يُعتبر العرض والطلب من المبادئ الأساسية في علم الاقتصاد، حيث يشكلان معًا المحرك الرئيسي لأسواق السلع والخدمات. يعتمد العرض والطلب على عوامل متعددة تؤثر في تحديد الأسعار وحجم الإنتاج والشراء، وهو ما يجعل فهم هذين المفهومين ضروريًا لفهم حركة الأسواق. سواء كنت مستهلكًا أو منتجًا، فإن العرض والطلب يؤثران على قراراتك اليومية، بدءًا من الأسعار التي تدفعها إلى الكميات التي تستهلكها. في هذا المقال، سنستعرض مفهوم العرض والطلب بشكل مُفصّل، بالإضافة إلى العوامل المؤثرة عليهما وكيفية تأثير تلك العوامل على الاقتصاد .

ما هي محددات الطلب؟

الطلب يعني ببساطة رغبة المستهلك في شراء السلع والخدمات دون تردد ودفع ثمنها. وبكلمات بسيطة، الطلب هو عدد السلع التي يكون العملاء على استعداد لشرائها بأسعار مختلفة خلال إطار زمني معين. التفضيلات والاختيارات هي أساسيات الطلب، ويمكن وصفها من حيث التكلفة والفوائد والربح والمتغيرات الأخرى.

تعتمد كمية السلع التي يختارها العملاء بشكل متواضع على تكلفة السلعة وتكلفة السلع الأخرى ومكاسب العميل وأذواقه وميوله. كمية السلعة التي يكون العميل مستعدًا لشرائها، وقادرًا على إدارتها وتحملها بأسعار السلع المحددة، وأذواق العميل وتفضيلاته تُعرف بالطلب على السلعة.

منحنى الطلب هو رسم بياني للعلاقة بين سعر السلعة أو الخدمة والعدد المطلوب لفترة زمنية معينة. في الرسم النموذجي، ستظهر التكلفة على المحور الرأسي الأيسر. العدد (الكمية) المطلوبة على المحور الأفقي يُعرف بمنحنى الطلب.

ما هي الامور التي تؤثر على مستوى الطلب؟

هناك العديد من محددات الطلب، ولكن أهم خمسة محددات للطلب هي كما يلي:

- تكلفة المنتج: يتغير الطلب على المنتج وفقًا للتغير في سعر السلعة. يظل الأشخاص الذين يقررون شراء منتج ثابتًا فقط إذا ظلت جميع العوامل المتعلقة به دون تغيير.

- دخل المستهلكين: عندما يزيد الدخل، يزداد أيضًا عدد السلع المطلوبة. وبالمثل، إذا انخفض الدخل، ينخفض الطلب أيضًا.

- تكاليف السلع والخدمات ذات الصلة: بالنسبة لمنتج مكمل، فإن الزيادة في تكلفة سلعة واحدة ستؤدي إلى تقليل الطلب على منتج مكمل. مثال: ستؤدي الزيادة في سعر الخبز إلى تقليل الطلب على الزبدة. وبالمثل، فإن الزيادة في سعر سلعة واحدة ستولد زيادة الطلب على منتج بديل. مثال: ستؤدي الزيادة في تكلفة الشاي إلى زيادة الطلب على القهوة وبالتالي، تقليل الطلب على الشاي.

- توقعات المستهلك: تؤدي التوقعات العالية للدخل أو التوقعات بزيادة سعر السلعة أيضًا إلى زيادة الطلب. وبالمثل، فإن انخفاض توقعات الدخل أو انخفاض أسعار السلع من شأنه أن يقلل الطلب.

- المشترون في السوق: إذا كان عدد المشترين لسلعة ما أكثر أو أقل، فسيكون هناك تحول في الطلب.

ما هي أنواع الطلب؟

هناك بعض الأنواع المختلفة الهامة للطلب وهي كما يلي:

- الطلب على السعر: يشير إلى أنواع مختلفة من كميات السلع أو الخدمات التي سيشتريها العميل بسعر محدد وفي وقت معين، مع الأخذ في الاعتبار ثبات الأشياء الأخرى.

- الطلب على الدخل: يشير إلى أنواع مختلفة من كميات السلع أو الخدمات التي سيشتريها العميل في مراحل مختلفة من الدخل، مع الأخذ في الاعتبار ثبات الأشياء الأخرى.

- الطلب المتقاطع: وهذا يعني أن الطلب على المنتج لا يعتمد على تكلفته الخاصة ولكنه يعتمد على تكلفة السلع الأخرى ذات الصلة.

- الطلب المباشر: عندما تلبي السلع أو الخدمات رغبات الفرد بشكل مباشر، يُعرف ذلك بالطلب المباشر.

- الطلب المشتق أو الطلب غير المباشر: تُعرف السلع أو الخدمات المطلوبة أو اللازمة لتصنيع السلع وإرضاء المستهلك بشكل غير مباشر بالطلب المشتق.

- الطلب المشترك: لإنتاج منتج، هناك العديد من الأشياء المرتبطة ببعضها البعض، على سبيل المثال، لإنتاج الخبز، نحتاج إلى خدمات مثل الفرن والوقود ومطحنة الدقيق والمزيد. لذا، يُعرف الطلب على أشياء إضافية أخرى لإنتاج منتج بالطلب المشترك.

- الطلب المركب: يمكن وصف الطلب المركب عندما يتم استخدام السلع والخدمات لأكثر من سبب واحد. مثال: الفحم

ما هو قانون الطلب؟

قانون الطلب هو مفهوم اقتصادي يوضح العلاقة العكسية بين سعر السلعة والكمية المطلوبة منها، حيث ينص القانون على أنه عندما يرتفع سعر السلعة، تنخفض الكمية المطلوبة منها، وعندما ينخفض السعر، تزداد الكمية المطلوبة، بشرط ثبات جميع العوامل الأخرى المؤثرة على الطلب مثل دخل المستهلكين وتفضيلاتهم. الفكرة الأساسية وراء هذا القانون هي أن المستهلكين يتصرفون بشكل عقلاني؛ أي أنهم يسعون للحصول على أكبر قيمة مقابل أقل تكلفة.

مثال على ذلك هو الطلب على التفاح: إذا كان سعر التفاح مرتفعاً (على سبيل المثال، 3 دولارات لكل كيلوغرام)، فإن المستهلكين قد يشترون كمية أقل من التفاح. ولكن إذا انخفض السعر إلى 1 دولار لكل كيلوغرام، فإنهم سيشترون المزيد من التفاح لأنهم يرونه فرصة للحصول على قيمة أكبر مقابل أموالهم. يعكس هذا المثال سلوك المستهلكين في السوق وكيف يتفاعلون مع تغيرات الأسعار بشكل عام.

يتأثر الطلب بعدة عوامل أخرى إلى جانب السعر، مثل دخل الأفراد، تفضيلاتهم، أسعار السلع البديلة والمكملة، وكذلك توقعاتهم المستقبلية.

ما هو تعريف محددات العرض؟

هي العوامل التي تؤثر على كمية السلع أو الخدمات التي يكون المنتجون على استعداد لتقديمها في السوق عند مختلف المستويات السعرية. هذه العوامل تلعب دورًا رئيسيًا في تحديد الكمية المعروضة، بغض النظر عن سعر السلعة

ما هي الامور التي تؤثر على العرض؟

محددات العرض هي العوامل التي تؤثر بشكل مباشر على كمية السلع أو الخدمات التي يمكن أن يقدمها المنتجون في السوق. هذه المحددات تؤثر على قرارات الشركات والمنتجين في تحديد الكمية التي يمكنهم تقديمها بناءً على الظروف الاقتصادية والتجارية. هذه أبرز محددات العرض بالتفصيل:

1. تكاليف الإنتاج:

تعتبر تكاليف الإنتاج من أهم محددات العرض. عندما ترتفع تكاليف المواد الخام، الأجور، أو تكاليف النقل، يقل عرض المنتجين لأنهم يصبحون أقل قدرة على تقديم السلع بنفس الكميات عند الأسعار السابقة. على سبيل المثال، إذا ارتفع سعر الحديد، فإن الشركات المصنعة للسيارات قد تقلل من إنتاجها أو ترفع الأسعار لتعويض التكاليف.

2. التكنولوجيا:

التطورات التكنولوجية تحسن كفاءة الإنتاج، مما يؤدي إلى زيادة العرض. التكنولوجيا الحديثة تسمح للمنتجين بإنتاج المزيد من السلع بنفس الموارد أو بتكلفة أقل. على سبيل المثال، استخدام الروبوتات في التصنيع يمكن أن يزيد الإنتاج ويقلل تكاليف العمالة، مما يؤدي إلى زيادة العرض.

3. عدد المنتجين في السوق:

إذا زاد عدد المنتجين الذين يقدمون نفس السلعة في السوق، فإن العرض الإجمالي لهذه السلعة سيزداد. على سبيل المثال، إذا دخلت شركات جديدة سوق إنتاج الهواتف الذكية، فإن العرض سيتزايد بسبب المنافسة بين المنتجين.

4. السياسات الحكومية:

الضرائب والدعم الحكومي لهما تأثير كبير على العرض. فرض ضرائب جديدة على المنتجات قد يؤدي إلى تقليل العرض بسبب زيادة تكاليف الإنتاج. على العكس، الدعم الحكومي، مثل تقديم حوافز مالية للمنتجين، قد يزيد العرض من خلال تقليل تكاليف الإنتاج.

5. التوقعات المستقبلية للأسعار:

توقعات المنتجين بشأن الأسعار المستقبلية تؤثر أيضًا على العرض. إذا توقع المنتجون ارتفاع الأسعار في المستقبل، قد يقللون من العرض الحالي لزيادة الربح في وقت لاحق. على العكس، إذا توقعوا انخفاض الأسعار، قد يزيدون من العرض الحالي للاستفادة من الأسعار المرتفعة قبل انخفاضها.

6. المنافسة:

المنافسة بين الشركات تؤثر أيضًا على العرض. في حالة وجود منافسة شديدة، قد تسعى الشركات لزيادة إنتاجها لتلبية الطلب والحفاظ على حصتها السوقية.

ما هو قانون العرض؟

قانون العرض هو مبدأ اقتصادي يشير إلى العلاقة الطردية بين سعر السلعة أو الخدمة والكمية المعروضة منها في السوق. وفقاً لهذا القانون، عندما يرتفع سعر السلعة، يزيد المنتجون من الكمية التي يعرضونها للبيع، والعكس صحيح، أي أنه عندما ينخفض السعر، تقل الكمية المعروضة. السبب وراء هذه العلاقة هو أن ارتفاع الأسعار يشجع المنتجين على زيادة إنتاجهم لتحقيق أرباح أكبر، بينما يؤدي انخفاض الأسعار إلى تقليل الإنتاج لتجنب الخسائر.

على سبيل المثال، إذا ارتفع سعر القمح، فإن المزارعين قد يزرعون المزيد من القمح لزيادة أرباحهم. ولكن إذا انخفض سعر القمح، فإنهم قد يقللون من زراعته أو يتحولون إلى زراعة محاصيل أخرى أكثر ربحية.

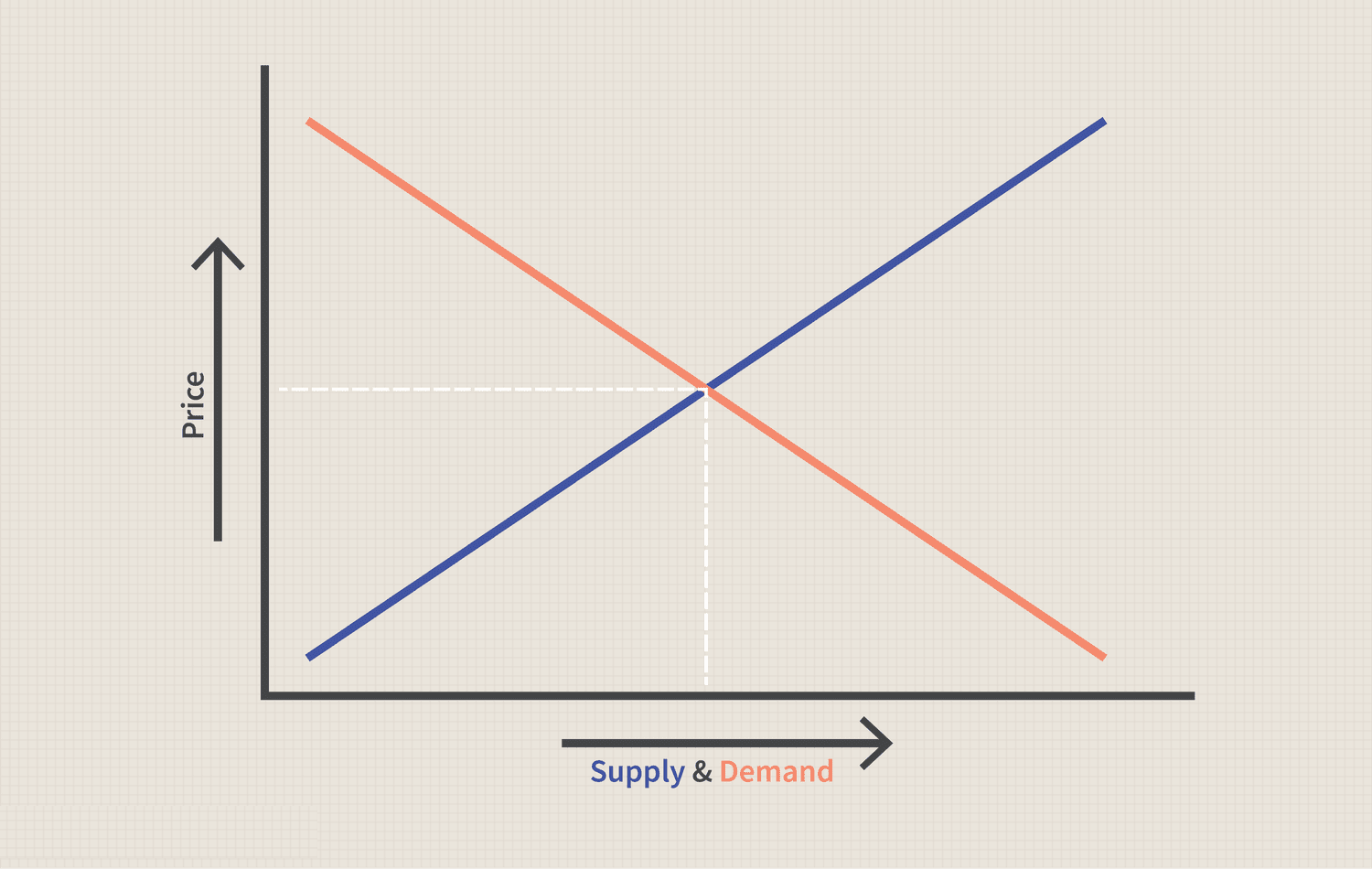

يعمل قانون العرض مع قانون الطلب لتحديد سعر التوازن في السوق، حيث تتلاقى الكمية المطلوبة مع الكمية المعروضة.

توازن السوق أو التوازن بين العرض والطلب

إن آلية التسعير في السوق الحرة تساوي بين العرض والطلب. يميل المشترون إلى رفع السعر إذا أرادوا شراء كمية أكبر من السلعة مما هو متاح بالسعر الحالي. ويخفض الموردون الأسعار إذا أرادوا شراء كمية أقل مما هو معروض بالسعر الحالي.

وبالتالي، تحدد آلية التسعير كمية السلع التي سيتم إنتاجها. ويحدد نظام التسعير أيضًا الأشياء التي سيتم إنشاؤها، وكيف سيتم إنتاجها، ومن سيحصل عليها - أي كيف سيتم توزيع السلع.

يمكن إنشاء السلع الاستهلاكية والخدمات والعمالة والسلع الأخرى القابلة للبيع وتوزيعها بهذه الطريقة. وفي كلتا الحالتين، ستؤدي الزيادة في الطلب إلى ارتفاع السعر، مما يدفع المنتجين إلى توفير المزيد؛ وسيؤدي انخفاض الطلب إلى انخفاض السعر، مما يدفع المنتجين إلى توفير كميات أقل.

ونتيجة لذلك، يوفر نظام التسعير مقياسًا بسيطًا يمكن من خلاله وزن المطالب المتعارضة من قبل أي مستهلك أو منتج. إن العلاقة الاقتصادية بين البائعين والمشترين للسلع المختلفة يتم تحديدها من خلال قانون العرض والطلب.

وفقًا لنظرية العرض والطلب، يتم تحديد سعر المنتج من خلال توفره وطلب العملاء عليه. إذا كان سعر المنتج مرتفعًا، فسوف يعرض البائعون المزيد منه في السوق.

من ناحية أخرى، قد يكون للحفاظ على السعر مرتفعًا تأثيرًا سلبيًا على كيفية إدراك المشترين للمنتج. إذا لم يعتقد العملاء أن المنتج يستحق السعر المرتفع، فقد يختارون بديلاً أقل تكلفة. قد يؤدي السعر المرتفع إلى انخفاض الطلب، مما قد يؤدي إلى انخفاض العرض

التحولات في منحنيات العرض والطلب

التحولات في منحنيات العرض والطلب تشير إلى التغيرات التي تحدث في مستوى العرض أو الطلب في السوق بسبب عوامل خارجية تؤثر على سلوك المنتجين أو المستهلكين. هذه التحولات يمكن أن تؤدي إلى انتقال منحنى العرض أو الطلب إلى اليمين أو اليسار، مما يعكس زيادة أو انخفاضًا في العرض أو الطلب عند كل مستوى سعري.

التحولات في منحنى الطلب:

يشير إلى تغيّر في الكمية المطلوبة للسلعة أو الخدمة عند كل مستوى من الأسعار، دون حدوث تغيير في السعر نفسه. يمكن أن تحدث هذه التحولات نتيجة عوامل متعددة مثل:

1. الدخل: زيادة دخل المستهلكين تؤدي إلى زيادة الطلب على السلع (انتقال المنحنى إلى اليمين)، والعكس صحيح.

2. الأذواق والتفضيلات: تغيّر الأذواق لصالح سلعة معينة يزيد من الطلب عليها.

3. تغير أسعار السلع البديلة أو المكملة: إذا ارتفع سعر سلعة بديلة، فقد يزيد الطلب على السلعة الأصلية.

4. التوقعات المستقبلية: إذا توقع المستهلكون ارتفاع الأسعار في المستقبل، فقد يزيدون من الطلب في الوقت الحالي.

5. عدد المستهلكين: زيادة عدد المستهلكين في السوق يؤدي إلى زيادة الطلب.

التحولات في منحنى العرض:

يشير إلى تغيّر في الكمية المعروضة من السلعة عند كل مستوى من الأسعار. يمكن أن يحدث التحول في منحنى العرض بسبب عوامل مثل:

1. تكلفة الإنتاج: ارتفاع تكاليف الإنتاج مثل المواد الخام أو الأجور يؤدي إلى تقليل العرض (انتقال المنحنى إلى اليسار).

2. التكنولوجيا: تحسين التكنولوجيا يؤدي إلى زيادة الكفاءة وتقليل تكاليف الإنتاج، مما يزيد من العرض.

3. الضرائب والدعم الحكومي: فرض ضرائب أعلى على المنتجين يقلل من العرض، في حين أن الدعم الحكومي يمكن أن يزيد من العرض.

4. عدد المنتجين: دخول المزيد من المنتجين إلى السوق يزيد من العرض.

5. التوقعات المستقبلية: إذا توقع المنتجون ارتفاع الأسعار في المستقبل، فقد يقللون من العرض الحالي.

أثر التحولات:

عندما يحدث تحول في منحنى العرض أو الطلب، فإنه يؤدي إلى تغيّر في سعر التوازن وكمية التوازن في السوق.

أسئلة شائعة

ما هو مفهوم العرض والطلب؟

مفهوم العرض والطلب يشير إلى العلاقة بين كمية السلع والخدمات المتاحة في السوق والكمية التي يرغب المستهلكون في شرائها. العرض هو الكمية التي تقدمها الشركات في السوق بأسعار معينة، بينما الطلب هو الكمية التي يرغب المستهلكون في شرائها عند تلك الأسعار. عندما يرتفع سعر السلع، يميل العرض إلى الزيادة بينما ينخفض الطلب. على العكس، عندما ينخفض السعر، يزيد الطلب ويقل العرض. هذه الديناميكية تؤدي إلى تحديد السعر التوازني الذي يتساوى فيه العرض مع الطلب. من خلال هذه العلاقة، يمكننا فهم كيفية تحديد الأسعار في السوق وكيف تتأثر القرارات الاقتصادية بالعوامل المختلفة .

كيف يؤثر تغير الأسعار على العرض والطلب؟

تغير الأسعار له تأثير مباشر على العرض والطلب. عندما يرتفع سعر المنتج، فإن المنتجين يكونون أكثر رغبة في زيادة كمية العرض، لأنهم يرون فرصة لتحقيق أرباح أكبر. في المقابل، يؤدي ارتفاع الأسعار إلى انخفاض الطلب، حيث يمكن أن يصبح المنتج غير ميسور بالنسبة لبعض المستهلكين. على الجانب الآخر، إذا انخفض السعر، فإن الطلب يميل إلى الزيادة، حيث يمكن للمستهلكين شراء المزيد من المنتج بأسعار أقل. هذه التغيرات في الأسعار تؤثر على التوازن في السوق، مما يؤدي إلى إعادة تقييم العرض والطلب وفقًا للظروف الجديدة. هذا التفاعل بين الأسعار والعرض والطلب هو ما يجعل السوق ديناميكيًا ويستجيب للاحتياجات المتغيرة .

ما هي العوامل المؤثرة في الطلب؟

توجد عدة عوامل تؤثر في الطلب، من أبرزها الدخل، والأسعار البديلة، وتفضيلات المستهلكين. عندما يزيد دخل المستهلكين، فإنهم يميلون إلى زيادة الطلب على السلع والخدمات، خصوصًا السلع الكمالية. كما أن أسعار المنتجات البديلة تلعب دورًا هامًا؛ إذا ارتفع سعر منتج معين، قد يتجه المستهلكون إلى بدائل أقل تكلفة، مما يقلل الطلب على المنتج الأصلي. بالإضافة إلى ذلك، تتأثر الطلبات بتغيرات في تفضيلات المستهلكين، مثل الاتجاهات الثقافية أو الإعلانات. لذلك، تعتبر فهم العوامل المؤثرة في الطلب أمرًا حيويًا للشركات من أجل تكييف استراتيجياتها التسويقية وزيادة مبيعاتها .

كيف يمكن أن تؤثر التغيرات في العرض على الأسعار في السوق؟

التغيرات في العرض يمكن أن تؤدي إلى تقلبات كبيرة في الأسعار في السوق. إذا زاد العرض بشكل كبير، على سبيل المثال بسبب تقدم التكنولوجيا أو زيادة الإنتاج، فقد يؤدي ذلك إلى انخفاض الأسعار لأن السلع تصبح متاحة أكثر. هذا الانخفاض في الأسعار قد يشجع المستهلكين على شراء المزيد، مما يزيد الطلب. من ناحية أخرى، إذا كان هناك انخفاض في العرض، مثلما يحدث بسبب الكوارث الطبيعية أو نقص المواد الخام، فإن الأسعار سترتفع بسبب قلة السلع المتاحة في السوق. هذه الزيادة في الأسعار قد تؤدي إلى تقليل الطلب، حيث يصبح المنتج أقل قدرة على الشراء. بالتالي، فإن فهم كيفية تأثير التغيرات في العرض على الأسعار يساعد على توقع الاتجاهات الاقتصادية والتخطيط الفعال في السوق .

في النهاية، يعد العرض والطلب ركيزتين أساسيتين لفهم الأسواق وتحليل الاقتصاد. يؤثران بشكل كبير على الأسعار وحجم المعروض من السلع والخدمات، وتتأثر هذه العلاقة بعدة عوامل، منها تفضيلات المستهلكين والتغيرات الاقتصادية والعوامل البيئية. لذلك، فإن فهم ديناميكيات العرض والطلب يمكن أن يساهم في تحسين القرارات الاقتصادية سواء على مستوى الأفراد أو الشركات .

المصادر