- Table of Contents

- Introduction

- What is Supply?

- Definition of Supply

- The Law of Supply

- Determinants of Supply

- What is Demand?

- Definition of Demand

- The Law of Demand

- Determinants of Demand

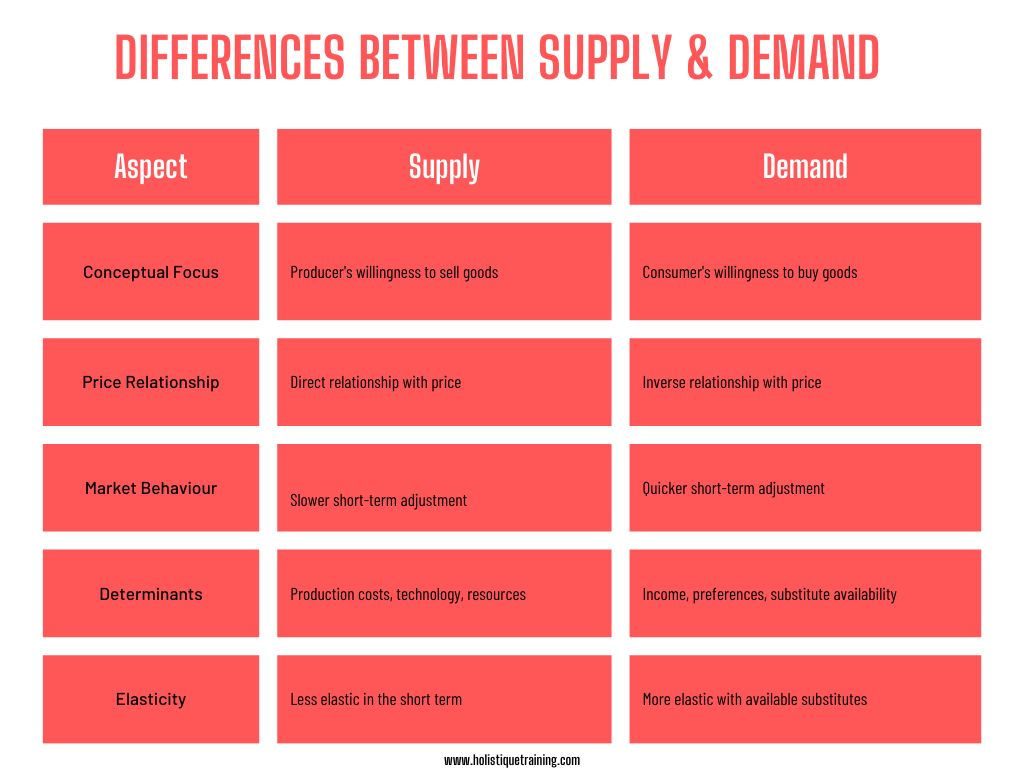

- 10 Key Differences Between Supply and Demand

- Conceptual Focus

- Relationship with Price

- Market Behaviour

- Determinants

- Elasticity

- Time Horizon

- Market Perspective

- Impact on Revenue

- Role in Economic Policy

- Implications for Market Structure

- How Demand vs. Supply Affects the Economy

- Price Determination

- Resource Allocation

- Employment Levels

- Economic Growth

- Inflation and Deflation

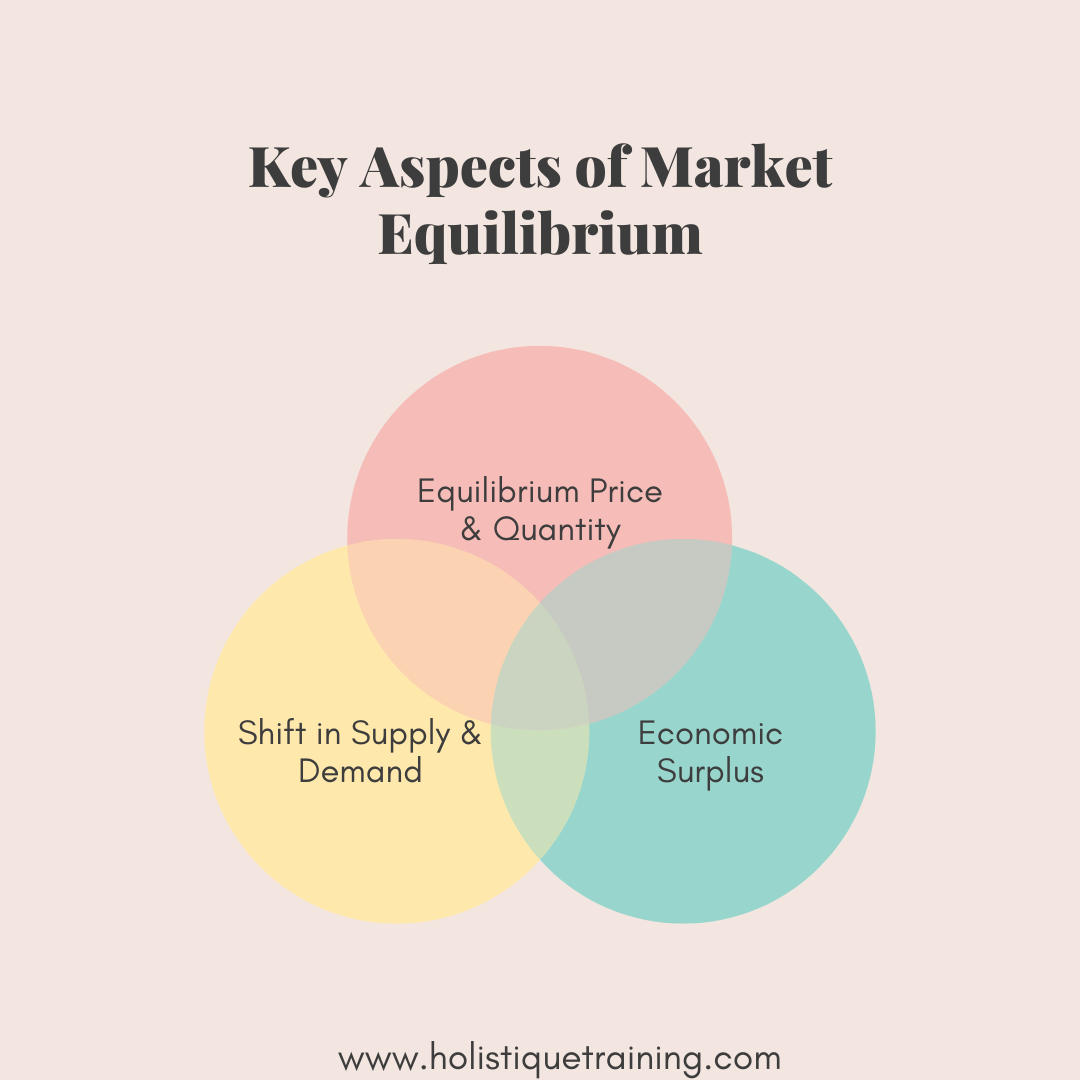

- Market Equilibrium and Its Key Aspects

- Definition of Market Equilibrium

- Equilibrium Price and Quantity

- Shifts in Supply and Demand

- Economic Surplus

- The Impact of Changes in Supply and Demand on Market Equilibrium

- Changes in Demand

- Changes in Supply

- Simultaneous Shifts in Supply and Demand

- The Role of Elasticity in Demand and Supply

- Understanding Elasticity

- Price Elasticity of Demand

- Price Elasticity of Supply

- Impact of Elasticity on Market Equilibrium

- Elasticity and Revenue

- Conclusion

Introduction

Navigating the complex world of economics often begins with understanding the fundamental concepts of supply and demand. These two forces serve as the backbone of market economies, shaping everything from the prices we pay for goods and services to allocating resources across industries. While they are often discussed together, supply and demand each have distinct roles and characteristics that uniquely influence market dynamics. Understanding their differences is crucial for anyone looking to grasp how markets function, whether you’re a business owner, policymaker, or consumer. This blog post delves into the key distinctions between supply and demand, exploring how their interaction drives market equilibrium, impacts the economy, and determines the direction of price movements. By the end, you’ll have a clearer picture of how these economic forces operate and why they are vital to decision-making in business and daily life.

What is Supply?

Definition of Supply

Supply, at its core, refers to the quantity of a good or service that producers can offer for sale at various price points within a given period. It reflects the seller's perspective in the marketplace, highlighting the relationship between the price of a good and the amount producers are prepared to sell. The fundamental principle behind supply is that the quantity supplied typically increases as prices rise, incentivising producers to produce and sell more.

The Law of Supply

The law of supply states that all else being equal, there is a direct relationship between the price of a good and the quantity supplied. When prices increase, suppliers are more willing to produce more of that good because higher prices can lead to higher revenues and profits. Conversely, when prices fall, the incentive to supply diminishes, leading to a reduction in the quantity offered in the market.

For example, if wheat prices increase significantly, farmers are more likely to plant more wheat to take advantage of the higher prices. However, if the price drops, they may switch to other crops with better profitability.

Determinants of Supply

Several factors influence the supply of a good or service beyond just price. These determinants include:

- Production Costs: The costs of inputs such as labour, raw materials, and technology directly impact supply. If production costs increase, supply may decrease as the goods become less profitable.

- Technological Advancements: Improvements in technology can lead to more efficient production processes, increasing supply by allowing producers to create more goods at a lower cost.

- Number of Sellers: An increase in the number of sellers in the market generally leads to an increase in supply, as more producers contribute to the total quantity of the goods available.

- Government Policies: Taxes, subsidies, and regulations can all affect supply. For instance, a subsidy may encourage more production, while a tax could have the opposite effect.

- Expectations of Future Prices: If producers expect prices to rise, they may hold back some of their current supply to sell later at a higher price, reducing the current supply.

- Natural Conditions: For agricultural products, weather conditions and natural disasters significantly determine supply. Good weather can lead to bumper crops, while droughts or floods can severely reduce supply.

What is Demand?

Definition of Demand

Demand refers to the quantity of a good or service that consumers are willing and able to purchase at various prices over a certain period of time. It represents the buyer's side of the market, emphasising how much of a product people want based on its price. The general assumption is that as the price of a good decreases, the quantity demanded increases, making it more affordable for consumers.

The Law of Demand

The law of demand posits an inverse relationship between price and quantity demanded. As the price of a good or service falls, the quantity demanded tends to rise, and as the price increases, the quantity demanded typically falls. This principle reflects basic consumer behaviour, where lower prices make goods more accessible to more people, while higher prices restrict access, reducing the quantity purchased.

For example, if the price of smartphones decreases significantly, more people will likely purchase them, increasing the overall demand. Conversely, if prices increase, fewer people may be able to afford them, leading to a decrease in demand.

Determinants of Demand

Demand is influenced by various factors, known as determinants of demand, including:

- Income Levels: As consumers’ incomes rise, they generally demand more goods and services. Conversely, a drop in income can lead to reduced demand, especially for non-essential goods.

- Consumer Preferences: Changes in tastes, fashion, and consumer preferences can significantly impact demand. A new trend or popular product can see a surge in demand, while outdated or less popular goods see a decline.

- Price of Related Goods: The demand for a good can be affected by the price of related goods. For instance, if the price of a substitute good rises, the demand for the original good may increase as consumers switch to the cheaper alternative. Similarly, a decrease in the cost of complementary goods can boost demand.

- Expectations of Future Prices: If consumers expect prices to rise, they may increase their current demand to avoid paying more later. On the other hand, if they expect prices to drop, they might hold off on purchasing, reducing current demand.

- Population Size and Demographics: A larger population generally leads to higher demand for goods and services. Additionally, demographic changes, such as an ageing population, can shift demand patterns for certain products.

- Seasonal Factors: Some goods have seasonal demand. For example, demand for winter clothing increases during the colder months and drops in the summer.

Distribution logistics focuses on efficiently distributing and delivering finished products. It links production to the market and contributes to high customer service standards. This course provides you with a comprehensive look at the fundamentals of distribution logistics. You will learn about

10 Key Differences Between Supply and Demand

Understanding the key differences between supply and demand is essential to grasp how markets operate. While they are often discussed together, each concept has unique characteristics and implications. Below is a detailed explanation of these differences:

Conceptual Focus

Supply and demand, though interrelated, focus on different aspects of the market. Supply is centred around the producer's side of the market equation. It reflects the quantity of a good or service that producers can sell at various price levels over a specific period. This concept is rooted in the production process, considering production costs, technology, and resource availability. On the other hand, demand represents the consumer's perspective. It focuses on the quantity of a good or service that consumers are willing and able to purchase at different prices. Demand is influenced by factors such as consumer preferences, income levels, and the availability of substitutes. While supply emphasises the producer’s capacity and willingness to produce, demand highlights consumer desires and purchasing power.

Relationship with Price

The relationship between price and quantity differs significantly between supply and demand. Supply typically directly relates to price, which is encapsulated in the law of supply. As prices increase, producers are generally more inclined to supply more of a good or service, as higher prices can lead to higher revenue and profitability. Conversely, when prices decrease, producers may reduce their output. Demand, however, exhibits an inverse relationship with price, as outlined by the law of demand. Consumers tend to purchase less of a good or service as prices rise because the higher cost reduces the perceived value or affordability. Conversely, consumers are more likely to increase their purchases when prices drop. This fundamental difference in how supply and demand respond to price changes is crucial for understanding market dynamics and price formation.

Market Behaviour

The behaviour of supply and demand in the market also differs. Supply tends to be more rigid in the short term due to factors like production capacity, resource availability, and time lags in adjusting output. Producers cannot always quickly increase or decrease production in response to price changes, leading to short-term inelasticity. Over the long term, however, supply can become more elastic as producers adjust their operations. On the other hand, demand can be more flexible and responsive in the short term, especially for non-essential goods. Consumers can quickly change their purchasing behaviour in response to price changes, preferences, or income shifts. This difference in market behaviour means supply adjustments often take longer, whereas demand can fluctuate more readily.

Determinants

The factors that determine supply and demand differ significantly. Supply is influenced by factors such as production technology, input prices, the number of producers, and government regulations or subsidies. These factors impact the ability and cost of producing goods or services. Technological improvements, for instance, can increase supply as production becomes more efficient. Demand is shaped by factors like consumer income, tastes and preferences, prices of related goods (substitutes and complements), and future expectations. For example, an increase in consumer income generally leads to higher demand for goods and services, especially for normal goods. These determinants reflect the different influences that shape the quantity supplied or demanded in the market.

Elasticity

Elasticity measures how responsive supply and demand are to changes in price. Supply elasticity refers to how much the quantity supplied of goods changes in response to a change in price. Supply tends to be more elastic in the long run as producers have time to adjust production levels, expand capacity, or enter new markets. However, supply is often inelastic in the short run due to fixed production capacity and time constraints. Demand elasticity, or price elasticity of demand, indicates how much the quantity demanded changes in response to price changes. Demand tends to be more elastic when there are readily available substitutes or when the good is non-essential. For example, luxury items usually have more elastic demand because consumers can easily forgo these purchases if prices rise. The concept of elasticity is crucial for understanding how price changes affect market supply and demand.

Time Horizon

The time horizon plays a different role in supply and demand. Supply often requires a longer time to adjust, particularly in industries that involve complex production processes or significant capital investments. For instance, increasing the supply of manufactured goods may require building new factories or purchasing additional equipment, which can take time. On the other hand, demand can change rapidly, especially in response to short-term factors like seasonal trends, marketing campaigns, or sudden changes in consumer preferences. The time horizon affects how quickly each side of the market can respond to changes, with demand often being more immediate and supply taking longer to catch up.

Market Perspective

From a market perspective, supply is typically viewed through the lens of producers and sellers, focusing on how they can meet market needs efficiently and profitably. Producers consider factors like production costs, competition, and market entry barriers when deciding on the quantity of goods to supply. Demand is viewed from the consumer's perspective, with a focus on maximising utility or satisfaction from goods and services. Consumers consider factors like price, quality, and personal preference when deciding how much of a product to purchase. This difference in perspective highlights the distinct roles that supply and demand play in the market, with supply driven by production considerations and demand driven by consumption needs.

Impact on Revenue

The impact of supply and demand on revenue generation differs between producers and consumers. Supply is directly tied to the revenue of producers; as they increase the quantity supplied at higher prices, their revenue can increase, assuming demand remains steady. However, if supply increases too much, leading to a surplus, prices might drop, potentially reducing revenue. Demand, while not directly tied to consumer revenue, impacts producers' revenue indirectly. Higher demand at a given price point can lead to higher revenue for producers as they sell more goods. However, if demand decreases, producers may face reduced revenue, significantly if they cannot lower production costs proportionately. Supply, demand, and revenue interplay is central to understanding market outcomes.

Role in Economic Policy

Supply and demand also play different roles in economic policy. Supply-side policies often focus on increasing production capacity and efficiency, such as through tax incentives for businesses, investments in infrastructure, or deregulation. These policies aim to boost supply, lower costs, and encourage economic growth. On the other hand, demand-side policies aim to increase consumer spending and overall economic demand. This can be achieved through fiscal policies like tax cuts for consumers, increased government spending, or monetary policies that lower interest rates. Understanding these differences helps policymakers design strategies targeting specific economic issues, whether to stimulate production or boost consumption.

Implications for Market Structure

Finally, supply and demand have different implications for market structure. Supply can influence market structure by determining the level of competition, market entry barriers, and the concentration of producers. For instance, in industries where a few large producers dominate supply, the market may lean towards oligopoly or monopoly, affecting pricing power and market dynamics. On the other hand, demand influences market structure by shaping consumer preferences and the variety of available goods. High consumer demand for diverse products can lead to more competitive markets with numerous suppliers offering different options. Conversely, low demand might result in a more concentrated market with fewer suppliers. These implications highlight the broader impact that supply and demand have on how markets are structured and how competition evolves.

By thoroughly understanding these ten key differences, one can better appreciate the intricate relationship between supply and demand and their combined economic effects.

Boost your supply chain skills with key strategies in communication, negotiation, and execution to excel in today’s fast-changing marketplace.

How Demand vs. Supply Affects the Economy

The interplay between supply and demand is fundamental to the functioning of economies. These forces determine not only the prices of goods and services but also the allocation of resources, the level of employment, and overall economic growth.

Price Determination

Supply and demand interact to determine the price of goods and services in a market. When demand exceeds supply, prices tend to rise, signalling producers to increase production. Conversely, prices fall when supply exceeds demand, signalling producers to reduce output. This price mechanism helps allocate resources efficiently, ensuring that goods and services are produced where they are most valued.

Resource Allocation

The forces of supply and demand also play a crucial role in resource allocation. Resources are limited, and the market allocates price signals to their most efficient uses. For instance, if the demand for electric vehicles rises, resources will be allocated to producing batteries, electric motors, and related technologies, reflecting the market’s shift toward sustainable transportation.

Employment Levels

Changes in demand and supply can have a significant impact on employment levels. An increase in demand for a particular good can lead to higher production, requiring more labour and thus increasing employment. On the other hand, if demand falls or supply exceeds demand, firms may reduce their workforce to cut costs, leading to unemployment.

Economic Growth

The balance between supply and demand also affects overall economic growth. A strong demand for goods and services encourages businesses to invest in new technologies, expand production, and hire more workers, all contributing to economic growth. However, if supply cannot keep up with demand, it can lead to inflation, which may slow economic growth.

Inflation and Deflation

Demand consistently exceeds supply, which can lead to inflation, where the general price level of goods and services rises. Inflation erodes purchasing power and can adversely affect the economy, such as reduced consumer spending and increased uncertainty. Conversely, if supply consistently exceeds demand, it can lead to deflation, where prices fall, potentially leading to reduced economic activity and increased unemployment.

Supply chain professionals continuously confront the challenge of improving service levels and simultaneously reducing costs to produce desired business outcomes. Cost reduction efforts incur risk, which is magnified in global supply chains. This course provides strategies to avoid, mitigate, or divert

Market Equilibrium and Its Key Aspects

Definition of Market Equilibrium

Market equilibrium occurs when the quantity supplied equals the quantity demanded at a particular price level. At this point, the market is in a state of balance, with no inherent tendency for prices to change. The equilibrium price is where the supply and demand curves intersect on a graph, representing the price at which producers are willing to sell and consumers are willing to buy.

Equilibrium Price and Quantity

The equilibrium price is when the quantity of goods supplied equals the amount demanded. There is no shortage or surplus in the market at this price, and the quantity exchanged is at its highest efficiency. The equilibrium quantity is the goods bought and sold at the equilibrium price.

Shifts in Supply and Demand

Market equilibrium is dynamic and can change when the supply or demand curve shifts. For example, if there is an increase in demand due to a rise in consumer income, the demand curve shifts to the right, leading to a higher equilibrium price and quantity. Conversely, if there is an improvement in production technology, the supply curve shifts to the right, lowering the equilibrium price and increasing the quantity.

Economic Surplus

At market equilibrium, the total economic surplus—comprising consumer surplus and producer surplus—is maximised. Consumer surplus is the difference between what consumers are willing to pay and what they actually pay. In contrast, producer surplus is the difference between what producers receive and their minimum acceptable price. Market equilibrium ensures that resources are allocated efficiently, maximising the benefits to both consumers and producers.

Explore Supply Chain Management—from standards to sustainability and responsible practices—shaping the future of global supply chains.

The Impact of Changes in Supply and Demand on Market Equilibrium

Changes in Demand

When demand increases, perhaps due to a rise in consumer income or a change in preferences, the demand curve shifts to the right. This shift results in a new equilibrium with a higher price and quantity. Producers respond to higher prices by increasing production, which meets the new level of demand. Conversely, a decrease in demand shifts the curve to the left, resulting in a lower equilibrium price and quantity.

For example, demand for certain products like toys and electronics typically increases during the holiday season. Retailers may raise prices in response, leading to a new higher equilibrium price. After the season, when demand falls, prices may drop back down to reflect the lower equilibrium.

Changes in Supply

Changes in supply, such as technological improvements or production costs, shift the supply curve. An increase in supply shifts the curve to the right, leading to a lower equilibrium price and higher quantity. Conversely, a decrease in supply shifts the curve to the left, resulting in a higher equilibrium price and lower quantity.

For instance, if a new technology makes it cheaper to produce smartphones, the supply curve for smartphones shifts to the right. This shift leads to a lower price for smartphones and a higher quantity sold in the market. If production costs rise, such as due to an increase in the price of raw materials, the supply curve shifts left, resulting in higher prices and lower quantities.

Simultaneous Shifts in Supply and Demand

In some cases, both supply and demand may shift simultaneously, leading to complex changes in equilibrium. For example, if there is an increase in demand for electric vehicles due to environmental concerns and a simultaneous improvement in battery technology, both the supply and demand curves will shift. The new equilibrium will depend on the relative magnitude of these shifts.

If the demand increase is larger than the supply increase, the equilibrium price and quantity will rise. If the supply increase exceeds the demand increase, the equilibrium price may fall while the quantity increases.

Metric | Supply Measurement | Demand Measurement |

Quantity | Units produced or available to sell | Units purchased or desired by consumers |

Price | Selling price set by producers | Purchase price consumers are willing to pay |

Elasticity | Responsiveness to price changes | Responsiveness to price changes |

Revenue | Total income from goods sold | Total expenditure by consumers |

Market Share | Producer’s share of total supply | Consumer’s share of total demand |

Table: Metrics to measure supply and demand

The Role of Elasticity in Demand and Supply

Understanding Elasticity

Elasticity measures how responsive the quantity demanded or supplied is to changes in price. Elasticity is crucial for understanding how price changes will impact the overall market, affecting both consumer behaviour and production decisions.

Price Elasticity of Demand

Price elasticity of demand (PED) refers to the responsiveness of the quantity demanded to a change in price. If demand is elastic, a small change in price leads to a significant change in the quantity demanded. Conversely, if demand is inelastic, quantity demanded changes little with price fluctuations.

For example, luxury goods often have elastic demand, meaning a small increase in price can lead to a large drop in demand. On the other hand, essential goods like insulin have inelastic demand, where even significant price changes have little effect on the quantity demanded.

Price Elasticity of Supply

Price elasticity of supply (PES) measures the responsiveness of the quantity supplied to a change in price. Producers can quickly increase supply in response to price changes if supply is elastic. If supply is inelastic, production is less responsive to price changes.

For example, agricultural products may have an inelastic supply in the short term because it takes time to grow crops. However, supply may become more elastic in the long term as producers adjust their production processes.

Impact of Elasticity on Market Equilibrium

Elasticity plays a crucial role in determining how changes in supply and demand affect market equilibrium. In markets with elastic demand, price changes can lead to significant shifts in quantity demanded, affecting equilibrium prices and quantities more dramatically. In markets with inelastic demand, price changes have a smaller impact on equilibrium quantities but can lead to significant changes in total revenue for producers.

For example, in the oil market, where both supply and demand are relatively inelastic, small changes in supply can lead to significant price fluctuations. A supply disruption can cause prices to spike, as demand does not decrease significantly in response to higher prices.

Elasticity and Revenue

For producers, understanding elasticity is crucial for pricing decisions. If demand is elastic, lowering prices can increase total revenue by attracting more buyers. Conversely, if demand is inelastic, raising prices can increase revenue, as the quantity demanded will not drop significantly.

Similarly, understanding the elasticity of supply helps producers anticipate how changes in production costs or market prices will affect their ability to supply goods and services.

Conclusion

The concepts of supply and demand are foundational to understanding economic principles and market dynamics. These forces determine prices and influence how resources are allocated across various sectors, ultimately driving economic growth and development. The interaction between supply and demand is what leads to market equilibrium, the critical point where the quantity supplied meets the quantity demanded, ensuring that markets function efficiently. However, this balance is delicate; even minor changes in supply and demand, coupled with the elasticity of these forces, can lead to significant market outcomes, ranging from price fluctuations to shifts in employment and resource distribution. Grasping these dynamics is essential for businesses, policymakers, and consumers alike, enabling them to navigate the complexities of an ever-changing economic landscape with greater confidence and foresight.

To further deepen your understanding of these critical economic concepts and learn how to apply them in real-world business scenarios, consider enrolling in our course "S&OP: Sales & Operational Planning." This course provides comprehensive insights into integrating sales and operations planning to optimise supply chain efficiency and drive strategic business growth.

Sales and Operation Planning (S&OP) is an integrated process for balancing supply and demand. It aligns multiple operational areas of an organisation to meet financial and organisational goals. In addition to supporting cross-functional activities, S&OP is a key communication tool that presents a unified plan