- Table of Contents

- What Are the Basic Concepts of Contracts in Project Management?

- What Defines a Time and Materials Contract?

- What Are the Advantages & Disadvantages of Fixed-Price Contracts?

- How Can Cost-Reimbursable Contracts Benefit Your Project?

- What Challenges Do Time and Materials Contracts Present?

- How to Choose the Best Type of Contract for Your Project?

Introduction

Exploring the intricacies of contracts in project management is fundamental to ensuring the success and smooth execution of any project. Contracts serve as the legal backbone of the project, outlining the expectations, roles, responsibilities, and financial arrangements between parties. With various types of contracts available, each with its own set of characteristics, advantages, and disadvantages, choosing the most suitable one is a critical decision that can significantly impact the project's outcome. This article delves into the basic concepts of contracts within project management, examining the defining aspects of time and materials, fixed-price, and cost-reimbursable contracts, among others. Understanding these contract types, along with their potential benefits and challenges, is essential for project managers and stakeholders to make informed decisions, aligning project goals with the appropriate contractual framework to foster transparency, risk management, and successful project delivery.

What Are the Basic Concepts of Contracts in Project Management?

In project management, contracts are formal agreements between two or more parties that define the scope of work, responsibilities, rights, and duties of each party involved in a project. These agreements are crucial for delineating expectations, ensuring legal protections, and establishing clear guidelines for the completion of the project. Here are the basic concepts of contracts in project management:

- Scope of Work (SOW): This outlines the specific tasks, deliverables, and objectives of the project, detailing what is expected to be accomplished by the contracted parties.

- Terms and Conditions: These are the legal clauses that govern the contract, including payment terms, confidentiality agreements, dispute resolution methods, and termination clauses.

- Payment Terms: This aspect specifies how and when payments will be made, including any milestones or conditions that must be met for payment to be released.

- Quality Requirements: The contract should detail the quality standards and criteria that the deliverables must meet, ensuring that the work complies with the project’s specifications.

- Timeline: A clear timeline for the project, including start and end dates, deadlines for specific deliverables, and any milestones critical to the project's progression.

- Risk Management: Contracts often include provisions for managing risks, outlining responsibilities for each party in case of unforeseen circumstances or changes in project scope.

- Change Management: This defines the process for managing changes to the project scope, timeline, or budget, including how changes will be approved and documented.

Change management protocols within an HR department are crucial for ensuring smooth transitions during organisational changes. These protocols establish systematic approaches to anticipate, plan, and implement changes effectively, minimising disruptions and maximising employee engagement and productivity. By implementing change management

- Dispute Resolution: The contract should specify how disputes will be handled, including the use of arbitration, mediation, or legal action, and the jurisdiction under which disputes will be settled.

- Termination Clause: Conditions under which the contract can be terminated by either party, including the consequences and processes for early termination.

Understanding these basic concepts is essential for effectively managing projects and ensuring that all parties are aligned with the project’s goals, responsibilities, and expectations.

This course teaches you to efficiently and effectively administer or manage a contract process. Contracts can be fraught with pitfalls and difficulties and have far-reaching legal implications. Therefore, it’s crucial to fully understand the legalities to ensure successful partnerships with vendors, service providers,

What Defines a Time and Materials Contract?

A Time and Materials (T&M) contract is defined by its flexible nature, compensating contractors based on the actual time spent working on the project and the materials used, plus a markup for overhead and profit. This type of contract is used when the scope of work is not clearly defined or is expected to change, making it difficult to estimate the total cost upfront.

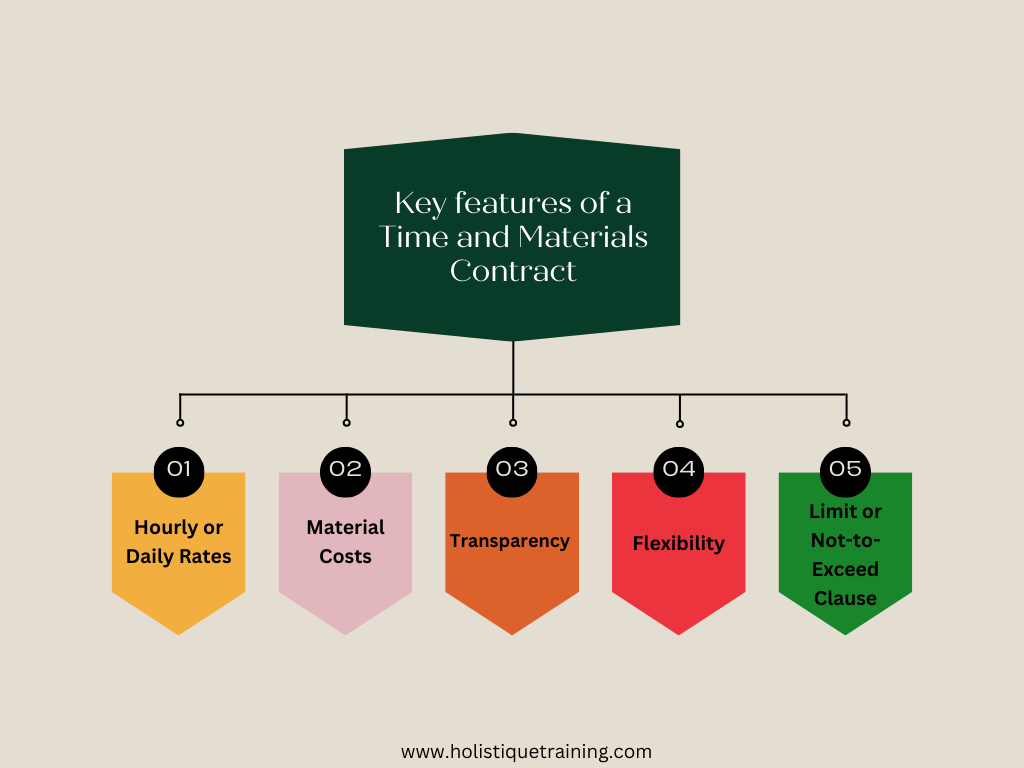

Key features of a T&M contract include:

- Hourly or Daily Rates: Payments are made to contractors based on the time spent working on the project. Rates are typically agreed upon in advance and may vary depending on the skill level of the personnel involved.

- Material Costs: The contract reimburses the cost of materials and equipment used in the project. These costs are usually marked up to cover handling and procurement.

- Transparency: Both parties agree to maintain transparency regarding the time spent on the project and materials used. This often involves regular reporting and documentation.

- Flexibility: T&M contracts allow for greater flexibility in managing project changes, as adjustments to the scope of work can be accommodated without renegotiating the entire contract.

- Limit or Not-to-Exceed Clause: To control costs, T&M contracts may include a limit or a not-to-exceed clause, capping the total expenses or specifying a maximum budget for the project.

T&M contracts are particularly suited for projects where requirements are expected to evolve or when it's challenging to define the full scope of work at the contract's outset. They provide a way to commence work quickly while maintaining the flexibility to adapt to project changes, with the understanding that risk related to cost overruns is shared between the client and the contractor.

What Are the Advantages & Disadvantages of Fixed-Price Contracts?

Fixed-price contracts involve a set amount agreed upon by both parties for the completion of a project or delivery of a product, irrespective of the actual costs incurred. Here are their advantages and disadvantages:

Advantages:

- Budget Certainty: They offer clients budget certainty, as the cost is agreed upon in advance. This makes financial planning and allocation of resources more predictable.

- Reduced Risk for Clients: Clients are protected from cost overruns since the risk of increased project costs is transferred to the contractor.

- Incentive for Efficiency: Contractors are motivated to work efficiently and control costs to maximize their profit margins , potentially leading to faster project completion.

- Simplified Contract Management: With a fixed price, contract management can be simpler for clients, as there is no need to continuously monitor actual work hours or material costs.

Disadvantages:

- Risk of Lower Quality: Contractors facing higher-than-anticipated costs might cut corners to stay within budget, potentially compromising the quality of work.

- Inflexibility: Fixed-price contracts can be inflexible, making it challenging to accommodate changes in project scope or requirements without renegotiating the contract.

- Higher Initial Prices: Contractors may quote higher prices to cover potential overruns and uncertainties, leading to higher costs for clients compared to other contract types.

- Detailed Scope Required: These contracts require a very detailed and clear project scope upfront, which can be time-consuming and difficult for projects with uncertain parameters.

- Potential for Disputes: The rigidity regarding scope and changes can lead to disputes between clients and contractors over what is included in the contract price.

Fixed-price contracts are well-suited for projects with clearly defined scopes and outcomes, where the risks associated with cost overruns are well-understood and can be accurately estimated upfront. However, they may not be ideal for projects where requirements are expected to evolve or are not fully understood at the contract's outset.

How Can Cost-Reimbursable Contracts Benefit Your Project?

Cost-reimbursable contracts, also known as cost-plus contracts, offer a payment structure where the client reimburses the contractor for all actual costs incurred during the project, plus an additional fee for profit. These contracts can be particularly beneficial for projects with undefined aspects or when scope changes are anticipated. Here is how they can benefit your project:

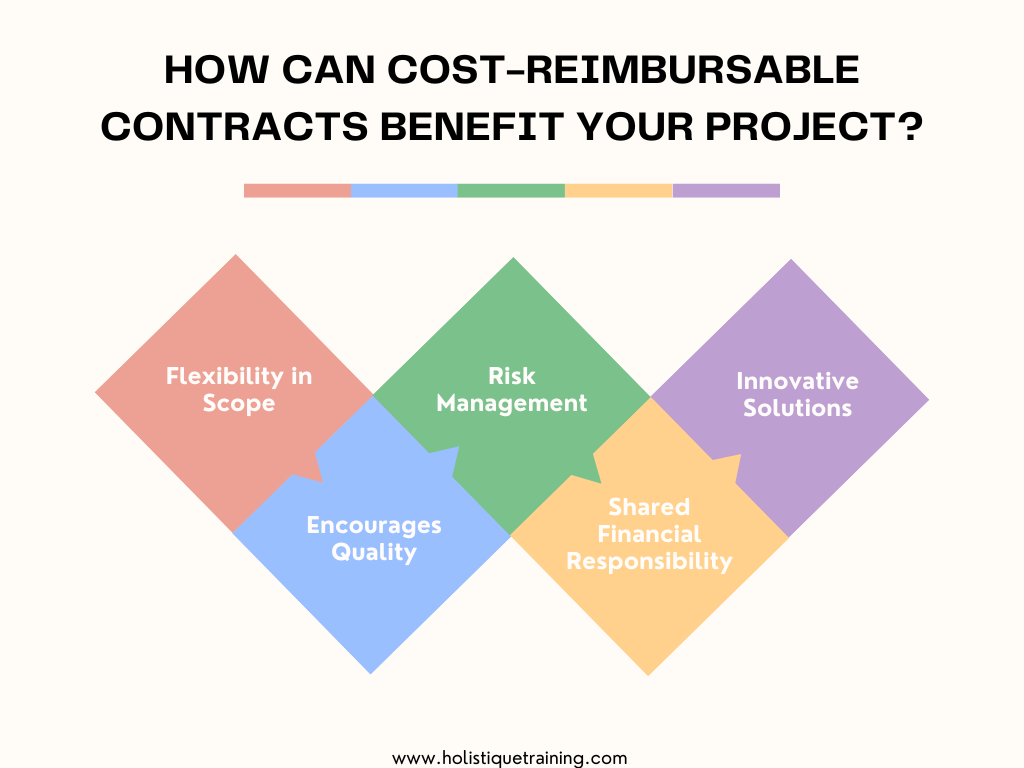

- Flexibility in Scope: They provide flexibility to adjust the project scope and requirements without renegotiating the entire contract, making them ideal for projects where the full scope isn't clear at the outset.

- Encourages Quality: Since the contractor is reimbursed for actual costs, there's an incentive to focus on quality and efficiency without the pressure to cut corners to stay within a fixed budget.

- Risk Management: The risk of cost overruns is largely transferred to the client, which can be a downside. However, this arrangement encourages close collaboration and monitoring of project progress, potentially leading to better risk management and transparency.

To manage a project effectively and achieve a positive outcome, you must understand how to identify and manage potential risks and mitigate them against a budget plan. You need to make informed and calculated decisions to benefit your department, wider business, and employees and create an

- Innovative Solutions: The flexibility associated with cost-reimbursable contracts can encourage contractors to explore innovative solutions and technologies without the constraint of a fixed budget, possibly leading to better project outcomes.

- Shared Financial Responsibility: Although the client bears the cost risks, these contracts often include clauses that cap total costs or set a guaranteed maximum price, which can help manage financial exposure while still offering contractors an incentive for cost control and efficient work.

Despite their advantages, cost-reimbursable contracts require rigorous oversight and clear communication between clients and contractors to ensure costs are controlled, and the project remains aligned with its goals. They are best suited for projects where the level of uncertainty is high, and the potential for changes during the project lifecycle is significant.

What Challenges Do Time and Materials Contracts Present?

Time and materials (T&M) contracts, while offering flexibility and simplicity for projects with uncertain scopes, present several challenges that need careful management:

- Budget Uncertainty: The biggest challenge with T&M contracts is the lack of a fixed budget, making it difficult for clients to predict the total project cost. This uncertainty can lead to budget overruns if not closely monitored.

- Monitoring and Oversight: These contracts require rigorous oversight to ensure that hours worked and materials used are accurately recorded and necessary. Without effective monitoring , there's a risk of inflated costs or inefficiencies.

- Scope Creep: The flexibility of T&M contracts can sometimes lead to scope creep, where the project's scope expands beyond the original objectives without corresponding increases in budget or timelines, affecting project outcomes.

- Reduced Incentive for Efficiency: Since contractors are paid for the time and materials used, there might be less incentive to work efficiently, potentially leading to prolonged project timelines and higher costs.

- Client-Contractor Disputes: The open-ended nature of T&M contracts can lead to disputes between clients and contractors over the necessity of work performed or the cost of materials, requiring clear communication and documentation to resolve.

To mitigate these challenges, clients and contractors must establish clear communication channels, set project management controls, and regularly review project progress against budgets and timelines. Implementing caps on total costs or defining specific deliverables within the T&M framework can also help align expectations and control costs.

How to Choose the Best Type of Contract for Your Project?

Choosing the right type of contract for your project involves evaluating the project's specific needs, risks, and objectives. Here’re steps to guide you in making an informed decision:

- Define Project Scope and Objectives: Clearly understand the project's scope, deliverables, and objectives. A well-defined scope aids in determining which contract type aligns with project goals and risk management strategies.

- Assess Project Risks: Identify potential risks, including scope changes, cost overruns, and timelines. Different contract types distribute risks differently between the client and the contractor.

- Consider the Level of Project Uncertainty: Evaluate how well you can define the project's scope and requirements upfront. Fixed-price contracts are suitable for projects with a well-defined scope, while time and materials or cost-reimbursable contracts may be better for projects where the scope is less clear.

- Evaluate Financial Constraints and Budget Flexibility: Determine the project's budget flexibility. If the budget is fixed with little room for variation, a fixed-price contract might be appropriate. If there's flexibility to accommodate changes in scope or unforeseen tasks, consider a time and materials or cost-reimbursable contract.

- Analyze Project Duration and Complexity: Long-term or complex projects might benefit from the flexibility of time and materials or cost-reimbursable contracts, allowing for adjustments as the project evolves. Shorter, less complex projects might be more suited to fixed-price contracts.

- Understand the Capabilities of Your Team and the Contractor: Assess the reliability, expertise, and past performance of the contractor. A trusted contractor might work effectively under a cost-reimbursable contract, while a fixed-price contract might be preferable when working with new contractors.

- Decide on Control and Oversight Requirements: Consider how much control and oversight you wish to retain over the project. Time and materials and cost-reimbursable contracts require more client oversight to monitor progress and costs, while fixed-price contracts offer more predictability and less daily management.

- Consult with Stakeholders: Engage with all key stakeholders, including project managers, financial officers, and legal advisors, to gather insights and considerations that might affect the contract choice.

- Review and Compare Contract Types: Examine the pros and cons of each contract type in the context of your project's specific requirements, risks, and objectives.

- Make an Informed Decision: Choose the contract type that best aligns with your project's needs, balances risks appropriately, and offers the best chance for a successful project outcome.

Table 1: Steps to Selecting the Optimal Contract Type for Your Project

Step | Considerations | Suitable Contract Types |

Define Project Scope and Objectives | Understand scope, deliverables, objectives | Depends on project goals and risk management |

Assess Project Risks | Scope changes, cost overruns, timelines | Varies; risk distribution is key |

Consider Level of Project Uncertainty | Clarity of project scope and requirements | Fixed-price for clear scopes; Time & Materials or Cost-Reimbursable for less clear scopes |

Evaluate Financial Constraints and Budget Flexibility | Budget rigidity or flexibility | Fixed-price for fixed budgets; Time & Materials or Cost-Reimbursable for flexible budgets |

Analyze Project Duration and Complexity | Length and complexity of the project | Time & Materials or Cost-Reimbursable for long/complex; Fixed-price for short/simple |

Understand the Capabilities of Your Team and the Contractor | Contractor reliability and expertise | Depends on contractor reliability |

Decide on Control and Oversight Requirements | Level of desired control and oversight | Time & Materials or Cost-Reimbursable require more oversight; Fixed-price offers predictability |

Consult with Stakeholders | Insights from project managers, financial officers, legal advisors | Varied based on stakeholder insights |

Review and Compare Contract Types | Pros and cons in context of project requirements | Critical step for making an informed choice |

Make an Informed Decision | Align contract type with project needs and risk balance | Final step to ensure project success |

Selecting the right contract type is crucial for project success, as it sets the foundation for the project's financial management, risk distribution, and relationship dynamics between the client and the contractor.

Conclusion

In conclusion, the selection of the appropriate contract type in project management is a critical decision that requires careful consideration of the project's scope, objectives, and inherent risks. Whether it’s a fixed-price, time and materials, or cost-reimbursable contract, each has its unique benefits and challenges that can significantly influence the project's financial and operational outcome. By understanding the nuances of these contract types, project managers can tailor their approach to contract selection, ensuring alignment with project goals and stakeholder expectations. Ultimately, the right contract lays the foundation for a transparent, efficient, and mutually beneficial relationship between parties, steering the project towards success and fostering a culture of trust and collaboration.

Throughout this course, you’ll gain the essential skills and knowledge you need to win a contract with other providers successfully. You’ll understand how to successfully implement a new contract into your business model and follow through to deliver your promises to your client. You will discover