- Table of Contents

- Introduction

- What is Depreciation?

- Types of Depreciation and How to Calculate Each One

- Straight-Line Depreciation:

- Declining Balance Depreciation:

- Sum-of-the-Years'-Digits (SYD) Depreciation:

- Units of Production Depreciation:

- Which Assets Can You Depreciate?

- 1. Property

- 2. Vehicles and Equipment

- 3. Furniture and Fixtures

- 4. Intangible Assets

- 5. Specialised Equipment

- 6. Rental and Leased Assets

- What Assets Cannot Be Depreciated?

- Land:

- Inventory:

- Personal Assets:

- Assets with Indefinite Lifespans:

- What Are the Causes of Depreciation?

- 1. Wear and Tear

- 2. Obsolescence

- 3. Natural Factors

- 4. Time

- 5. Usage Intensity

- 6. Depletion

- 7. Legal and Regulatory Changes

- 8. Economic Factors

- 9. Accidents and Damage

- 10. Maintenance Neglect

- Benefits of Calculating Depreciation

- 1. Accurate Financial Reporting

- 2. Tax Savings

- 3. Budgeting and Planning

- 4. Asset Management

- 5. Decision-Making

- 6. Regulatory Compliance

- 7. Enhanced Profitability Analysis

- 8. Supports Loan and Credit Applications

- 9. Facilitates Benchmarking

- 10. Encourages Strategic Asset Allocation

- Depreciation Practices in Accounting

- What is a Depreciation Schedule?

- What to Do After Calculating Depreciation

- 1. Evaluate Asset Performance

- 2. Plan for Asset Replacement

- 3. Improve Budgeting and Cash Flow Management

- 4. Enhance Tax Planning

- 5. Support Decision-Making in Financing and Investments

- 6. Track and Manage Intangible Assets

- 7. Improve Profitability Analysis

- 8. Facilitate Financial Reporting and Compliance

- 9. Inform Strategic Business Decisions

- 10. Communicate Value to Stakeholders

- Conclusion

Introduction

Depreciation is a fundamental concept in accounting and finance that impacts businesses, investors, and accountants alike. It refers to the reduction in value of an asset over time, usually due to wear and tear, age, or obsolescence. This process has significant implications for both financial reporting and tax purposes. In this blog post, we will explore the intricacies of depreciation, focusing on its types, causes, benefits, and how to calculate it accurately. We will also delve into the depreciation schedule, the accounting practices that govern it, and how businesses can leverage depreciation data for sound decision-making.

What is Depreciation?

Depreciation is the process by which businesses allocate the cost of tangible assets over their useful life. Rather than expensing the full purchase price of an asset in the year it was acquired, depreciation allows businesses to spread this cost across several years. This not only ensures more accurate financial reporting but also provides tax benefits by reducing taxable income.

For instance, if a company buys a piece of machinery for $100,000, it will not list this expense in full in the year of purchase. Instead, the company will apply depreciation to this asset over its useful life, distributing the cost over several years. This makes the financial impact of acquiring the machinery more manageable and reflective of its actual consumption in the business.

Types of Depreciation and How to Calculate Each One

There are several methods of calculating depreciation, each suited for different types of assets and business needs. The main types of depreciation include:

Straight-Line Depreciation:

This is the simplest and most commonly used method. With straight-line depreciation, the same amount of depreciation expense is recorded each year over the asset’s useful life. The formula for straight-line depreciation is:

Annual Depreciation Expense=Cost of Asset - Salvage ValueUseful Life of Asset

Example: If a piece of machinery costs $50,000, has a salvage value of $5,000, and a useful life of 5 years, the annual depreciation expense would be:

50,000 - 5,0005=9,000 per year

Declining Balance Depreciation:

This method applies a constant percentage rate to the asset’s book value, resulting in higher depreciation expenses in the earlier years of the asset’s life. This is particularly useful for assets that lose value more rapidly in their early years. The formula is:

Depreciation Expense=Book Value at Start of YearDepreciation Rate

Example: If an asset costs $100,000 with a 20% depreciation rate, the first year’s depreciation would be:

100,0000.20=20,000

In the second year, the depreciation would be based on the new book value after the first year’s depreciation.

Sum-of-the-Years'-Digits (SYD) Depreciation:

This method accelerates depreciation by allocating a larger portion of the asset’s cost in the earlier years, but not as much as declining balance. The depreciation is based on the sum of the years of an asset’s useful life. The formula involves adding up the digits for each year of the asset's life (for example, for a 5-year asset, the sum would be 1 + 2 + 3 + 4 + 5 = 15) and allocating depreciation based on this sum.

Depreciation Method | Description | Best Suited For |

Straight-Line | Spreads asset cost equally over its useful life. | Assets with consistent usage over time. |

Declining Balance | Higher depreciation initially, less in later years. | Rapidly depreciating or high-tech assets. |

Sum-of-the-Years’-Digits | Accelerates depreciation based on asset lifespan fraction. | Assets losing value quickly upfront. |

Units of Production | Depreciation based on usage or output level. | Manufacturing equipment or production tools. |

Double Declining Balance | Twice the straight-line rate; front-loaded expense. | Assets needing fast write-offs for taxes. |

Units of Production Depreciation:

This method ties depreciation to the actual usage of an asset, making it more variable and reflective of how much the asset is used in a given period. For example, an asset used more heavily in one year than in another will have a higher depreciation expense in the busier year. The formula is:

Depreciation Expense=Cost of Asset - Salvage ValueTotal Estimated ProductionActual Production in the Period

Each of these methods has its advantages depending on the nature of the asset and the company's financial strategy.

Which Assets Can You Depreciate?

Not all assets are eligible for depreciation. Depreciation applies to assets with a finite useful life that businesses use in their operations. These assets gradually lose value due to wear and tear, obsolescence, or other factors. Here’s a detailed look at the types of assets that qualify for depreciation, along with examples and specific considerations:

1. Property

Tangible property, such as buildings and structures, is a common category of depreciable assets. These are assets that businesses own and use in their operations, but which do not last forever. Over time, buildings experience wear and tear, requiring repairs, maintenance, or replacement.

- Buildings and Structures: Depreciation for real estate properties applies only to the structure itself and not the land it occupies. For instance, if a business owns an office building, the building's cost can be depreciated over its useful life, while the land value remains intact because land does not wear out.

- Leasehold Improvements: If a business leases a property and invests in improvements like installing partitions, upgrading electrical systems, or other customizations, these improvements can also be depreciated. The depreciation period for leasehold improvements is typically the shorter of the lease term or the improvement's useful life.

2. Vehicles and Equipment

Vehicles and equipment are central to many businesses and often experience heavy usage, making them eligible for depreciation.

- Vehicles: Company-owned cars, trucks, delivery vans, and specialized vehicles used for business purposes are depreciable. However, the extent to which a vehicle is used for business versus personal purposes can affect the depreciation calculation. For example, a truck used exclusively for deliveries would be fully depreciable, while a personal vehicle used partially for business may have a prorated depreciation amount.

- Machinery and Equipment: From manufacturing machines to office equipment like printers and computers, these assets are essential to business operations. Machinery, for instance, may have a shorter useful life due to its intensive usage in factories. On the other hand, office computers may become obsolete before they physically wear out, necessitating replacement.

3. Furniture and Fixtures

Furniture, fixtures, and fittings used in business operations also qualify for depreciation. Examples include:

- Office desks, chairs, and cabinets in corporate settings.

- Shelving units and display racks in retail stores.

- Fixtures such as lighting systems, air conditioning units, and signage.

These items are generally depreciated over a span of several years, depending on their expected useful life.

4. Intangible Assets

Though depreciation primarily applies to tangible assets, certain intangible assets are also eligible under a related process calledamortization. Intangible assets are non-physical items that provide value to a business over time. Examples include:

- Patents: If a company owns a patent, it can amortize its cost over the patent's legal lifespan, typically 20 years.

- Trademarks: While trademarks may have indefinite lives, those with finite contractual terms can be amortized over their enforceable period.

- Copyrights: The cost of copyrights can be amortized based on their useful legal life or contractual period.

- Licenses and Franchises: These are amortized over the period of their validity.

Intangible assets are not physically worn out, but their value diminishes over time due to factors like expiration or technological advancements.

5. Specialised Equipment

Businesses in niche industries often invest in specialized tools or equipment that can also be depreciated. Examples include:

- Medical equipment in healthcare facilities, such as MRI machines.

- Scientific instruments in research labs.

- Construction equipment like cranes and bulldozers.

These assets often require specific depreciation schedules due to their unique usage and high initial cost.

6. Rental and Leased Assets

If a business owns property or equipment and leases it out to others, these assets can still be depreciated. For example, a company that owns rental properties can depreciate the cost of the building while collecting income from tenants. Similarly, leased machinery can be depreciated as long as the business retains ownership of the asset.

What Assets Cannot Be Depreciated?

While the list of depreciable assets is extensive, it’s also important to understand which assets are not eligible for depreciation:

Land:

Land is not depreciable because it does not wear out, become obsolete, or diminish in utility. Its value is considered indefinite, though it may fluctuate based on market conditions.

Inventory:

Goods held for sale are not depreciable. Instead, they are accounted for as inventory and expensed as cost of goods sold when sold.

Personal Assets:

Any asset used for personal purposes, such as a privately owned car, cannot be depreciated for business purposes unless there is a clear and documented business use.

Assets with Indefinite Lifespans:

Certain intangible assets, like goodwill, may not be amortized under some accounting standards unless their value is deemed to be impaired.

Understanding which assets qualify for depreciation and how they are categorized helps businesses optimize their financial strategies. By accurately identifying depreciable assets, companies can take advantage of tax deductions and align their financial statements with their operational realities. This practice is an essential part of effective financial management and long-term planning.

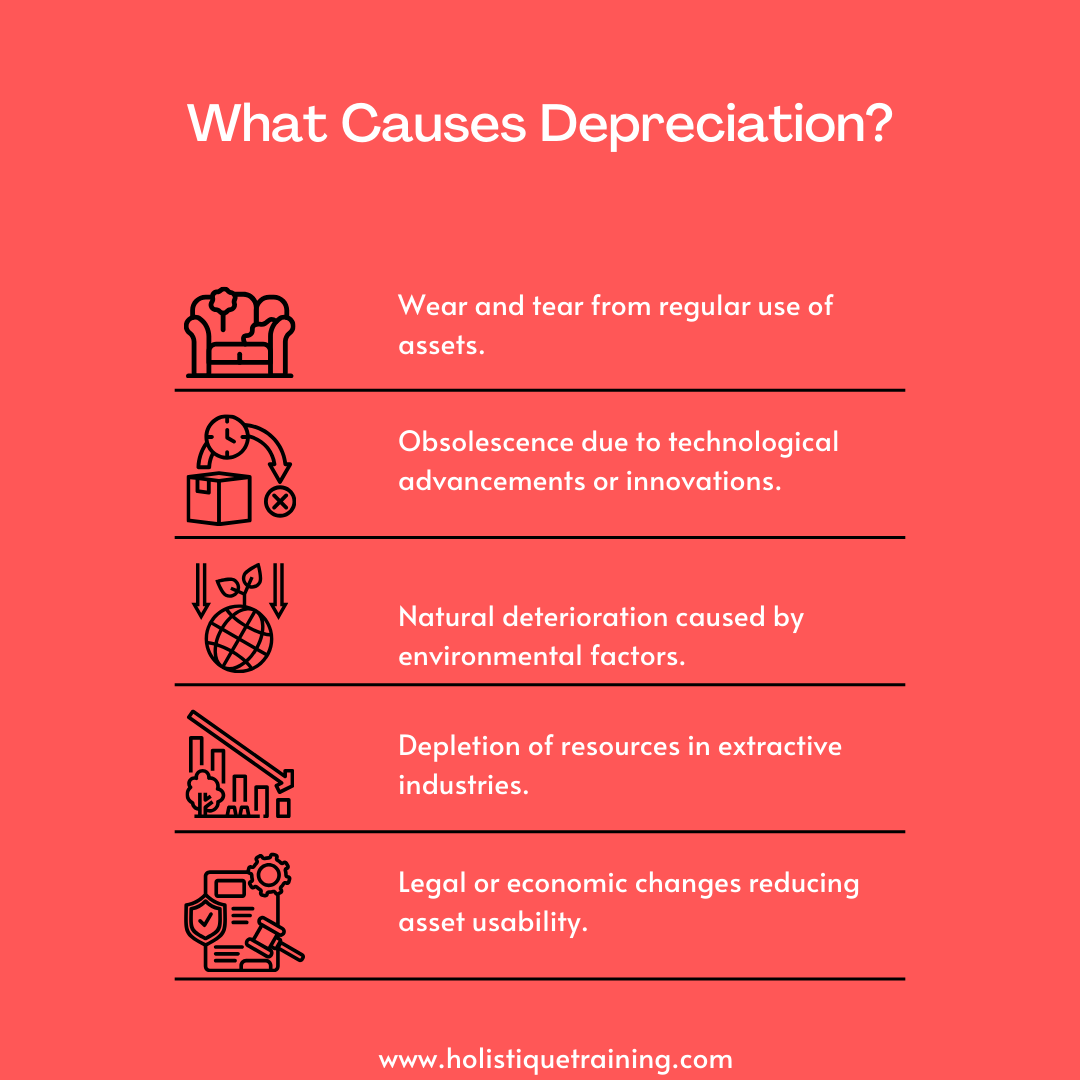

What Are the Causes of Depreciation?

Depreciation is the natural decline in the value of an asset over time due to various factors. Understanding these causes can help businesses better manage their assets, anticipate costs, and make informed financial decisions. Here’s a detailed look at the primary causes of depreciation:

1. Wear and Tear

One of the most obvious causes of depreciation is the physical deterioration of an asset due to regular use. Assets such as machinery, vehicles, and furniture experience constant wear during operation, leading to reduced functionality and efficiency over time.

- Example: A manufacturing machine used for daily production gradually loses its precision and efficiency. Eventually, it may require frequent maintenance or replacement parts, reducing its overall value.

- Impact: Wear and tear are most common in industries where equipment and tools are heavily utilized, such as construction, manufacturing, and transportation.

2. Obsolescence

Technological advancements and changes in market trends can render assets obsolete, even if they remain functional. Obsolescence occurs when an asset no longer meets current standards, market demands, or operational requirements.

- Technological Obsolescence: Equipment like computers and smartphones quickly become outdated as newer, faster, and more efficient models enter the market. Businesses often replace these items before they physically wear out.

- Functional Obsolescence: This occurs when an asset's design or features are no longer adequate for its intended purpose. For instance, a factory may upgrade to modern machinery to improve efficiency, even though the old machines are still operational.

- Market Obsolescence: A shift in consumer preferences can also contribute. For example, traditional retail displays may depreciate faster if the market moves toward digital signage.

3. Natural Factors

Certain assets, especially those exposed to environmental conditions, are subject to depreciation due to natural factors.

- Weather and Climate: Buildings, outdoor equipment, and vehicles are affected by rain, snow, heat, and humidity. Over time, these elements cause rust, corrosion, and structural damage.

- Biological Factors: For assets like agricultural equipment or buildings in pest-prone areas, depreciation may result from damage caused by termites, rodents, or other organisms.

- Example: A coastal property may experience faster depreciation due to exposure to saltwater and strong winds, which can corrode metal and damage structures.

4. Time

Even if an asset is not actively used, its value decreases with time. This is particularly relevant for assets that have a predetermined useful life, such as patents or leased equipment.

- Example: A patent's value diminishes as it nears expiration, regardless of how often it is used in operations.

- Impact: Time-based depreciation is common for intangible assets and assets held as investments, such as leased properties.

5. Usage Intensity

The frequency and intensity with which an asset is used directly affect its rate of depreciation. Assets subjected to heavy usage tend to wear out faster and require more frequent repairs or replacement.

- Example: A delivery vehicle in a logistics company, which operates daily over long distances, will depreciate more quickly than a similar vehicle used occasionally for local errands.

- Impact: Businesses in high-demand industries often face accelerated depreciation rates due to intensive asset usage.

6. Depletion

Certain assets, such as natural resources, experience depreciation through depletion. Depletion refers to the reduction in the availability of a finite resource as it is consumed.

- Example: A mining company depletes the reserves of a coal mine as it extracts coal. Over time, the mine's value decreases as its resources are exhausted.

- Impact: Depletion is unique to industries that rely on natural resource extraction, such as mining, oil, and gas.

7. Legal and Regulatory Changes

Changes in laws, regulations, or industry standards can render certain assets less useful or entirely obsolete, causing depreciation.

- Example: A company using machinery that does not comply with updated environmental standards may need to replace it. This makes the old machinery obsolete and reduces its value.

- Impact: Regulatory-driven depreciation is common in industries like manufacturing, transportation, and energy, where compliance is critical.

8. Economic Factors

Macroeconomic conditions, such as inflation, market downturns, or changes in demand, can also cause asset depreciation.

- Example: During an economic downturn, a commercial property may lose value due to decreased demand for office spaces.

- Impact: Economic factors often affect the resale value of assets, even if their physical condition remains unchanged.

9. Accidents and Damage

Unforeseen incidents, such as accidents or natural disasters, can lead to sudden and significant depreciation of assets.

- Example: A manufacturing plant that sustains damage from a fire may see a sharp decline in the value of its machinery and infrastructure.

- Impact: Insurance coverage may mitigate financial losses, but the depreciation resulting from accidents is often unavoidable.

10. Maintenance Neglect

Proper maintenance extends an asset’s useful life and slows its depreciation. Conversely, neglecting regular upkeep accelerates depreciation.

- Example: A vehicle that does not receive routine servicing will experience faster wear on its engine, tires, and other components.

- Impact: Poor maintenance practices lead to higher repair costs and shorter asset lifespans, increasing overall depreciation rates.

Understanding the causes of depreciation is crucial for businesses to manage their assets effectively. Each factor—whether physical wear, technological obsolescence, or economic shifts—affects the asset's value differently. By recognizing these causes, businesses can take proactive measures, such as regular maintenance, upgrades, or strategic asset allocation, to minimize depreciation’s impact and optimize financial performance.

Benefits of Calculating Depreciation

Calculating depreciation is more than just a financial accounting requirement; it serves as a strategic tool that helps businesses manage their assets effectively, make informed decisions, and maintain compliance with legal and regulatory standards. Here’s a closer look at the significant benefits of calculating depreciation:

1. Accurate Financial Reporting

Depreciation ensures that a company’s financial statements accurately reflect the true value of its assets over time. By systematically allocating the cost of an asset over its useful life, businesses can present a more realistic picture of their financial health.

- Balance Sheet Representation: Depreciation reduces the asset's book value on the balance sheet, preventing overstatement of net assets. For example, a machine purchased for $50,000 but now worth $20,000 due to depreciation will be reflected accurately in the financial records.

- Income Statement Impact: Depreciation is recorded as an expense, reducing taxable income and aligning reported profits with actual asset usage.

2. Tax Savings

Depreciation is a non-cash expense that reduces taxable income, allowing businesses to retain more cash for operations, investments, or other needs.

- Tax Deductions: By deducting depreciation, companies lower their tax liability, providing a financial cushion. For instance, a business claiming $10,000 in depreciation expenses annually can reduce its taxable income by the same amount.

- Accelerated Depreciation Benefits: Certain tax systems allow businesses to use methods like double-declining balance or bonus depreciation to claim higher deductions in the early years of an asset’s life, maximizing upfront tax savings.

3. Budgeting and Planning

Depreciation calculations help businesses anticipate future expenses, such as repairs, maintenance, or replacement of aging assets. This foresight is crucial for effective budgeting and long-term financial planning.

- Repair and Replacement Planning: Knowing when an asset will be fully depreciated helps businesses schedule replacements or upgrades without disrupting operations.

- Cash Flow Management: Depreciation schedules provide insight into ongoing costs, allowing businesses to allocate resources efficiently.

Implementing advanced budgeting techniques is crucial for businesses seeking heightened financial control, strategic planning, and adaptability in today's dynamic business environment. These advanced techniques go beyond traditional budgeting approaches, incorporating sophisticated methodologies to enhance precision and effectiveness. Zero-based budgeting, which requires

4. Asset Management

Depreciation is an essential aspect of tracking and managing a company’s assets. It provides insights into the lifecycle of each asset, helping businesses maximize their value and utility.

- Lifecycle Tracking: Depreciation helps businesses monitor how long an asset remains useful, facilitating timely decisions about upgrades or replacements.

- Optimizing Utilization: Businesses can use depreciation data to evaluate whether assets are being used efficiently. For instance, if a machine is depreciating faster than anticipated due to overuse, the company may need to reassess its operations or invest in additional equipment.

5. Decision-Making

Depreciation figures play a critical role in decision-making processes, particularly in capital investment and operational planning.

- Investment Decisions: When considering purchasing new assets, depreciation data helps businesses estimate costs and evaluate the return on investment (ROI).

- Lease vs. Buy Decisions: Depreciation calculations assist in determining whether leasing or buying an asset is more cost-effective. For example, leasing may be preferable for assets with rapid obsolescence, while buying is advantageous for long-term utility.

The petroleum business is worth billions worldwide, and it’s important to fully understand the potential risks and mitigation tactics to help maintain profits and ensure continuous improvement within individual gas and oil businesses in this huge network. Understanding the implications and costs

6. Regulatory Compliance

Accurate depreciation calculations are essential for complying with accounting standards and tax regulations. Failing to record depreciation properly can lead to financial misstatements, penalties, or audits.

- Accounting Standards: Adhering to Generally Accepted Accounting Principles (GAAP) orInternational Financial Reporting Standards (IFRS) requires consistent and accurate depreciation practices.

- Audit Preparedness: Proper depreciation records help businesses demonstrate compliance during audits, reducing the risk of fines or disputes with tax authorities.

This course is designed to bridge the gap between theoretical knowledge of International Financial Reporting Standards (IFRS) and their practical application in real-world financial reporting. Rather than focusing solely on definitions and rules, the programme emphasises interpretation, professional judgement, and implementation of key IFRS requirements in day-to-day

7. Enhanced Profitability Analysis

Depreciation data enables businesses to conduct more precise profitability analysis by factoring in the cost of asset usage.

- Cost Allocation: By allocating the cost of assets to the periods in which they are used, businesses can better match revenues with expenses, improving the accuracy of profitability metrics.

- Product Pricing: Depreciation expenses can be incorporated into product pricing strategies to ensure profitability. For example, a factory producing goods can include the depreciation cost of machinery in the pricing model.

8. Supports Loan and Credit Applications

Lenders and investors often review a company’s financial statements to assess creditworthiness. Properly depreciating assets enhances the credibility of these statements and demonstrates sound financial management.

- Asset Valuation for Collateral: Depreciated values provide a realistic estimate of asset worth when used as collateral for loans.

- Investor Confidence: Accurate depreciation practices signal to investors that the company is managing its resources prudently.

9. Facilitates Benchmarking

Depreciation calculations provide a basis for comparing the performance and efficiency of assets within the company or against industry standards.

- Internal Benchmarking: Companies can compare the depreciation rates of similar assets to identify inefficiencies or evaluate usage patterns.

- Industry Comparison: Benchmarking against competitors' depreciation practices can highlight areas for improvement, such as adopting more efficient equipment.

10. Encourages Strategic Asset Allocation

By understanding how different assets depreciate, businesses can make informed decisions about where to allocate resources for maximum productivity and cost-effectiveness.

- Example: If an older machine is depreciating rapidly and incurring high maintenance costs, reallocating funds to purchase newer, more efficient equipment may yield better long-term benefits.

Calculating depreciation offers a range of benefits that extend beyond simple compliance. It enhances financial accuracy, supports strategic decision-making, improves tax efficiency, and ensures better asset management. By leveraging depreciation data, businesses can optimize operations, plan effectively, and maintain a competitive edge in their industry.

Depreciation Practices in Accounting

In the United States, depreciation practices must comply withGenerally Accepted Accounting Principles (GAAP), which are standards set by theFinancial Accounting Standards Board (FASB). GAAP ensures consistency and transparency in financial reporting.

Under GAAP, businesses must follow specific rules regarding how depreciation is calculated and reported, ensuring that depreciation expenses are recorded accurately and consistently across all periods. The FASB provides guidance on the acceptable depreciation methods and the useful life of assets. Additionally, companies must disclose the depreciation method used in their financial statements.

Internationally, the International Financial Reporting Standards (IFRS) are used, which provide similar guidelines but allow for more flexibility in certain areas, such as the revaluation of assets.

What is a Depreciation Schedule?

A depreciation schedule is a table or document that outlines the amount of depreciation expense to be recorded each year over the useful life of an asset. It provides a clear picture of how the asset’s value will decline over time.

Typically, a depreciation schedule includes three key columns:

- Year: The year in which the depreciation is being recorded.

- Depreciation Expense: The amount of depreciation for that particular year.

- Accumulated Depreciation: The total amount of depreciation that has been recorded up until that point in time.

By the end of the asset's useful life, the accumulated depreciation will equal the original cost of the asset, minus its salvage value.

Example of a Depreciation Schedule

Year | Depreciation Expense | Accumulated Depreciation | Net Book Value |

1 | $10,000 | $10,000 | $90,000 |

2 | $10,000 | $20,000 | $80,000 |

3 | $10,000 | $30,000 | $70,000 |

In this example, the asset cost $100,000, with a straight-line depreciation method spreading its expense equally over 10 years.

A depreciation schedule is not just a tool for compliance; it’s a vital resource for strategic decision-making. By providing a clear picture of an asset’s declining value, it allows businesses to make informed choices about resource allocation, asset management, and financial planning.

What to Do After Calculating Depreciation

Calculating depreciation is only the first step in managing an asset’s life cycle. Once you have these figures, the next step is to leverage them for strategic decision-making across various aspects of your business. Depreciation data can guide asset management, budgeting, tax planning, financial reporting, and long-term strategic planning. Here's how you can effectively use these numbers to drive better decisions:

1. Evaluate Asset Performance

Depreciation data helps businesses assess the efficiency and performance of their assets, guiding decisions about repair, replacement, or disposal.

- Identify Underperforming Assets: Assets that depreciate faster than expected or require frequent repairs may no longer be cost-effective to retain.

- Example: If a delivery truck incurs high maintenance costs and has little remaining book value, replacing it may be more economical.

- Optimize Usage: Analyzing depreciation rates can also reveal if assets are underused, allowing companies to redistribute or lease them to maximize their utility.

2. Plan for Asset Replacement

Knowing an asset's depreciation schedule provides insight into when it will reach the end of its useful life, enabling better planning for replacements.

- Replacement Timelines: Businesses can avoid operational disruptions by scheduling replacements before assets become non-functional.

- Example: If a piece of machinery is nearing the end of its useful life in five years, a company can start allocating funds for its replacement well in advance.

- Technology Upgrades: Depreciation schedules can also signal when to replace assets to stay competitive, especially in industries where technological advancements are frequent.

3. Improve Budgeting and Cash Flow Management

Depreciation numbers are invaluable for financial planning, as they provide a predictable expense that can be factored into budgets and forecasts.

- Budget Allocation: By anticipating depreciation expenses, businesses can allocate resources more effectively, ensuring they have sufficient funds for asset-related costs like maintenance or upgrades.

- Cash Flow Planning: Depreciation expenses, while non-cash, can help companies project cash flow more accurately by identifying future spending needs tied to asset management.

4. Enhance Tax Planning

Depreciation offers significant tax benefits, and using this data strategically can reduce tax liabilities and improve cash retention.

- Maximize Deductions: Businesses can plan their tax strategy around depreciation schedules, taking advantage of accelerated methods like bonus depreciation to reduce taxable income in early years.

- Example: A company might choose to use a double-declining balance method for assets expected to lose value quickly, optimizing immediate tax savings.

- Timing Asset Purchases: Understanding depreciation rules can help businesses decide when to purchase assets to maximize tax benefits. Buying equipment near the end of a fiscal year, for instance, may allow a company to claim a partial year’s depreciation.

5. Support Decision-Making in Financing and Investments

Depreciation data provides critical information for evaluating the financial viability of investments and securing financing.

- Investment Decisions: Depreciation calculations can reveal the total cost of ownership (TCO) for assets, helping businesses decide whether purchasing or leasing an asset is more advantageous.

- Loan Applications: Depreciation figures are essential when presenting financial statements to lenders, as they demonstrate prudent asset management and realistic valuations for collateral.

6. Track and Manage Intangible Assets

For businesses with significant intangible assets like patents, trademarks, or software, depreciation (or amortization) data is critical for strategic management.

- License Renewals and Expirations: Businesses can plan for renewing or replacing intangible assets as their value diminishes over time.

- Example: A company with a patent nearing the end of its useful life may decide to invest in new R&D to stay competitive.

- Valuation Adjustments: Understanding how intangible assets depreciate ensures accurate valuation, which is particularly important for mergers, acquisitions, or investment decisions.

7. Improve Profitability Analysis

Incorporating depreciation expenses into profitability analysis ensures that product pricing and cost management strategies are comprehensive and realistic.

- Product Pricing: Businesses can factor depreciation into their pricing models, ensuring that each unit sold covers not only production costs but also asset usage.

- Example: A manufacturer might include a portion of machinery depreciation in thecost of goods sold (COGS) to ensure profitability.

- Operational Efficiency: If high depreciation costs are eroding profits, businesses can evaluate whether upgrading to more efficient assets might improve their bottom line.

8. Facilitate Financial Reporting and Compliance

Accurate depreciation calculations are essential for creating reliable financial statements and meeting regulatory requirements.

- Audit Preparedness: Depreciation figures support transparent reporting, reducing the risk of disputes during audits by tax authorities or external auditors.

- Compliance with Standards: By adhering to accounting standards like GAAP (Generally Accepted Accounting Principles) or IFRS (International Financial Reporting Standards) as mentioned above, businesses demonstrate financial accountability and professionalism.

9. Inform Strategic Business Decisions

Depreciation data often influences broader strategic choices, such as expansion, diversification, or cost-cutting initiatives.

- Capacity Planning: If depreciation data shows that production assets are nearing obsolescence, businesses may decide to invest in modern facilities to meet future demand.

- Outsourcing or In-House Production: Companies may also evaluate whether outsourcing certain processes is more cost-effective than maintaining depreciating equipment.

10. Communicate Value to Stakeholders

Depreciation figures provide a clear understanding of asset value and usage, which is essential for communication with stakeholders, including investors, partners, and board members.

- Transparency: Clear depreciation schedules and calculations show stakeholders that the company is managing its resources responsibly.

- Investment Appeal: Accurate valuation of assets can increase investor confidence, particularly during funding rounds or public offerings.

After calculating depreciation, the key is to use the numbers proactively rather than letting them sit as static figures on financial statements. From strategic asset management and budgeting to enhancing profitability and ensuring compliance, depreciation data serves as a foundation for well-informed decision-making. By leveraging these insights, businesses can optimize their operations, maximize efficiency, and achieve sustainable growth.

Conclusion

Depreciation is an essential aspect of business accounting, providing a systematic way to allocate the cost of an asset over time. Understanding the different methods, the assets that qualify for depreciation, and the benefits it offers in terms of tax savings and financial reporting can help businesses make informed decisions. By adhering to accounting standards such as GAAP or IFRS and using tools like depreciation schedules, companies can ensure they are managing their assets efficiently and accurately. Ultimately, depreciation plays a critical role in the financial health and strategic planning of any organization.

If you’re looking to deepen your understanding of financial concepts like depreciation, our Accounting and Finance for Non-Financial Professionals course is designed to equip you with the practical skills you need. Gain insights into financial principles, learn how to analyze reports, and make more confident business decisions. Join us today and take the next step toward financial proficiency, even if you don’t have an accounting background!

This Training course is aimed at business professionals who need to understand how finance works. Financial information can provide a clear picture of how to increase profitability, decrease costs, and meet targets in any business. It is very crucial that