- Table of Contents

- Introduction

- What Is Cash Basis Accounting?

- Pros of Cash Basis Accounting

- 1- Simplicity and Ease of Use

- 2- Immediate Cash Flow Visibility

- 3- Reduced Chances of Errors

- 4- Minimal Record-Keeping Requirements

- Cons of Cash Basis Accounting

- 1- Limited Financial Insight

- 2- Inaccurate Matching of Revenue and Expenses

- 3- Limited Applicability for Growing or Complex Businesses

- 4- Potential Tax Implications

- What Is Accrual Accounting?

- Pros of Accrual Accounting

- 1- Accurate Matching of Revenue and Expenses

- 2- Comprehensive Financial Reporting

- 3- Effective Cash Flow Management

- 4- Compliance with Accounting Standards

- Cons of Accrual Accounting

- 1- Complexity and Expertise Required

- 2- Discrepancy Between Cash Flow and Reported Income

- 3- Possible Overemphasis on Accrual-Based Metrics

- 4- Higher Initial Implementation Costs

- Key Differences Between Cash and Accrual Accounting

- How to Choose Between Cash- and Accrual-Basis Accounting

- 1. Nature and Size of Your Business

- 2. Cash Flow Management

- 3. Complexity of Transactions

- 4. Industry and Regulatory Requirements

- 5. Long-Term Business Goals

- 6. Consultation with Accounting Professionals

- Their Effect on Taxes

- Emerging Trends in Accounting Technology

- 1. Cloud-Based Accounting Software

- 2. Artificial Intelligence (AI) and Machine Learning

- 3. Automation of Repetitive Tasks

- 4. Blockchain Technology

- 5. Data Analytics and Business Intelligence

- 6. Integration of Financial Systems

- 7. Enhanced Cybersecurity Measures

- 8. Mobile Accounting Applications

- Ethical Considerations in Financial Management

- Accurate and Transparent Financial Reporting

- Fair Treatment of Stakeholders

- Compliance with Legal and Regulatory Requirements

- Responsible Resource Allocation

- Prevention of Fraud and Corruption

- Ethical Use of Financial Resources

- Promotion of Sustainability

- Long-Term Relationship Building

- Conclusion

Introduction

Accurate financial management is crucial for any business to thrive. One essential aspect of financial management is choosing the appropriate accounting method. The two primary methods businesses use worldwide are cash-based accounting and accrual accounting. Each method has its own set of advantages and disadvantages, and understanding the key differences between them is essential for making informed financial decisions. In this blog post, we will explore cash basis and accrual accounting concepts, analyse their pros and cons, and discuss their impact on taxes. By the end, you will clearly understand these accounting methods and be better equipped to choose the right one for your business.

What Is Cash Basis Accounting?

Cash basis accounting is a straightforward method that records transactions only when cash is received or paid out. Under this method, revenue is recognised when payment is received, and expenses are recognised when payment is made. Small businesses and individuals commonly use it for its simplicity and ease of use. Cash-based accounting provides an immediate picture of cash flow, focusing solely on the movement of cash in and out of the business.

Pros of Cash Basis Accounting

1- Simplicity and Ease of Use

One of the primary advantages of cash-based accounting is its simplicity. Small businesses and individuals often find this method accessible because it requires minimal accounting knowledge. Transactions are recorded only when cash changes hands, making it easy for entrepreneurs to track their finances without the need for complex accounting procedures or professional assistance.

2- Immediate Cash Flow Visibility

Cash basis accounting provides an immediate snapshot of a business's cash flow. Businesses can readily assess their liquidity by recording transactions when cash is received or paid. This real-time insight enables quick decision-making, helping businesses manage their day-to-day operations more effectively. Entrepreneurs can gauge their financial health and adjust their spending or investment strategies promptly.

3- Reduced Chances of Errors

Due to its straightforward nature, cash-based accounting reduces the likelihood of errors. Since transactions are limited to cash movements, there is less room for confusion or misinterpretation. Small business owners, especially those without a financial background, appreciate this simplicity as it minimises the risk of mistakes in their financial records. Accurate financial data is essential for making informed business decisions, and cash-based accounting provides a reliable way to achieve this.

4- Minimal Record-Keeping Requirements

Cash basis accounting demands minimal record-keeping. Businesses do not need to maintain elaborate ledgers or complex financial statements, as transactions are limited to cash receipts and payments. This reduced paperwork saves entrepreneurs time and effort, allowing them to focus on core business activities. This streamlined approach to record-keeping is a significant advantage for small enterprises with limited resources, enabling them to allocate their time and resources more efficiently.

Cons of Cash Basis Accounting

1- Limited Financial Insight

One of the significant drawbacks of cash-basis accounting is its limited ability to provide a comprehensive financial overview. Since it only accounts for cash transactions, it may not accurately reflect a company's financial position. Businesses might have significant outstanding invoices (accounts receivable) or pending bills (accounts payable) that are not considered in cash-basis accounting. This limitation can lead to a distorted view of the company's overall financial health, making it challenging to plan for long-term growth or assess its true profitability.

2- Inaccurate Matching of Revenue and Expenses

Cash-based accounting does not match revenue with the corresponding expenses, leading to inaccurate financial statements. For instance, a business might make a substantial sale. Still, if the payment is received in the following accounting period, the profit will not be reflected in the current financial statement. Similarly, if a business incurs an expense but delays the payment to the next period, it will not be deducted from the current revenue. This mismatch can create misleading financial reports, hindering accurate performance evaluation and strategic decision-making.

3- Limited Applicability for Growing or Complex Businesses

Businesses often outgrow cash basis accounting as they expand. Complex operations, increased transactions, and the need for more detailed financial reporting make this method impractical for larger enterprises. As businesses evolve, they require a more sophisticated accounting approach that accurately represents their financial complexities. With its limitations in handling intricate financial structures, cash basis accounting becomes inadequate for businesses aiming for significant growth or dealing with diverse revenue streams.

4- Potential Tax Implications

While cash-based accounting can provide tax advantages by allowing businesses to time their cash flows strategically, it can also create challenges. In some jurisdictions, certain businesses must use accrual accounting for tax reporting, irrespective of their chosen accounting method for internal purposes. This disconnect between internal financial management and tax reporting can lead to complications and require adjustments, consuming additional time and resources to accurately comply with tax regulations.

By understanding both the pros and cons of cash-basis accounting, businesses can make informed decisions about their financial management strategies. They can weigh the simplicity and immediate cash flow visibility against the limitations in financial insight and accuracy.

What Is Accrual Accounting?

Accrual accounting captures business revenue and corresponding expenses when they are incurred, irrespective of the timing of cash transactions, according to NetSuite. This method provides a more comprehensive and accurate representation of a company's financial position by considering all economic activities during a given period.

Under accrual accounting, revenue is recorded when it is earned, typically when goods are delivered or services are provided, regardless of when the payment is received. Similarly, expenses are recognised when they are incurred, even if payment is not immediately made. This approach provides a more realistic view of a business's profitability and financial health.

Pros of Accrual Accounting

1- Accurate Matching of Revenue and Expenses

One of accrual accounting's primary advantages is its ability to accurately match revenue with corresponding expenses. Accrual accounting provides a more realistic view of a company's profitability by recognising revenue when it is earned and expenses when they are incurred. This matching principle allows businesses to assess their true financial performance, enabling better decision-making and strategic planning.

2- Comprehensive Financial Reporting

Accrual accounting offers a comprehensive view of a business's financial position. It considers all economic activities, including accounts receivable and accounts payable, and provides a detailed picture of the company's financial obligations and resources. This in-depth analysis aids businesses in evaluating their liquidity, managing outstanding debts, and understanding their overall financial health. Investors and stakeholders often rely on accrual-based financial statements to assess a company's value and stability accurately.

3- Effective Cash Flow Management

Accrual accounting allows businesses to track accounts receivable and accounts payable, facilitating better cash flow management. By understanding the timing of expected payments and expenses, businesses can optimise their cash reserves, ensuring they have enough liquidity to cover their operational needs. This proactive approach to cash flow management is crucial for the sustainability and growth of businesses, especially during periods of economic uncertainty.

4- Compliance with Accounting Standards

Accrual accounting aligns with generally accepted accounting principles (GAAP) and international financial reporting standards (IFRS). Adhering to these standards enhances the credibility and reliability of a company's financial statements. Compliance with accounting standards is essential for businesses seeking external funding, as lenders, investors, and regulatory authorities often require financial reports prepared using accrual accounting methods. Accrual-based financial statements provide a solid foundation for transparent and trustworthy financial reporting.

Cons of Accrual Accounting

1- Complexity and Expertise Required

Accrual accounting is more complex than cash-based accounting and requires more accounting expertise. Businesses using accrual accounting need professionals who understand intricate accounting principles, adjusting entries, and financial statement preparation. This complexity may necessitate hiring skilled accountants or investing in specialised accounting software, increasing operational costs for businesses, particularly smaller enterprises with limited resources.

2- Discrepancy Between Cash Flow and Reported Income

One of the challenges of accrual accounting is the potential discrepancy between cash flow and reported income. Businesses may recognise revenue when they generate sales but face payment delays. Similarly, expenses incurred might not align with the timing of cash outflows. This mismatch can create confusion, making it challenging to accurately evaluate a company's cash position. Businesses must carefully manage this disparity to avoid cash flow issues despite reported profitability.

3- Possible Overemphasis on Accrual-Based Metrics

In accrual accounting, certain financial metrics, such as revenue and profit, can be influenced by accounting policies and estimates. While these metrics are essential for assessing a company's performance, relying solely on accrual-based numbers might lead to overemphasising short-term financial goals. Businesses should balance accrual-based metrics and operational realities to make decisions supporting their long-term sustainability and growth.

4- Higher Initial Implementation Costs

Transitioning from a cash basis to accrual accounting can incur higher initial implementation costs. Businesses need to invest in training employees, adopting new accounting software, and potentially hiring external experts to ensure a smooth transition. These upfront expenses can be a significant burden for small businesses with limited budgets, impacting their ability to invest in other essential areas of their operations.

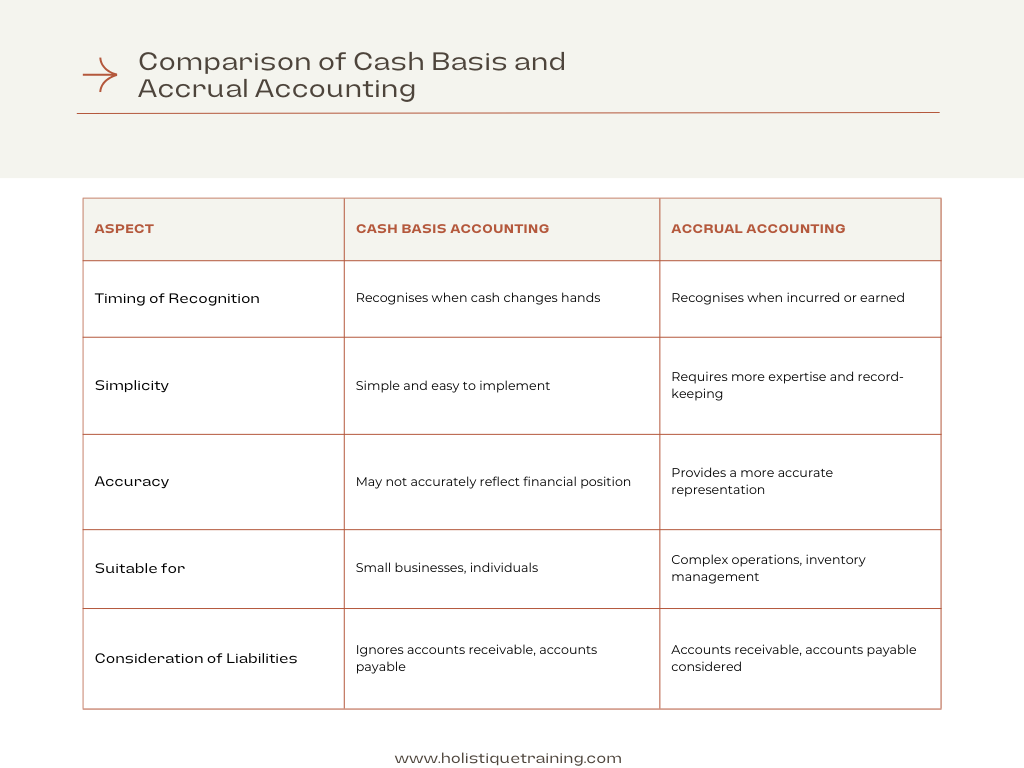

Key Differences Between Cash and Accrual Accounting

While cash-basis accounting and accrual accounting have their respective merits, they differ in fundamental ways. The key differences between the two methods lie in when revenue and expenses are recognised and the focus on cash flow versus comprehensive financial reporting.

Cash-basis accounting recognises revenue and expenses only when cash is received or paid, while accrual accounting records them when they are earned or incurred. This difference means that cash-basis accounting may not accurately represent a company's financial health, particularly in cases where transactions occur well before or after cash changes hands.

Accrual accounting, on the other hand, considers revenue and expenses regardless of cash movements. This method provides a more comprehensive view of a business's financial position by matching revenue with associated expenses, allowing for a better evaluation of profitability and performance. Accrual accounting also accounts for accounts receivable, accounts payable, and other outstanding liabilities, offering a more accurate representation of a company's financial obligations.

How to Choose Between Cash- and Accrual-Basis Accounting

Choosing between cash-basis and accrual-basis accounting methods is a critical decision for businesses, and several factors should be considered to make an informed choice.

1. Nature and Size of Your Business

Consider the nature of your business operations and its size. Cash-based accounting is often suitable for small businesses, sole proprietors, and freelancers. Cash-based accounting provides a simple and efficient way to manage finances if your business has straightforward revenue and expense structures and minimal inventory. On the other hand, accrual accounting is better suited for larger businesses with complex operations, multiple revenue streams, inventory management, and significant accounts receivable and accounts payable. Larger businesses benefit from accrual accounting's ability to provide a more comprehensive and accurate financial overview.

2. Cash Flow Management

Evaluate your business's cash flow patterns. Cash-based accounting might be a preferred choice if your business relies heavily on managing cash flow. This method allows businesses to track cash movements in real time, making it easier to assess liquidity and make immediate financial decisions. Accrual accounting, while providing a more accurate long-term view of financial health, may not offer the same level of immediacy in cash flow analysis. Cash-based accounting might be the more practical option if effective cash flow management is crucial for your business.

3. Complexity of Transactions

Consider the complexity of your business transactions. Cash-based accounting works well for businesses with straightforward, immediate transactions. If your business deals with numerous credit transactions, delayed payments, or long-term contracts, accrual accounting ensures that revenue and expenses are recognised when they occur, regardless of when cash exchanges hands. Accrual accounting captures the nuances of intricate financial transactions, providing a more detailed and accurate representation of your business's financial position.

4. Industry and Regulatory Requirements

Examine industry standards and regulatory requirements in your sector. Certain industries or jurisdictions mandate the use of accrual accounting for financial reporting or tax purposes. Compliance with these regulations is non-negotiable if your business operates in such an industry or region. Failure to adhere to industry-specific accounting standards can result in legal repercussions or loss of credibility. Understanding your industry's specific requirements is crucial in choosing the appropriate accounting method.

5. Long-Term Business Goals

Consider your long-term business goals. Accrual accounting provides a more comprehensive view of your business's financial performance over time. If your goal is to attract investors, secure loans, or expand your business, accrual accounting offers transparent and detailed financial statements that potential investors and lenders often require. Accurate financial reporting enhances your business's credibility and fosters stakeholder trust, facilitating long-term growth and stability.

6. Consultation with Accounting Professionals

When in doubt, seek advice from accounting professionals. Certified accountants have the expertise to assess your business's specific needs and recommend the most suitable accounting method. They can analyse your financial requirements, industry regulations, and growth objectives to guide you in making an informed decision. Investing in professional advice ensures that your chosen accounting method aligns seamlessly with your business goals and compliance obligations.

In short, the choice between cash-basis and accrual-basis accounting methods is not one-size-fits-all. Careful consideration of your business's size, complexity, cash flow patterns, industry requirements, long-term goals, and professional advice is essential. By weighing these factors thoughtfully, you can select the accounting method that best serves your business's financial management needs, paving the way for accurate record-keeping, strategic decision-making, and sustainable growth.

Their Effect on Taxes

The choice of accounting method can have significant implications for tax reporting. In many countries, tax authorities allow small businesses to use cash-based accounting for tax purposes, as it aligns with their simplicity and ease of implementation. However, larger businesses often must use accrual accounting to report their taxable income.

Aspect | Cash Basis Accounting | Accrual Accounting |

Small Business Taxes | Often allowed for tax reporting | Larger businesses may be required to use |

Tax Advantage | Can reduce taxable income by timing cash flows | Provides a more accurate representation of financial performance |

Complexity | Simplicity in tax calculations | May require more complex tax accounting |

Table 1: Tax implications of cash basis and accrual accounting

Cash-based accounting can offer certain tax advantages, particularly when cash flows do not align with revenue recognition. By delaying the receipt of payments or accelerating expenses, businesses can potentially reduce their taxable income in a given year. Accrual accounting, on the other hand, provides a more accurate representation of a company's financial acumen and performance and is generally required for tax reporting purposes for larger businesses.

Maintaining financial understanding is crucial for any business's success. Executives and other senior positions need to be able to effectively communicate the current state of finances with other employees with financial control. A non-finance manager developing the skillset required to manage

Emerging Trends in Accounting Technology

Advancements in technology have revolutionised the field of accounting, transforming traditional financial practices into streamlined, efficient, and data-driven processes. These emerging trends in accounting technology have reshaped how businesses manage their finances, enhancing accuracy, security, and overall productivity.

1. Cloud-Based Accounting Software

Cloud-based accounting software has become a game-changer for businesses of all sizes. By moving accounting operations to the cloud, businesses can access real-time financial data from anywhere, anytime. This accessibility fosters collaboration among team members and enables stakeholders to make data-driven decisions on the go. Cloud-based platforms also offer automatic updates and backups, ensuring that businesses always have access to the latest features and that their data remains secure.

2. Artificial Intelligence (AI) and Machine Learning

Artificial Intelligence and Machine Learning technologies have introduced predictive analytics and data-driven insights to accounting. AI algorithms can analyse vast datasets, identify patterns, and generate forecasts. In the context of accounting, AI can automate mundane tasks, such as data entry and reconciliation, reducing the risk of human error. Machine Learning algorithms can also flag anomalies in financial transactions, helping businesses detect fraudulent activities and ensuring compliance with regulatory standards.

In the modern world, artificial intelligence and machine learning systems have taken over and become necessary features in almost all industries, regardless of sector. This is especially true for the financial sector, as artificial intelligence is perfectly designed to gather and process financial data.

3. Automation of Repetitive Tasks

Automation technologies have significantly reduced the time and effort spent on repetitive accounting tasks. Robotic Process Automation (RPA) software can handle tasks like invoice processing, payroll management, and expense reporting quickly and accurately. By automating these routine activities, businesses can free up their workforce to focus on more strategic and value-added tasks, improving overall productivity and efficiency.

4. Blockchain Technology

Blockchain technology has gained prominence in accounting for its ability to enhance transparency and security in financial transactions. Blockchain creates an immutable digital ledger of transactions, ensuring that it cannot be altered retroactively once a record is added. This feature is particularly beneficial in auditing, where a secure and unchangeable record of financial transactions is essential. Blockchain technology also facilitates faster, secure, and cost-effective cross-border transactions, reducing the reliance on traditional banking systems.

5. Data Analytics and Business Intelligence

Data analytics tools enable businesses to gain valuable insights from their financial data. These tools can process large datasets, identify trends, and provide actionable insights for strategic decision-making. By understanding customer behaviours, market trends, and financial patterns, businesses can make informed choices that optimise their operations and enhance profitability. Business Intelligence (BI) dashboards consolidate complex financial information into visually appealing, easy-to-understand formats, empowering stakeholders to monitor key performance indicators (KPIs) and track the business's overall financial health in real-time.

6. Integration of Financial Systems

Integration of financial systems has become crucial for businesses with diverse software applications. Modern accounting technology allows seamless integration between accounting software, Customer Relationship Management (CRM) systems, inventory management software, and other enterprise solutions. This integration ensures that financial data flows seamlessly across various departments, eliminating data silos and promoting accurate, consistent, and real-time information sharing. Integrated systems enhance collaboration among departments, leading to more efficient decision-making processes.

7. Enhanced Cybersecurity Measures

Cybersecurity has become a top priority in accounting technology with the increasing reliance on digital platforms. Businesses now invest in advanced cybersecurity measures, including multi-factor authentication, encryption, and secure cloud storage solutions. Regular security audits and compliance checks help businesses safeguard sensitive financial data from cyber threats, ensuring client confidentiality and regulatory compliance.

8. Mobile Accounting Applications

Mobile accounting applications have empowered business owners and finance professionals to manage their finances on smartphones and tablets. These applications offer features such as expense tracking, invoicing, and financial reporting, all accessible through user-friendly interfaces. Mobile accounting apps provide flexibility and convenience, allowing users to monitor their financial transactions, approve invoices, and make critical financial decisions, regardless of their location.

Ethical Considerations in Financial Management

Ethical considerations in financial management play a pivotal role in shaping a business's reputation, fostering trust among stakeholders, and ensuring long-term sustainability. Businesses are entrusted with managing resources, financial transactions, and sensitive information, making ethical financial practices essential for maintaining integrity and credibility. Here are some key aspects of ethical considerations in financial management:

Accurate and Transparent Financial Reporting

Ethical financial management begins with accurate and transparent financial reporting. Businesses must provide stakeholders, including investors, employees, and regulators, with truthful and reliable financial performance and position information. Misleading or falsified financial statements breach ethical standards and can lead to legal consequences and damage the organisation's reputation.

Fair Treatment of Stakeholders

Ethical financial management involves fair treatment of all stakeholders, including customers, employees, suppliers, and investors. Businesses should uphold fair payment practices, ensuring suppliers are paid on time, and employees are compensated fairly. Transparent communication with stakeholders regarding financial matters, such as profit distribution and investment opportunities, fosters trust and strengthens relationships.

Compliance with Legal and Regulatory Requirements

Adhering to legal and regulatory requirements is a fundamental ethical obligation. Businesses must comply with financial laws, taxation regulations, and accounting standards specific to their industry and jurisdiction. Failure to comply undermines ethical standards and exposes the business to financial penalties and reputational damage. Regular audits and assessments are essential to ensure ongoing compliance.

Responsible Resource Allocation

Ethical financial management involves responsible resource allocation, both financial and non-financial. Businesses should prioritise investments that align with their values, contribute positively to society, and promote sustainability. Responsible resource allocation includes environmental impact, social responsibility, and ethical sourcing of materials. By integrating these factors into financial decision-making, businesses can create a positive societal impact while maintaining financial integrity.

Prevention of Fraud and Corruption

Ethical financial management requires robust measures to prevent fraud and corruption. Businesses should implement internal controls, segregation of duties, and regular audits to detect and prevent fraudulent activities. Whistleblower policies and anonymous reporting mechanisms create a culture where employees feel safe reporting unethical behaviour, fostering a transparent and accountable work environment.

Embark on a journey into Administrative Accounting, a pivotal realm in financial management. Explore its significance, roles, and the path to a rewarding career. From strategic decision-making to career growth, discover the value Administrative Accountants bring to organisational success.

Ethical Use of Financial Resources

Businesses have a responsibility to use financial resources ethically and responsibly. Excessive executive compensation, wasteful spending, and unnecessary extravagance can raise ethical concerns, particularly when these actions negatively impact stakeholders. Ethical financial management involves prudent spending, ensuring that financial resources are utilised efficiently and benefitting the organisation and its stakeholders.

Promotion of Sustainability

Ethical financial practices extend to promoting sustainability in business operations. This includes adopting environmentally friendly practices, minimising waste, and reducing the carbon footprint. Businesses can invest in renewable energy, eco-friendly technologies, and sustainable supply chain practices. Ethical financial management embraces the concept of triple-bottom-line accounting, where financial, social, and environmental impacts are considered equally important in decision-making processes.

Long-Term Relationship Building

Ethical financial management fosters long-term relationships with stakeholders. Businesses prioritising ethical practices build trust with customers, investors, and partners. Ethical behaviour enhances the organisation's reputation, attracting ethical investors and customers who value responsible business practices. Long-term relationships based on trust are essential for business growth and stability.

In summary, ethical considerations in financial management are integral to the success and sustainability of any business. By upholding principles of accuracy, transparency, fairness, compliance, responsible resource allocation, fraud prevention, ethical use of financial resources, sustainability, and relationship building, businesses can positively impact society while maintaining financial integrity. Ethical financial practices not only strengthen the organisation's reputation but also contribute to the overall stability and trustworthiness of the financial industry, promoting a healthier and more responsible business environment.

Conclusion

In summary, cash-based accounting and accrual accounting are two distinct methods of recording financial transactions. While cash-based accounting provides simplicity and immediate visibility of cash flow, accrual accounting offers a more accurate picture of a business's financial position by matching revenue with expenses and considering accounts receivable and accounts payable. The choice between the two methods depends on the nature and size of the business, as well as its reporting and tax requirements. By understanding the concepts, pros and cons, and differences between cash basis and accrual accounting, business owners can make informed decisions supporting their financial management goals.

Elevate your financial acumen and propel your career to new heights with our cutting-edge MBA Accounting and Finance course. Gain expert insights, refine your decision-making skills, and become a financial maestro, equipped to navigate the complexities of both cash basis and accrual accounting. Enrol now to unlock a world of opportunities and transform your passion for finance into a powerful catalyst for success!

Having accurate and efficient accounting and finance processes, employees, and systems are essential to any business. Without good record upkeep, policies designed to keep track of spending and overheads, and competent employees who are prepared to identify issues and risk areas, your business could fall