Introduction

Real estate accounting is a specialized field that plays a crucial role in the real estate industry, ensuring the accurate tracking, reporting, and analysis of financial transactions related to property assets. This area of accounting involves unique challenges, such as managing complex transactions, adhering to industry-specific regulations, and navigating intricate tax implications. Given the significant capital involved and the long-term nature of real estate investments, effective accounting practices are essential for maintaining financial health, ensuring regulatory compliance, and making informed business decisions. Understanding the key principles and practices of real estate accounting is vital for professionals in this industry to maximize profitability and minimize risks.

Key Concepts in Real Estate Accounting

Real estate accounting encompasses various specialized practices tailored to the unique nature of real estate assets and transactions. At its core, real estate assets are defined as properties held for various purposes, including investment, development, or resale. These assets may include land, buildings, residential properties, commercial properties, and industrial facilities. The diversity of these assets underscores the complexity of real estate accounting, as each type may have different accounting requirements.

Understanding the types of real estate transactions is crucial for accurate financial reporting and analysis. These transactions can be broadly categorized into property acquisitions,property sales, lease agreements,property development, and investment in real estate trusts (REITs). Each transaction type has specific accounting treatments that need to be accurately recorded to reflect the financial health and performance of real estate entities. For instance, property acquisitions typically involve significant capital investments and may require proper allocation of costs such as purchase price, legal fees, and improvement expenses. On the other hand, property sales necessitate the recognition of revenue and any corresponding gains or losses on the sale of the property.

Revenue recognition in real estate is another critical concept that requires careful attention to detail. Unlike other industries where revenue is recognized when goods are delivered or services are performed, real estate revenue recognition can be more complex due to the long-term nature of many real estate transactions. Depending on the nature of the transaction, revenue may be recognized at different stages, such as upon the completion of a sale, over the lease term, or as construction milestones are met in the case of development projects. Real estate accountants must be familiar with the specific criteria for revenue recognition under relevant accounting standards, such as IFRS 15 or ASC 606, to ensure accurate financial reporting.

Key points to consider in real estate revenue recognition include:

- Sales of Property: Revenue is recognized when the control of the property is transferred to the buyer, which typically coincides with the closing of the sale.

- Leases: Rental income is recognized on a straight-line basis over the lease term unless another systematic basis better represents the time pattern in which the benefit derived from the leased property is diminished.

- Construction Contracts: Revenue may be recognized over time if certain criteria are met, such as the buyer having control over the work in progress, or at a point in time upon the completion of significant milestones.

Establishing contracts for all involved parties is important in any industry. This is especially true in the construction industry, as the nature of this work is often highly unpredictable, and disputes can often arise due to varying factors. Work-related disputes have the potential

These key concepts form the foundation of real estate accounting and are essential for ensuring that financial statements accurately reflect the economic realities of real estate operations.

Basic Principles of Real Estate Accounting

The basic principles of real estate accounting provide the foundation for accurately capturing and reporting financial transactions within the industry. One of the fundamental decisions in real estate accounting is whether to use the accrual basis or cash basis of accounting. Under theaccrual basis of accounting, revenues and expenses are recorded when they are earned or incurred, regardless of when cash is actually exchanged. This method provides a more accurate picture of a company's financial position and performance over time, particularly for businesses with long-term projects, such as real estate development. On the other hand, thecash basis of accounting records revenues and expenses only when cash is received or paid. While simpler to implement, the cash basis can sometimes present a distorted view of financial health, especially in an industry where large, infrequent transactions are common.

Depreciation and amortization are critical processes in real estate accounting, particularly given the significant investments made in tangible and intangible assets. Depreciation is applied to tangible assets like buildings and improvements, allowing for the systematic allocation of the asset's cost over its useful life. This process not only reflects the wear and tear on the property but also provides a tax benefit by reducing taxable income. Amortization, meanwhile, applies to intangible assets such as leasehold improvements or goodwill. Both depreciation and amortization require careful estimation of useful life and residual value, as these assumptions can significantly impact financial statements and tax obligations.

Another key principle in real estate accounting is property valuation and impairment. Property valuation involves determining the fair market value of real estate assets, which can fluctuate due to changes in market conditions, location desirability, and the overall economic environment. Accurately valuing properties is essential for financial reporting, tax assessments, and making informed investment decisions.Impairment occurs when the carrying amount of a property exceeds its recoverable amount, indicating that the asset has lost value. In such cases, an impairment loss must be recognized in the financial statements, which can affect profitability and asset valuations. Impairment is particularly relevant in real estate due to the potential for significant declines in property values, especially during economic downturns or due to changes in property use or zoning laws.

Key points to consider in these principles include:

- Accrual vs. Cash Basis Accounting:

- Accrual basis provides a more comprehensive view of financial performance, especially for long-term projects.

- Cash basis is simpler but may not accurately reflect financial health.

- Depreciation and Amortization:

- Depreciation spreads the cost of tangible assets over their useful life.

- Amortization applies to intangible assets and reduces taxable income.

- Property Valuation and Impairment:

- Accurate property valuation is critical for financial reporting and investment decisions.

- Impairment must be recognized when a property's value falls below its carrying amount.

Summary of Basic Principles in Real Estate Accounting

Principle | Summary |

Accrual vs. Cash Basis Accounting | Accrual basis records revenues/expenses when earned/incurred, providing a comprehensive view, especially for long-term projects. Cash basis records when cash is exchanged, but may distort financial health. |

Depreciation and Amortization | Depreciation spreads the cost of tangible assets (like buildings) over their useful life, reducing taxable income. Amortization applies to intangible assets (like goodwill). |

Property Valuation and Impairment | Property valuation assesses the fair market value, crucial for reporting and investment. Impairment recognizes losses when property value falls below its carrying amount. |

Understanding these basic principles is essential for managing the financial aspects of real estate assets and ensuring compliance with relevant accounting standards. They help ensure that financial statements present a true and fair view of a company's financial position, enabling better decision-making for stakeholders.

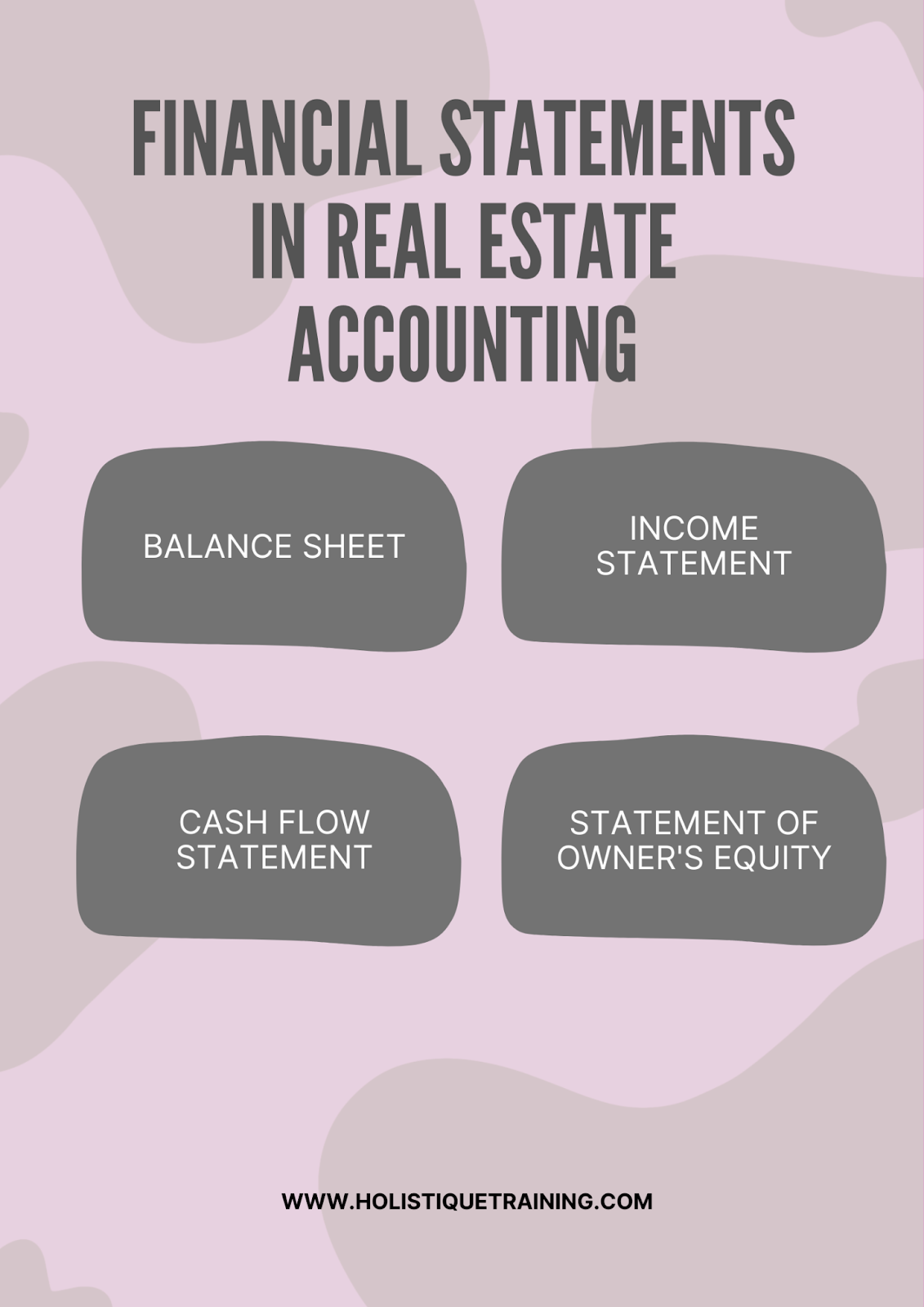

Financial Statements in Real Estate Accounting

Financial statements are the backbone of real estate accounting, providing a comprehensive view of an entity's financial health and performance. The four primary financial statements—Balance Sheet,Income Statement,Cash Flow Statement, and Statement of Owner's Equity—each play a crucial role in conveying different aspects of a real estate company's financial activities.

The Balance Sheet presents a snapshot of a real estate company's financial position at a specific point in time. It details the company's assets, liabilities, and equity, giving stakeholders a clear picture of what the company owns and owes. In real estate accounting, assets typically include properties (both developed and under development), cash, accounts receivable, and investments in real estate ventures. Liabilities may encompass mortgages, loans, accounts payable, and other obligations related to property ownership or development. Equity represents the residual interest in the assets of the company after deducting liabilities and includes contributions by owners and retained earnings. The balance sheet is essential for evaluating the liquidity, solvency, and overall financial stability of a real estate company.

The Income Statement, also known as the profit and loss statement, provides a summary of the company's revenues, expenses, and profits over a specific period, typically a quarter or year. In the real estate industry, revenues might come from property sales, rental income, or service fees, while expenses could include property management costs, depreciation, interest on loans, and taxes. The income statement is vital for assessing the profitability of a real estate business and understanding the factors driving income and expenses. It helps stakeholders determine whether the company is generating sufficient revenue to cover its costs and achieve a profit.

The Cash Flow Statement tracks the movement of cash in and out of the real estate business over a period. It is divided into three sections: operating activities, investing activities, and financing activities. For a real estate company, cash inflows from operating activities might include rental income or proceeds from property sales, while cash outflows could involve payments for property maintenance, salaries, and taxes. Investing activities generally relate to the acquisition or sale of properties, while financing activities include borrowing or repaying loans and distributing dividends to owners. The cash flow statement is crucial for understanding how a real estate company manages its cash, ensuring it has enough liquidity to meet its obligations and invest in future opportunities.

The Statement of Owner's Equity reflects changes in the owner's equity during the accounting period. In real estate accounting, this statement shows how the equity balance has been affected by various factors such as net income, owner contributions, withdrawals, and dividends. It provides insight into how the ownership stake in the company has evolved over time. This statement is particularly important for real estate companies where equity investments are significant, as it shows the return on investment for owners and highlights any distributions made to them.

Key points to consider for each financial statement include:

- Balance Sheet:

- Assets include properties, cash, and investments.

- Liabilities encompass mortgages, loans, and payables.

- Equity reflects ownership interest and retained earnings.

- Income Statement:

- Revenue sources include property sales and rental income.

- Expenses cover property management, depreciation, and taxes.

- Net profit or loss indicates overall financial performance.

Property management is crucial in the world of real estate. Effective property management will ensure that all tenants' needs are met, that the building remains fully compliant with legal regulations, and that finances are accurately managed. Property management should be conducted

- Cash Flow Statement:

- Operating activities cover day-to-day cash inflows and outflows.

- Investing activities relate to property acquisitions and sales.

- Financing activities include loans and equity transactions.

- Statement of Owner's Equity:

- Tracks changes in equity due to net income, contributions, and distributions.

- Shows the impact of financial performance on ownership value.

Together, these financial statements provide a holistic view of a real estate company's financial condition, guiding decision-making and strategic planning for stakeholders.

Accounting for Real Estate Transactions

Real estate transactions are at the heart of real estate accounting, encompassing a range of activities from property acquisitions to managing rental income. Each type of transaction requires careful accounting to ensure accurate financial reporting and compliance with relevant regulations.

The purchase and sale of properties is one of the most significant transactions in real estate accounting. When purchasing a property, all costs associated with the acquisition, such as the purchase price, legal fees, title transfer costs, and any immediate improvements, are capitalized as part of the property's value on the balance sheet. These capitalized costs are then subject to depreciation over the useful life of the property, except for land, which is not depreciated. When a property is sold, the sale proceeds are recognized as revenue, and the property's carrying value, including any accumulated depreciation, is deducted from this amount to calculate the gain or loss on the sale. This gain or loss is then reported on the income statement, providing insight into the profitability of the transaction.

Lease accounting is another critical aspect of real estate accounting, particularly with the advent of new standards such as IFRS 16 and ASC 842, which have significantly impacted how leases are reported. Under these standards, leases are classified as either finance leases (formerly capital leases) or operating leases. For finance leases, the lessee recognizes the leased asset and a corresponding liability on the balance sheet, with interest expense and depreciation recorded over the lease term. Operating leases, on the other hand, are generally kept off the balance sheet, with lease payments expensed as incurred. For lessors, lease accounting involves recognizing rental income and, depending on the lease type, either retaining the leased asset on the balance sheet or derecognizing it in favor of a receivable.

Property development and construction costs are vital considerations in real estate accounting, especially for companies involved in building new properties or renovating existing ones. Development costs include expenditures such as land acquisition, construction materials, labor, and architectural fees. These costs are capitalized as part of the property’s value and only expensed once the property is completed and ready for its intended use. During the construction phase, interest costs on borrowed funds used for development can also be capitalized, reducing the impact on the income statement. Once the property is completed, it begins to be depreciated, and any further development costs are expensed as incurred.

Managing rental income and expenses is a key component of real estate accounting for companies that hold properties for lease. Rental income is recognized on a straight-line basis over the lease term unless another method better represents the time pattern of earning the income. This approach ensures that income is recorded evenly throughout the lease period, providing a stable revenue stream on the income statement. Rental expenses, including property management fees, maintenance costs, property taxes, and utilities, are expensed as incurred. Properly managing these income and expense streams is crucial for maintaining profitability and ensuring accurate financial reporting.

Key points to consider in accounting for real estate transactions include:

- Purchase and Sale of Properties:

- Capitalize acquisition costs, including purchase price, legal fees, and improvements.

- Recognize gain or loss on sale by comparing sale proceeds with the property's carrying value.

- Lease Accounting:

- Classify leases as finance or operating, with different treatment for each.

- Lessees recognize leased assets and liabilities for finance leases, while lessors recognize rental income.

- Property Development and Construction Costs:

- Capitalize development costs until the property is ready for use.

- Capitalize interest on borrowed funds during construction, with depreciation beginning post-completion.

- Managing Rental Income and Expenses:

- Recognize rental income on a straight-line basis over the lease term.

- Expense rental-related costs, including management fees, maintenance, and taxes, as incurred.

These aspects of real estate transaction accounting are essential for providing accurate and meaningful financial information to stakeholders, ensuring that real estate entities can effectively manage their operations and make informed decisions.

Tax Considerations in Real Estate Accounting

Tax considerations play a significant role in real estate accounting, impacting everything from property ownership and operations to the sale of assets. Understanding these tax implications is essential for maximizing returns and ensuring compliance with tax regulations.

Property taxes are a major expense for real estate owners and are typically assessed annually based on the property's assessed value. These taxes are levied by local governments and vary widely depending on the property's location, size, and use. Property taxes are considered operating expenses and are recorded on the income statement as they are incurred. Failure to pay property taxes can result in penalties, interest charges, or even the loss of the property through tax liens. It’s crucial for real estate companies to accurately calculate and regularly pay these taxes to avoid any legal complications or financial losses. Additionally, property tax expenses can often be deducted from taxable income, reducing the overall tax burden on the real estate entity.

Capital gains tax is another critical consideration in real estate accounting, particularly when selling property. Capital gains tax is imposed on the profit realized from the sale of a property, which is calculated as the difference between the sale price and the property's adjusted basis (the original purchase price plus any capital improvements made). There are typically two types of capital gains tax: short-term and long-term. Short-term capital gains, applied to properties held for less than a year, are taxed at higher ordinary income tax rates, while long-term capital gains, for properties held longer than a year, benefit from lower tax rates. Understanding the timing of property sales and structuring transactions to qualify for long-term capital gains treatment can significantly reduce tax liabilities and enhance overall profitability.

Depreciation and tax deductions are powerful tools in real estate accounting that can help reduce taxable income. Depreciation allows real estate owners to recover the cost of a property over its useful life through annual deductions. For tax purposes, the Internal Revenue Service (IRS) provides specific guidelines on the depreciable life of various property types—27.5 years for residential rental property and 39 years for commercial property, for example. Depreciation is a non-cash expense, meaning it reduces taxable income without affecting the company’s cash flow. However, when the property is eventually sold, the previously taken depreciation must be "recaptured" and taxed as ordinary income, which is a crucial consideration in tax planning.

In addition to depreciation, other tax deductions are available to real estate owners, such as deductions for mortgage interest, property management fees, repair and maintenance costs, and insurance premiums. These deductions further reduce taxable income, making real estate an attractive investment from a tax perspective. However, it’s essential for real estate companies to keep detailed records and comply with IRS guidelines to ensure that all deductions are valid and substantiated.

Key points to consider in tax considerations for real estate accounting include:

- Property Taxes:

- Assessed annually based on the property's value and recorded as operating expenses.

- Deductible from taxable income, reducing overall tax liability.

- Capital Gains Tax:

- Imposed on the profit from property sales, with different rates for short-term and long-term gains.

- Strategic timing of property sales can minimize tax liabilities.

- Depreciation and Tax Deductions:

- Depreciation reduces taxable income over the property’s useful life but requires recapture upon sale.

- Additional deductions, such as mortgage interest and maintenance costs, can further reduce taxable income.

Understanding these tax considerations is essential for real estate companies to optimize their tax positions, enhance cash flow, and ensure compliance with tax regulations. Proper tax planning can significantly impact the financial success of real estate investments.

Taxation is an important aspect every organisation should be aware of and competent in. Regulations are constantly being created and updated to maintain an efficient practice and protect all parties involved. When it comes to taxation laws, it is crucial

Common Challenges in Real Estate Accounting

Real estate accounting is a complex and dynamic field, with several challenges that professionals in the industry must navigate. These challenges stem from the nature of real estate transactions, the need to comply with various regulations and standards, and the intricacies of tax implications.

Managing complex transactions is one of the most significant challenges in real estate accounting. Real estate deals often involve multiple parties, intricate financial arrangements, and substantial amounts of capital. These transactions can include property acquisitions and sales, lease agreements, financing arrangements, and property development projects, each with its own accounting requirements. For instance, accurately recognizing revenue from property sales, allocating costs among various phases of a development project, or accounting for lease modifications can be particularly challenging. The complexity increases when transactions involve multiple jurisdictions or entities, requiring careful consideration of currency conversions, differing accounting practices, and intercompany eliminations. To manage these complexities effectively, real estate companies need robust accounting systems, skilled professionals, and meticulous record-keeping to ensure accurate and timely financial reporting.

Compliance with regulations and standards is another major challenge in real estate accounting. The real estate industry is heavily regulated, with various local, national, and international laws governing property transactions, financial reporting, and tax obligations. In addition to general accounting principles, real estate companies must adhere to specific standards such as IFRS (International Financial Reporting Standards) or GAAP (Generally Accepted Accounting Principles), depending on their jurisdiction. These standards include detailed guidance on revenue recognition, lease accounting, and fair value measurements, which can be complex to implement and maintain. Moreover, regulatory bodies frequently update these standards, requiring continuous education and adaptation by real estate accounting professionals. Non-compliance can result in financial penalties, legal issues, and damage to a company’s reputation, making it essential for real estate firms to stay abreast of regulatory changes and ensure strict adherence to applicable standards.

Navigating tax implications in real estate accounting is also a significant challenge, given the intricate and often-changing tax laws that impact real estate transactions. Real estate companies must consider property taxes, capital gains taxes, and the tax treatment of depreciation and other deductions, each of which has specific rules and implications. For example, the tax treatment of income from rental properties differs from that of income from property sales, and navigating these distinctions requires a deep understanding of tax laws and careful planning. Additionally, real estate companies must be aware of tax incentives, such as 1031 exchanges in the U.S., which allow for the deferral of capital gains taxes when proceeds from a property sale are reinvested in similar properties. However, taking advantage of these incentives requires precise timing and documentation, adding to the complexity of tax planning. Failure to properly account for and plan around tax implications can lead to unexpected liabilities and reduced profitability.

Key challenges in real estate accounting include:

- Managing Complex Transactions:

- Accounting for property acquisitions, sales, leases, and developments.

- Handling transactions involving multiple entities or jurisdictions.

- Compliance with Regulations and Standards:

- Adhering to IFRS,GAAP, and other relevant accounting standards.

- Staying updated with changes infinancial reporting requirements.

This course is designed to bridge the gap between theoretical knowledge of International Financial Reporting Standards (IFRS) and their practical application in real-world financial reporting. Rather than focusing solely on definitions and rules, the programme emphasises interpretation, professional judgement, and implementation of key IFRS requirements in day-to-day

- Navigating Tax Implications:

- Managing property taxes, capital gains taxes, and depreciation.

- Utilizing tax incentives and ensuring proper tax planning.

These challenges require real estate companies to employ experienced accounting professionals, invest in sophisticated accounting systems, and maintain a proactive approach to regulatory and tax developments to ensure accurate financial management and reporting.

Conclusion

In conclusion, real estate accounting is fundamental to the success of any real estate business, as it ensures accurate financial management, compliance with regulations, and effective tax planning. By mastering the complexities of managing transactions, adhering to accounting standards, and navigating tax implications, real estate professionals can enhance their financial stability and strategic decision-making. Ultimately, the ability to apply sound accounting practices not only supports day-to-day operations but also drives long-term profitability and growth in the competitive real estate market.