Introduction

Tax accounting is an integral aspect of financial management that ensures individuals and businesses comply with their tax obligations while optimising their tax liabilities legally. It goes beyond mere record-keeping and delves into the complexities of tax regulations and laws. In this blog post, we will explore the definition and various types of tax accounting, highlighting its importance in financial planning and decision-making. Additionally, we will examine accountants' specific roles in organisations, providing insights into how their expertise drives successful financial strategies.

What Is Tax Accounting?

Tax accounting is a specialised accounting branch that prepares, analyses, and submits tax-related documents and financial records. Its primary purpose is to ensure compliance with the tax laws and regulations of the relevant jurisdiction while maximising tax efficiency. Tax accountants work diligently to interpret the ever-changing tax codes and tailor financial strategies accordingly, ultimately contributing to an entity's fiscal success.

Types of Tax Accounting

In the complex realm of tax accounting, different types cater to the specific needs and challenges individuals and businesses face. Understanding these diverse branches is crucial for tax accountants to provide effective guidance and ensure compliance. Let's delve deeper into each category:

a) Individual Income Tax Accounting

Individual income tax accounting is a personalised approach to navigating the intricate web of personal finances. Tax accountants in this field are akin to financial navigators for individuals, steering through the nuances of tax regulations to optimise returns. They assist in the meticulous preparation of tax returns, considering diverse income streams, deductions, and tax credits. This process aims to minimise tax burdens and ensure full compliance with the ever-evolving tax laws applicable to individual taxpayers.

In the context of individual income tax accounting, tax accountants often advise on investment decisions, retirement planning, and the implications of life events such as marriage or the birth of a child. The meticulous nature of this accounting type requires a deep understanding of the individual's financial landscape and an ability to tailor strategies that align with both short-term financial goals and long-term financial well-being.

b) Corporate Tax Accounting

Corporate tax accounting presents a distinct set of challenges compared to individual income tax accounting. Here, tax accountants navigate the labyrinthine world of business finance, ensuring that companies adhere to tax laws while strategically optimising their tax positions. This involves meticulous reporting of corporate income, expenses, and tax credits.

One critical aspect of corporate tax accounting is dealing with complex issues such as transfer pricing, capital gains and losses, and deductions. Transfer pricing, for instance, involves determining the prices at which transactions occur between different entities within the same corporate group. Tax accountants specialising in corporate tax must carefully navigate these intricacies to maximise the company's financial efficiency while safeguarding against potential legal pitfalls.

c) International Tax Accounting

The globalisation of businesses has created the need for international tax accounting. Companies operating across borders face unique challenges due to varying tax laws and treaties between countries. International tax accountants are crucial in ensuring that multinational entities operate efficiently and compliantly in this complex environment.

In addition to managing the standard tax considerations, international tax accountants must grapple with issues like double taxation, transfer pricing across different jurisdictions, and the implications of tax treaties. This necessitates a profound understanding of not only the tax regulations of individual countries but also the interactions between these regulations on a global scale. International tax accountants are, therefore, strategic partners in helping companies navigate the intricate web of international taxation, optimising their global operations.

d) Sales Tax Accounting

Sales tax accounting revolves around the financial intricacies of the transactions between businesses and consumers. Businesses must comply with regional and local sales tax laws, and sales tax accountants play a pivotal role in ensuring accurate reporting and timely remittance of sales taxes to the appropriate authorities.

This type of tax accounting involves calculating, collecting, and remitting sales taxes, requiring a keen eye for detail. Sales tax rates can vary not only between regions but also between goods and services. Sales tax accountants need to stay abreast of these variations to ensure compliance. Furthermore, advancements in e-commerce have added another layer of complexity, as businesses engage in transactions across geographical boundaries, triggering diverse sales tax regulations.

e) Property Tax Accounting

Property tax accounting focuses on managing taxes levied on real estate and tangible assets. This type of tax accounting is unique as it involves assessing the value of taxable properties and facilitating the payment of property taxes. Property tax accountants must be well-versed in real estate valuation methodologies and local tax assessment practices.

Unlike other types of taxes that may vary with income or sales, property taxes are often based on the property's assessed value. This requires property tax accountants to conduct detailed assessments, considering factors like property improvements and market trends. Property tax regulations can vary widely between different jurisdictions, adding another layer of complexity to this specialised area of tax accounting.

Exploring these distinct types of tax accounting sheds light on the diverse skill sets required by tax accountants. It underscores the need for specialisation and a deep understanding of the unique challenges posed by each category, ensuring that professionals can navigate the complexities of the ever-evolving tax landscape.

Why Is Tax Accounting Important?

Tax accounting holds immense significance for both individuals and businesses for various reasons:

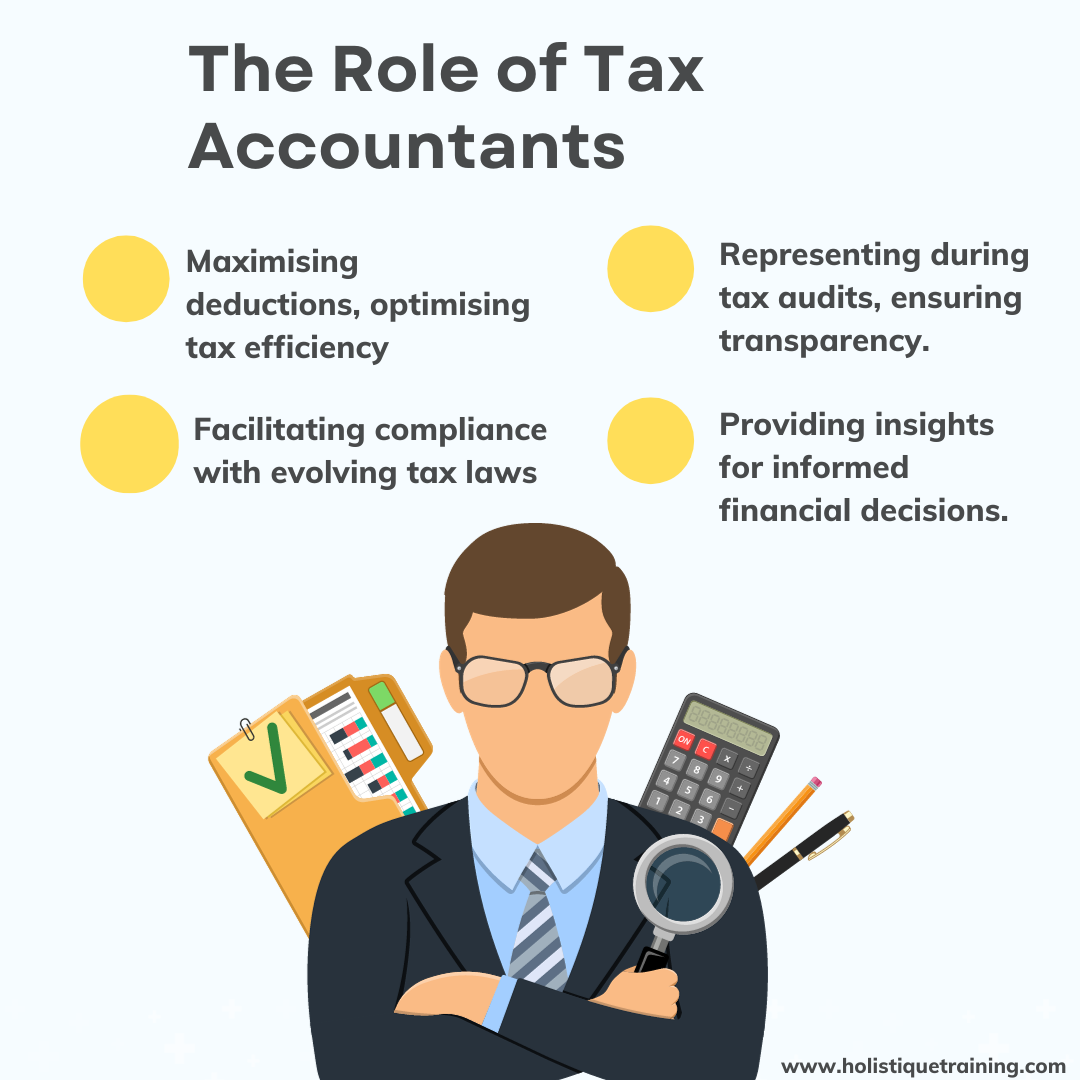

a) Compliance and Avoidance of Penalties

Accurate tax accounting is paramount in its role as a safeguard against non-compliance. Tax laws are intricate and subject to frequent changes, and failure to adhere to them can result in severe penalties and legal consequences. Tax accountants serve as the guiding compass, helping individuals and businesses navigate the complexities of tax regulations. By staying abreast of the latest tax codes and regulations, tax accountants mitigate the risk of non-compliance, ensuring that their clients operate within the legal boundaries and avoid punitive measures.

Moreover, as regulatory bodies become increasingly stringent in enforcing tax compliance, the expertise of tax accountants becomes indispensable. They act as the first line of defence against potential legal ramifications, providing peace of mind to individuals and businesses by fostering adherence to the ever-evolving tax laws.

b) Tax Efficiency and Savings

Tax efficiency is not merely a financial buzzword; it's a tangible outcome of effective tax accounting. Tax accountants are adept at employing various strategies to optimise tax liabilities while staying firmly within the bounds of the law. This involves meticulously examining available deductions, credits, and incentives that align with the client's financial profile.

Effective tax planning can lead to substantial tax savings, facilitated by knowledgeable tax accountants. Individuals and businesses can reduce their overall tax burden by strategically managing capital gains and losses, maximising available deductions, and exploring applicable tax incentives. Tax accounting transforms into a proactive tool for financial optimisation, allowing clients to retain more of their hard-earned money.

c) Financial Decision-Making

Tax considerations pervasively influence financial decisions. Individuals and businesses are confronted with myriad choices, from investment strategies to business expansion, and each decision carries its own set of tax implications. Armed with their expertise, tax accountants provide invaluable insights into these choices' tax ramifications.

By integrating tax considerations into financial decision-making, tax accountants empower their clients to make informed choices that align with their overarching financial goals. Whether it's choosing the most tax-efficient investment vehicle or structuring a business transaction to minimise tax liabilities, the guidance of a tax accountant ensures that financial decisions are not made in isolation but are part of a comprehensive, tax-aware strategy.

d) Audit Support

Auditing tax authorities through audits is an inevitable aspect of financial life. In such instances, the importance of well-maintained and accurate tax records cannot be overstated. Tax accountants are pivotal in providing audit support, acting as the liaison between the client and tax authorities.

During audits, tax accountants' comprehensive understanding of an individual's or business's financial data and in-depth knowledge of tax regulations position them as advocates for their clients. They confidently navigate the audit process, ensuring all necessary documentation is available and transparent. This facilitates a smoother audit and enhances the client's credibility with tax authorities, mitigating the risk of unnecessary disputes or penalties.

Tax accounting is not a mere formality but a dynamic and strategic discipline that transcends traditional notions. It is a linchpin for ensuring financial compliance, optimising resources, and guiding individuals and businesses toward fiscal success. As the financial landscape continues to evolve, the role of tax accounting becomes increasingly pivotal, underscoring its status as an indispensable facet of modern financial management.

Aspect | Description |

Integration of ESG into Tax | Aligning tax strategies with environmental sustainability |

ESG Reporting and Transparency | Ensuring accurate and comprehensive disclosure of ESG practices |

Incentives for ESG Activities | Identifying and leveraging tax incentives for sustainable initiatives |

International Tax Planning | Navigating diverse ESG regulations in global operations |

Ethical Leadership in Governance | Fostering ethical governance practices within tax planning |

Table 1: ESG integration into tax planning

Tax Accounting and VAT

Value Added Tax (VAT) is a consumption tax levied on the value added to goods and services at each stage of production or distribution. VAT accounting requires meticulous record-keeping and compliance with VAT regulations, including timely filing of returns. VAT-registered businesses must account for the VAT they charge on sales (output tax) and the VAT they pay on purchases (input tax). The difference between output and input tax is the net amount payable to the tax authority.

VAT accounting can be complex, particularly for businesses operating across borders. Accountants specialising in VAT ensure businesses comply with the relevant VAT laws and maximise opportunities for VAT reclaims, reducing the overall VAT burden.

Tax Accounting and Self-Assessment

Self-assessment is a tax system in which individuals and businesses calculate their tax liability and submit a tax return to the tax authorities. This system requires taxpayers to ensure accurate reporting, making tax accounting critical.

Tax accountants assist individuals and businesses in navigating the self-assessment process, guiding them incorrectly calculating their taxable income, deductions, and credits. They also help prepare and file the tax return, reducing the risk of errors and potential penalties.

This Training course is aimed at business professionals who need to understand how finance works. Financial information can provide a clear picture of how to increase profitability, decrease costs, and meet targets in any business. It is very crucial that

Your Role as an Accountant in an Organisation

As an accountant in an organisation, your role extends beyond merely crunching numbers. You play a pivotal role in ensuring the financial health and success of the organisation. In the context of tax accounting, your responsibilities include:

a) Tax Planning and Compliance

Your expertise in tax accounting positions you as a key player in developing effective tax strategies aligned with the organisation's financial objectives. Tax planning is not a one-size-fits-all endeavour; it requires a nuanced understanding of the organisation's structure, operations, and long-term goals. By delving into the intricacies of tax laws and regulations, you ensure that the company not only maximises its tax efficiency but also remains fully compliant with the ever-evolving tax landscape.

This involves proactive steps such as identifying eligible deductions, optimising the timing of transactions to minimise tax liabilities, and exploring potential tax credits. As the steward of the organisation's financial well-being, you play a vital role in mitigating the risk of penalties and legal issues by ensuring adherence to tax laws.

b) Record-keeping and Documentation

Accurate and well-organised financial records are the bedrock of effective tax accounting. In your role, meticulous record-keeping is not just a compliance requirement; it's a strategic imperative. You maintain a detailed account of income, expenses, deductions, and credits, ensuring that the organisation's financial data is readily available and accessible for tax purposes.

This involves leveraging modern accounting software and technologies to streamline record-keeping processes. By maintaining a digital trail of financial transactions, you enhance the efficiency of day-to-day operations, facilitate seamless audits, and ensure transparency in financial reporting.

c) Tax Reporting and Filing

Preparing and filing accurate tax returns on behalf of the organisation is a core responsibility. This goes beyond mere data entry; it involves a comprehensive understanding of the organisation's financial landscape to calculate the correct tax liability. In this capacity, you maximise deductions, ensure compliance with all relevant tax codes, and meet stringent filing deadlines.

Tax reporting accuracy is crucial during audits or reviews by tax authorities. By diligently preparing and filing tax returns, you contribute to the organisation's credibility and demonstrate a commitment to financial transparency and compliance.

d) Tax Audits and Disputes

In the event of a tax audit or dispute, you step into a critical role as the organisation's representative before tax authorities. Your comprehensive knowledge of the company's financial data and a deep understanding of tax regulations allow you to navigate the audit process confidently.

During audits, you serve as the liaison between the organisation and tax authorities, ensuring that all necessary documentation is provided and discrepancies are addressed. Your role is not just reactive but also proactive. Maintaining accurate records and adhering to best practices in tax accounting minimises the likelihood of disputes and contributes to a smooth audit process.

e) Financial Strategy and Decision Support

Beyond the specific realm of tax accounting, your financial expertise positions you as a valuable asset in crafting the organisation's overall financial strategies. You provide insights into the broader financial implications of various decisions, enabling the organisation to make informed choices that contribute to its financial growth.

This involves collaborating with other departments to align financial goals with operational strategies. Whether it's evaluating the financial viability of a new project, assessing the impact of a strategic business decision, or planning for long-term financial sustainability, your role extends to being a trusted advisor on matters that transcend the immediate scope of tax accounting.

In summary, your role as an accountant within an organisation transcends the traditional view of number-crunching. You are a strategic partner, contributing to the organisation's financial success by ensuring compliance, optimising tax strategies, and providing valuable insights for informed decision-making. Embracing the complexities of tax accounting empowers you to make a substantial impact, solidifying your position as a key player in the organisation's journey towards financial excellence.

Tax Accounting and Technology

In the ever-evolving financial management landscape, integrating technology into tax accounting practices has become a game-changer. The symbiotic relationship between tax accounting and technology streamlines routine tasks and enhances tax professionals' strategic capabilities. Here's how technology is reshaping the field of tax accounting:

1. AI and Machine Learning

Artificial Intelligence (AI) and Machine Learning (ML) have emerged as powerful tools in the tax accountant's arsenal. The market size of Artificial Intelligence in Accounting is anticipated to experience substantial growth, increasing from USD 1.17 billion in 2023 to reach USD 4.96 billion by 2028, reflecting a robust Compound Annual Growth Rate (CAGR) of 33.50% over the forecast period from 2023 to 2028, according to Mordor Intelligence. AI and ML enable automated data analysis, freeing up accountants from routine tasks and allowing them to focus on more strategic aspects of tax accounting. These technologies can process vast datasets at speeds impossible for humans, identifying patterns, anomalies, and potential areas for tax optimisation.

Moreover, machine learning algorithms can provide predictive insights into future tax trends. By analysing historical data and considering external factors, AI systems can help tax accountants anticipate changes in tax regulations or identify potential areas of risk and opportunity. This predictive capability enhances the proactive nature of tax planning, allowing organisations to stay ahead of the curve in a dynamic regulatory environment.

2. Blockchain

Blockchain technology is revolutionising the way financial transactions are recorded and verified. In tax accounting, where data accuracy and security are paramount, blockchain provides a decentralised and tamper-resistant ledger. Transactions recorded on a blockchain are transparent, traceable, and immune to unauthorised alterations.

For tax accountants, this means a higher level of confidence in the integrity of financial data. Blockchain's secure and transparent nature reduces the risk of errors or fraud in financial records. Additionally, the decentralised nature of blockchain eliminates the need for intermediaries, streamlining the verification process and reducing the time and resources traditionally spent on reconciling financial transactions.

Blockchain is a technology that distributes a shared database or ledger across nodes in a computer network. Its decentralised and distributed nature is disrupting traditional products and services and providing opportunities to securely store different types of transactional data. This course

3. Cloud Computing

Cloud computing has transformed the way tax accountants access and manage financial data. The ability to store and retrieve data from the cloud provides unprecedented flexibility, allowing tax professionals to work from anywhere with an internet connection. This remote accessibility enhances the efficiency of day-to-day operations and facilitates collaborative workflows among team members located in different geographic locations.

Cloud-based accounting software offers real-time updates and synchronisation, ensuring everyone involved in the tax accounting process works with the latest data. This reduces the likelihood of errors due to data discrepancies and fosters seamless communication and collaboration among team members, whether they are in the same office or spread across the globe.

The Impact of Technology on Tax Accounting Professionals

The integration of technology into tax accounting practices has transformative implications for tax professionals:

a) Skill Evolution

As technology automates routine tasks, tax professionals find themselves in a position where strategic skills become more critical. The ability to interpret complex data analyses, understand the outputs of AI algorithms, and make informed decisions based on predictive insights becomes paramount. Tax accountants need to evolve from being data processors to data interpreters and strategists.

b) Risk Management

While technology enhances efficiency, it also introduces new risks, such as cybersecurity threats and data breaches. Tax accountants must adapt to a landscape where safeguarding sensitive financial information is as crucial as optimising tax liabilities. This involves staying updated on cybersecurity best practices and employing technologies prioritising data security.

c) Client Engagement

Technology facilitates a more dynamic and interactive client experience. Through online collaboration tools and cloud-based platforms, tax accountants can engage with clients in real-time, providing instant insights and updates. This strengthens client relationships and positions tax professionals as proactive advisors rather than mere service providers.

In short, integrating technology into tax accounting is not a mere trend but a transformative shift that redefines the role of tax professionals. The symbiotic relationship between tax accounting and technology empowers professionals to navigate the complexities of a dynamic financial landscape. As tax accountants embrace these technological advancements, they position themselves as stewards of financial data and as strategic partners contributing to the overall success and resilience of the organisations they serve.

Conclusion

Tax accounting is a multifaceted discipline that is vital in ensuring compliance with tax laws, optimising tax liabilities, and facilitating sound financial decision-making. Accountants specialising in tax accounting are indispensable assets to individuals and organisations, guiding them through complex tax processes and safeguarding their financial well-being. As an accountant in an organisation, your expertise in tax accounting positions you as a key player in driving financial success and growth. Embracing the intricacies of tax accounting empowers you to make a substantial impact, both for your clients and the organisations you serve.

Finally, if you're passionate about advancing your financial career, we encourage you to enroll in our renowned MBA Accounting and Finance course. In it, you'll gain comprehensive knowledge and practical skills to excel in the dynamic world of accounting and finance.

Having accurate and efficient accounting and finance processes, employees, and systems are essential to any business. Without good record upkeep, policies designed to keep track of spending and overheads, and competent employees who are prepared to identify issues and risk areas, your business could fall