Introduction

Demand and supply are foundational concepts in market economics, governing the behavior of buyers and sellers in a marketplace. Demand refers to the quantity of a good or service that consumers are willing and able to purchase at various price levels, while supply represents the quantity that producers are willing to sell. The interaction between these forces determines market prices and the allocation of resources. Understanding demand and supply is crucial for analyzing how markets function, predicting price movements, and making informed economic decisions that impact both businesses and consumers.

Understanding Demand

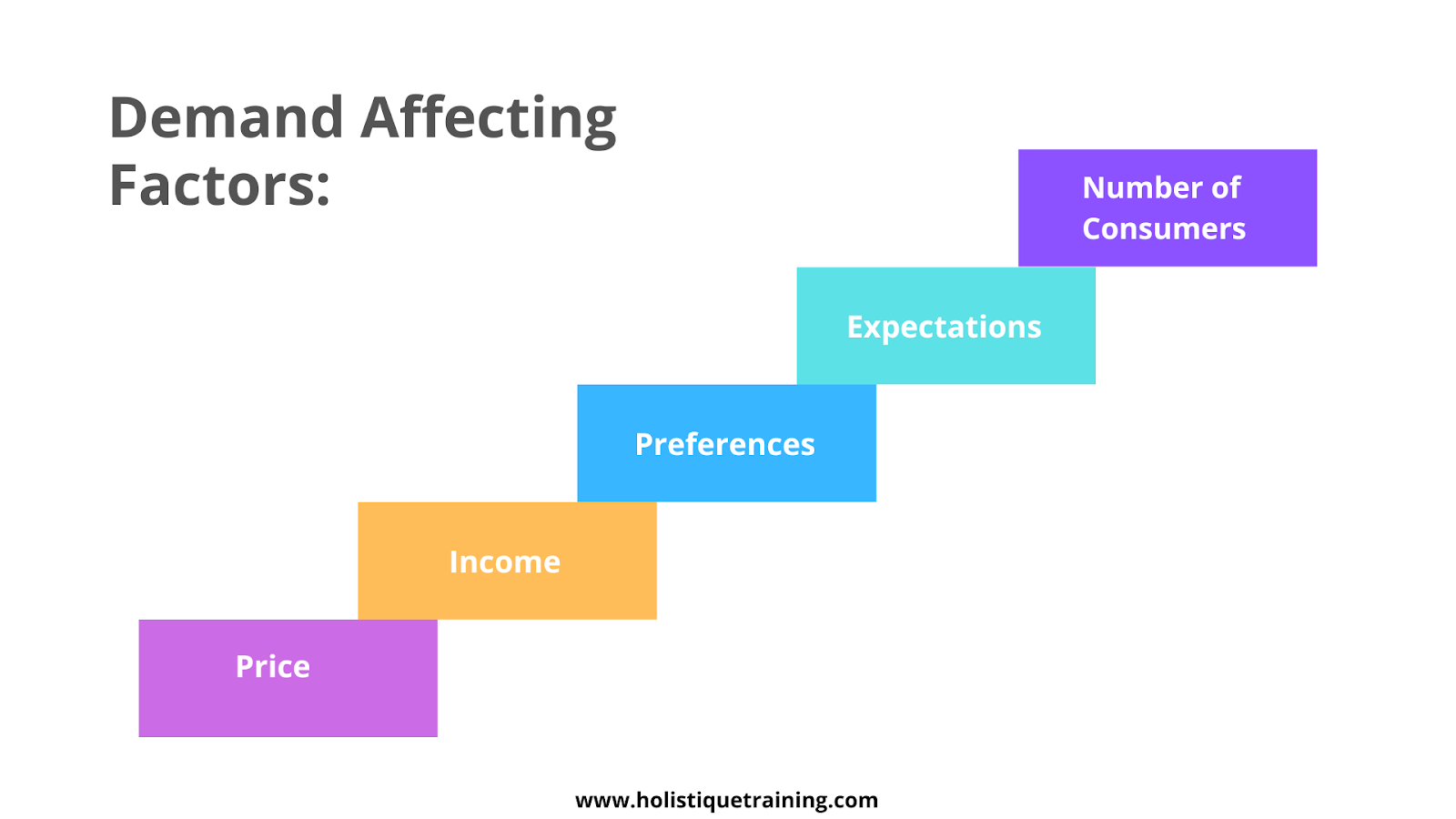

Demand is a fundamental concept in economics that refers to the quantity of a good or service that consumers are willing and able to purchase at a given price over a specific period. It encompasses various aspects and factors that influence consumer behavior and market dynamics. The law of demand states that, all else being equal, as the price of a good decreases, the quantity demanded increases, and vice versa. This inverse relationship is depicted by the demand curve, which typically slopes downward from left to right, reflecting that lower prices lead to higher quantities demanded. Several factors affect demand, including:

- Price: The primary determinant of demand. According to the law of demand, as prices fall, demand generally increases, and as prices rise, demand typically decreases.

- Income: Changes in consumer income can shift demand. Generally, an increase in income boosts demand for normal goods, while demand for inferior goods might decrease.

- Preferences: Consumer preferences and tastes can significantly affect demand. A shift in consumer preferences towards a particular good increases its demand.

- Expectations: Future expectations about prices, income, or availability can impact current demand. For instance, if consumers expect prices to rise in the future, they may increase current demand.

- Number of Consumers: An increase in the number of consumers in a market generally raises the overall demand for goods and services.

Demand elasticity measures how sensitive the quantity demanded is to changes in price. If demand is elastic, a small change in price leads to a significant change in quantity demanded. Conversely, if demand is inelastic, quantity demanded is less responsive to price changes. Understanding these concepts is crucial for businesses and policymakers to anticipate market behavior, set pricing strategies, and forecast economic conditions.

Demand planning is the cross-functional process of meeting customer demand while managing inventory levels and avoiding supply chain disruptions. It is essential to ensure high customer satisfaction levels, reduce operating costs, and free up working capital. This course provides you

Understanding Supply

Supply is a core economic concept that describes the quantity of a good or service that producers are willing and able to offer for sale at a given price over a specific period. It reflects how production decisions and market conditions influence the availability of goods and services in the market. The law of supply asserts that, all else being equal, as the price of a good rises, the quantity supplied increases, and as the price falls, the quantity supplied decreases. This direct relationship is illustrated by the supply curve, which generally slopes upward from left to right, indicating that higher prices incentivize producers to supply more. Several key factors affect supply, including:

- Production Costs: Changes in the costs of inputs, such as labor, raw materials, and energy, can significantly impact supply. Higher production costs typically reduce supply, while lower costs increase it.

- Technology: Advances in technology can enhance production efficiency and reduce costs, thereby increasing supply. Technological improvements often lead to a more efficient production process, allowing producers to offer more goods at lower prices.

- Number of Producers: An increase in the number of producers in a market generally boosts the overall supply of a good or service, as more firms compete to offer the product.

- Expectations: Producers’ expectations about future prices can influence current supply. If producers expect prices to rise, they may withhold current supply to sell at higher future prices, reducing current supply.

- Prices of Related Goods: The prices of related goods can affect supply. For instance, if the price of a substitute good rises, producers might shift their resources to produce that good instead, reducing the supply of the original product.

Supply elasticity measures how responsive the quantity supplied is to changes in price. If supply is elastic, a small change in price results in a significant change in quantity supplied. In contrast, if supply is inelastic, quantity supplied does not change much with price fluctuations. Understanding these factors and elasticity helps businesses and policymakers manage production strategies, predict market outcomes, and make informed economic decisions.

Interaction of Demand and Supply

The interaction between demand and supply determines the equilibrium in a market, which is crucial for understanding market dynamics and price stability. Market equilibrium occurs when the quantity demanded by consumers equals the quantity supplied by producers at a particular price level. At this point, there is neither a surplus nor a shortage of goods. The market clearing price is the price at which this equilibrium is achieved, effectively balancing supply and demand. Key concepts related to the interaction of demand and supply include:

- Surplus: A surplus occurs when the quantity supplied exceeds the quantity demanded at a given price. This typically happens when the price is set above the equilibrium level. Producers may experience excess inventory, leading to downward pressure on prices as sellers attempt to reduce their stock.

- Shortage: A shortage arises when the quantity demanded exceeds the quantity supplied at a particular price. This situation often occurs when prices are set below the equilibrium level. Consumers may struggle to purchase the product, leading to upward pressure on prices as demand outstrips supply.

- Shifts in Demand and Supply Curves: Changes in market conditions can lead to shifts in the demand and supply curves:

- Demand Curve Shifts: Factors such as changes in consumer preferences, income levels, or expectations can shift the demand curve to the right (increase in demand) or left (decrease in demand).

- Supply Curve Shifts: Factors such as changes in production technology, input prices, or the number of producers can shift the supply curve to the right (increase in supply) or left (decrease in supply).

When either the demand or supply curve shifts, the market equilibrium price and quantity will change. For instance, an increase in demand, with supply held constant, will lead to a higher equilibrium price and quantity. Conversely, an increase in supply, with demand held constant, will lead to a lower equilibrium price and a higher quantity.

Understanding these interactions helps businesses and policymakers anticipate market changes, adjust strategies, and maintain balance in the marketplace.

Table: Comparison of Key Concepts in the Interaction of Demand and Supply

Concept | Description | Impact on Market |

Market Equilibrium | Occurs when the quantity demanded equals the quantity supplied at a particular price. | No surplus or shortage; stable prices and balanced market. |

Surplus | When quantity supplied exceeds quantity demanded at a given price. | Downward pressure on prices as producers reduce inventory. |

Shortage | When quantity demanded exceeds quantity supplied at a given price. | Upward pressure on prices as consumers compete for limited goods. |

Shifts in Demand Curve | Changes due to factors like consumer preferences, income, or expectations. | Rightward shift increases demand (higher price and quantity); leftward shift decreases demand (lower price and quantity). |

Shifts in Supply Curve | Changes due to factors like production technology, input costs, or the number of producers. | Rightward shift increases supply (lower price and higher quantity); leftward shift decreases supply (higher price and lower quantity). |

Impact of Curve Shifts on Equilibrium | Shifts in demand or supply curves change the equilibrium price and quantity in the market. | Increase in demand leads to higher price and quantity; increase in supply leads to lower price and higher quantity. |

Impact on Market Prices

Market prices are influenced by a variety of factors and mechanisms that reflect changes in supply and demand dynamics. Understanding these influences is crucial for businesses and policymakers to manage economic outcomes effectively. Key aspects of how market prices are impacted include:

- Price Adjustment Mechanisms: Prices in a market are primarily adjusted through the interaction of supply and demand. When there is a surplus, producers may lower prices to increase sales and reduce excess inventory. Conversely, during a shortage, prices are likely to rise as consumers are willing to pay more to secure limited goods. This price adjustment process helps restore market equilibrium by aligning supply with demand. The market mechanism operates to balance out any discrepancies between quantity demanded and quantity supplied.

- Influence of External Shocks: External shocks, such as natural disasters, geopolitical events, or sudden economic changes, can significantly impact market prices. For example:

- Natural Disasters: Events like hurricanes or earthquakes can disrupt supply chains, reduce production capabilities, and cause shortages, leading to increased prices.

- Geopolitical Events: Conflicts or trade policies can affect the availability of goods and resources, influencing supply and driving up prices.

- Economic Changes: Fluctuations in currency exchange rates, inflation, or changes in global economic conditions can affect both supply and demand, leading to volatility in market prices.

- Government Interventions and Price Controls: Governments may intervene in markets through various measures to influence prices and stabilize the economy. Common interventions include:

- Price Controls: Governments may impose price ceilings (maximum allowable prices) or price floors (minimum allowable prices) to protect consumers or producers. For example, a price ceiling on essential goods can prevent prices from rising too high during shortages, while a price floor can ensure that producers receive a minimum income.

- Subsidies: Providing subsidies to producers can lower production costs, increase supply, and stabilize or lower market prices.

- Taxes and Tariffs: Imposing taxes or tariffs on imported goods can affect prices by increasing costs for consumers and altering supply dynamics.

These mechanisms and interventions play a critical role in shaping market prices, affecting consumer behavior, and influencing the overall economic environment. Understanding these factors helps in anticipating price movements and making informed decisions in both business and policy contexts.

Implications for Businesses and Consumers

The interaction of demand and supply, along with market price adjustments, has significant implications for both businesses and consumers. These dynamics influence strategic decisions, market behavior, and economic well-being.

- Strategic Business Decisions:

- Pricing Strategies: Businesses must continuously monitor supply and demand conditions to set optimal prices. Pricing strategies, such as dynamic pricing or discounting, are employed to manage demand and respond to changes in market conditions. For example, during periods of high demand or limited supply, businesses may raise prices to maximize profits or manage inventory levels.

Understanding pricing, trade, and the economic framework is crucial for businesses navigating the complexities of the global marketplace. This comprehensive course delves into the intricacies of pricing strategies, shedding light on the various factors influencing product and service pricing in dynamic economic environments.

- Production Planning: Understanding demand patterns helps businesses plan their production schedules and inventory levels effectively. Companies may adjust their production rates, invest in new technologies, or modify their supply chain strategies to align with anticipated changes in demand and supply.

- Market Expansion: Businesses often use demand and supply analyses to explore new markets or product lines. Identifying areas with high demand or potential supply advantages can guide decisions about entering new markets or diversifying product offerings.

- Risk Management: External shocks and price fluctuations require businesses to develop risk management strategies. This might include securing supply contracts, implementing hedging strategies, or diversifying sources of supply to mitigate the impact of price volatility and supply disruptions.

The fundamentals of project risk management encompass a systematic approach to identifying, assessing, and mitigating potential threats that could impede project success. At its core, this discipline involves recognising uncertainties that may arise throughout the project lifecycle and implementing proactive measures to address them.

- Consumer Behavior and Purchasing Patterns:

- Price Sensitivity: Consumers’ purchasing decisions are influenced by changes in prices. When prices rise, consumers may seek substitutes, reduce consumption, or postpone purchases. Conversely, lower prices can lead to increased spending and a shift in consumption patterns.

- Consumption Choices: Fluctuations in supply and demand can alter consumer preferences and choices. For instance, if a product becomes scarce or expensive, consumers may switch to alternative products or brands that offer better value.

- Budgeting and Planning: Consumers often adjust their budgets and spending habits in response to price changes and market conditions. This adjustment can affect overall spending patterns and impact demand for various goods and services.

Implementing advanced budgeting techniques is crucial for businesses seeking heightened financial control, strategic planning, and adaptability in today's dynamic business environment. These advanced techniques go beyond traditional budgeting approaches, incorporating sophisticated methodologies to enhance precision and effectiveness. Zero-based budgeting, which requires

- Long-term Expectations: Anticipated future price changes and market trends can influence current consumer behavior. For example, if consumers expect prices to rise, they might increase current purchases to avoid higher future costs.

Understanding these implications enables businesses to make informed strategic decisions and helps consumers navigate market changes effectively, ensuring both parties can adapt to shifting economic conditions and optimize their outcomes.

Conclusion

In summary, the dynamics of demand and supply are central to understanding how markets operate, influencing prices, production, and consumption patterns. The interaction between these forces shapes market equilibrium, and shifts in demand or supply can lead to significant economic changes. Looking ahead, factors such as technological advancements, global economic shifts, and evolving consumer preferences will continue to impact demand and supply, necessitating adaptive strategies from both businesses and policymakers to navigate future market trends effectively.