess, and mitigate various financial risks, including liquidity, credit, market, and operational risks. By monitoring key ratios and financial indicators, stakeholders can proactively anticipate potential risks, develop contingency plans, and safeguard the company's financial stability and resilience in the face of adversity.

In summary, financial ratio analysis plays a pivotal role in guiding strategic decision-making, enhancing transparency, and mitigating risks in the complex landscape of corporate finance. By leveraging the insights gleaned from ratio analysis, stakeholders can navigate uncertainty, capitalise on opportunities, and steer their organisations toward sustained growth and success in today's dynamic business environment.

Types of Financial Ratios

Financial ratios are powerful tools for analysing and interpreting a company's financial performance and position. They provide valuable insights into various aspects of a company's operations, liquidity, profitability, solvency, and efficiency. Understanding the different types of financial ratios empowers stakeholders to assess a company's strengths, weaknesses, and overall financial health. Let's explore the key categories of financial ratios:

1) Liquidity Ratios

Liquidity ratios measure a company's ability to meet short-term financial obligations and its overall liquidity position. They assess the company's ability to convert assets into cash to cover liabilities. The primary liquidity ratios include:

Current Ratio: Calculated as current assets divided by current liabilities, the current ratio indicates the company's ability to meet short-term obligations using its current assets.

Quick Ratio: Also known as the acid-test ratio, the quick ratio measures the company's ability to meet short-term obligations using its most liquid assets, excluding inventory.

Cash Ratio: This ratio compares a company's cash and cash equivalents to its current liabilities, providing insights into its ability to cover short-term obligations solely with cash.

2) Solvency Ratios

Solvency ratios evaluate a company's long-term financial stability and its ability to meet long-term debt obligations. They assess the company's leverage and debt management practices. Key solvency ratios include:

Debt-to-Equity Ratio: The debt-to-equity ratio measures the proportion of debt and equity financing the company uses to finance its operations. It helps assess the company's capital structure and financial leverage.

Interest Coverage Ratio: This ratio indicates the company's ability to meet interest payments on its debt obligations. It measures the company's earnings relative to its interest expenses.

Debt Ratio: The debt ratio compares a company's total debt to its total assets, providing insights into the percentage of assets financed by debt.

3) Profitability Ratios

Profitability ratios assess a company's ability to generate profits relative to its revenue, assets, and equity. They measure the efficiency of the company's operations and its ability to generate shareholder returns. Key profitability ratios include:

Gross Profit Margin The gross profit margin measures the percentage of revenue retained by the company after deducting the cost of goods sold. It reflects the company's pricing strategy and cost management practices.

Net Profit Margin: The net profit margin measures the percentage of revenue remaining after deducting all expenses, including taxes and interest. It indicates the company's overall profitability.

Return on Assets (ROA) measures the company's ability to generate profits from its assets. It compares net income to average total assets and reflects the company's asset utilisation efficiency.

Return on Equity (ROE) measures the company's ability to generate profits relative to shareholders' equity. It indicates the return shareholders earn on their investment.

4) Efficiency Ratios

Efficiency ratios evaluate a company's operational efficiency and asset utilisation. They assess how effectively the company manages its resources to generate revenue and profits. Key efficiency ratios include:

Inventory Turnover Ratio: This ratio measures how often a company's inventory is sold and replaced during a specific period, indicating its efficiency in managing inventory levels.

Accounts Receivable Turnover Ratio: The turnover ratio measures how efficiently a company collects customer payments and indicates the effectiveness of its credit and collection policies.

Asset Turnover Ratio: The asset turnover ratio measures how efficiently a company utilises its assets to generate revenue. It compares net sales to average total assets and reflects the company's asset management efficiency.

5) Market Value Ratios

Market value ratios assess a company's market performance and investor sentiment. They help investors evaluate the company's valuation and growth prospects relative to its market price. Key market value ratios include:

Price-Earnings (P/E) Ratio: The price-earnings ratio compares the company's stock price to its earnings per share, indicating investors' expectations of future earnings growth.

Earnings Per Share (EPS): EPS measures the company's profitability on a per-share basis, providing insights into its ability to generate earnings for shareholders.

Dividend Yield: Thedividend yield measures the percentage of dividends paid relative to the company's stock price, indicating the return investors receive through dividends.

Understanding these types of financial ratios enables stakeholders to perform comprehensive financial analysis, identify trends, assess performance relative to industry benchmarks, and make informed investment and managerial decisions. By leveraging the insights provided by financial ratios, stakeholders can navigate the complexities of the financial landscape and drive sustainable growth and value creation for their organisations.

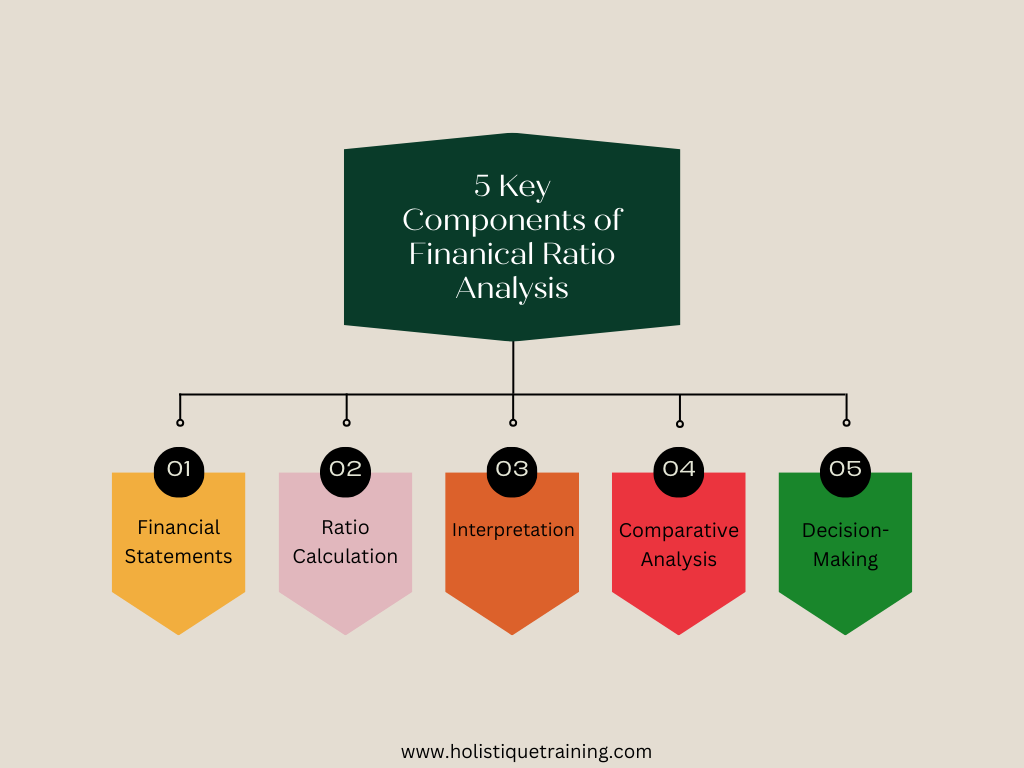

How to Apply Financial Ratio Analysis

Applying financial ratio analysis involves a systematic approach to interpreting and contextualising financial data to derive meaningful insights. Here's how to apply financial ratio analysis effectively:

Step 1: Gather Financial Statements

In the initial step of financial ratio analysis, stakeholders must gather comprehensive financial statements, including the balance sheet, income statement, and cash flow statement. These documents are the foundation for calculating key financial ratios and assessing the company's financial performance. It's crucial to ensure the accuracy and completeness of the financial data to derive reliable insights.

Step 2: Calculate Financial Ratios

Once the financial statements are gathered, stakeholders proceed to calculate a range of financial ratios using relevant data extracted from the statements. Consistency in calculation methods and adherence to accounting standards are essential to ensure the accuracy and comparability of the ratios over time and across companies. Advanced financial analysis tools and software can streamline the calculation process and facilitate dynamic ratio analysis.

Step 3: Interpret Ratio Results

Interpreting financial ratio results requires deeply understanding of the underlying financial dynamics and industry benchmarks. Stakeholders must analyse the computed ratios in the context of the company's operational model, industry trends, and macroeconomic factors. It's essential to identify trends, anomalies, and outliers in the ratio results and assess their implications for the company's financial health and performance.

Step 4: Compare and Benchmark

Comparative analysis and benchmarking are pivotal in financial ratio analysis. They enable stakeholders to contextualise the company's performance relative to industry peers, historical trends, and best practices. By benchmarking key ratios against industry standards and competitors' metrics, stakeholders gain insights into the company's competitive position, identify areas of strength and weakness, and formulate targeted strategies for improvement.

Step 5: Draw Conclusions and Recommendations

Drawing meaningful conclusions from financial ratio analysis requires synthesising quantitative data with qualitative insights and strategic considerations. Stakeholders must weigh the implications of ratio results against broader business objectives, market dynamics, and risk factors. Based on the analysis, stakeholders formulate actionable recommendations for management, investors, and other relevant stakeholders to optimise performance, mitigate risks, and drive sustainable growth.

By following these steps diligently and leveraging the insights derived from financial ratio analysis, stakeholders can understand the company's financial position, identify strategic opportunities and challenges, and make informed decisions that align with organisational goals and stakeholders' interests. Effective application of financial ratio analysis empowers stakeholders to navigate complexities in the financial landscape and unlock value-creation opportunities for the company.

An Example of Ratio Analysis

Consider a hypothetical company, XYZ Inc., engaged in the retail industry. By conducting a financial ratio analysis for XYZ Inc., stakeholders can gain valuable insights into its financial health and performance metrics.

Liquidity Ratio: Current Ratio = Current Assets / Current Liabilities

Solvency Ratio: Debt-to-Equity Ratio = Total Debt / Shareholders' Equity

Profitability Ratio: Net Profit Margin = (Net Income / Revenue) * 100

Efficiency Ratio: Inventory Turnover Ratio = Cost of Goods Sold / Average Inventory

By computing and analysing these ratios for XYZ Inc., stakeholders can assess its liquidity position, leverage levels, profitability margins, and operational efficiency vis-a-vis industry standards and benchmarks.

Metrics | Description |

Accuracy of Predictions | Assessing how closely ratios predict outcomes |

Timeliness of Reporting | Evaluating speed in providing financial data |

Stakeholder Satisfaction | Gauging satisfaction with ratio analysis |

Decision-Making Impact | Measuring influence on strategic decisions |

Ratio Interpretation Ease | Evaluating ease of understanding ratio results |

Table 1: Metrics to Measure the Effectiveness of Financial Ratio Analysis

Limitations of Financial Ratio Analysis

While financial ratio analysis offers valuable insights, it's essential to acknowledge its limitations:

Limited Scope:

While financial ratios provide valuable insights into a company's financial performance, they offer a narrow perspective and may not capture the full complexity of the business environment. Factors such as market dynamics, technological disruptions, regulatory changes, and competitive pressures may not adequately reflect in ratio analysis. Stakeholders must supplement ratio analysis with qualitative assessments and contextual insights to better understand the company's operations and external influences.

Industry Variability:

Financial ratios are subject to industry-specific dynamics and operating models, making establishing universal benchmarks for comparison challenging. Industries vary in terms of capital structure, revenue recognition practices, asset utilisation patterns, and risk profiles, which can distort ratio comparisons across different sectors. Stakeholders must exercise caution when benchmarking ratios and consider industry-specific factors to avoid misinterpretation and misleading conclusions.

Accounting Practices:

Differences in accounting standards, policies, and methods among companies can significantly impact ratio analysis outcomes. Variations in depreciation methods, inventory valuation techniques, revenue recognition criteria, and goodwill impairment assessments may distort ratio calculations and comparisons. To ensure comparability and accuracy, stakeholders must exercise diligence in understanding the accounting principles underlying financial statements and adjust ratio interpretations accordingly.

This Training course is aimed at business professionals who need to understand how finance works. Financial information can provide a clear picture of how to increase profitability, decrease costs, and meet targets in any business. It is very crucial that

Data Integrity:

Financial ratio analysis relies on accurate and reliable financial data to generate meaningful insights. Data inaccuracies, errors, or omissions in financial statements can compromise the validity of ratio analysis results and lead to erroneous conclusions. To mitigate the risk of relying on flawed data for decision-making, stakeholders must conduct due diligence in verifying the integrity and completeness of financial data sources, scrutinising disclosures, and corroborating information from multiple sources.

Dynamic Nature:

Financial ratios reflect a snapshot of a company's financial performance at a specific point in time and may not capture the dynamic nature of business operations and market conditions. Economic fluctuations, industry trends, competitive dynamics, and strategic initiatives can impact ratio results over time, rendering historical comparisons less relevant. Stakeholders must complement ratio analysis with trend analysis, scenario planning, andsensitivity analysis to account for evolving market dynamics and anticipate future performance trends accurately.

External Influences:

Financial ratio analysis may overlook external factors beyond the company's control that could impact its financial performance and market valuation. Macroeconomic factors such as interest rate fluctuations, currency exchange rates, geopolitical events, and regulatory changes can significantly influence business operations and financial outcomes. Stakeholders must incorporate macroeconomic analysis and scenario forecasting into their decision-making process to assess the potential impact of external factors on the company's financial position and risk exposure.

By acknowledging these limitations and adopting a nuanced approach to the ratio analysis, stakeholders can enhance the reliability and relevance of their financial assessments, mitigate risks associated with decision-making, and gain deeper insights into the underlying drivers of business performance. Supplementing ratio analysis with qualitative assessments, scenario analysis, and external market intelligence enables stakeholders to make more informed decisions and effectively navigate uncertainties in the dynamic business environment.

Conclusion

In conclusion, financial ratio analysis is a cornerstone of financial decision-making, offering a systematic framework for evaluating company performance, assessing risk exposure, and driving strategic initiatives. By understanding the nuances of ratio analysis, stakeholders can navigate the complexities of the financial landscape with confidence and clarity, leveraging data-driven insights to propel organisational growth and sustainability.

In your journey toward financial mastery, consider enrolling in our course, ‘Financial Acumen for Non-Finance Experts.’ Designed to empower professionals from various backgrounds, this course goes beyond the basics, providing a hands-on approach to understanding financial ratios, interpreting financial statements, and making informed decisions. Gain practical skills that transcend theory, ensuring you comprehend financial metrics and apply them strategically in your role. Unlock the power of financial acumen, and confidently contribute to your organisation's success. Join now to elevate your financial understanding and amplify your impact in the business world.

Maintaining financial understanding is crucial for any business's success. Executives and other senior positions need to be able to effectively communicate the current state of finances with other employees with financial control. A non-finance manager developing the skillset required to manage