- Table of Contents

- Introduction

- 1. The Entrepreneurial Mindset

- 2. Identifying Your Entrepreneurial Idea

- 3. Validating Your Idea Before You Build

- 4. Building a Business Plan

- 5. Choosing the Right Legal Structure

- 6. Securing Funding for Your Venture

- 7. The Key Stages of the Entrepreneurial Journey

- 8. Building and Leading Your Team

- 9. Launching Your Business

- 10. Scaling Your Business for Growth

- 11. Managing Risk and Building Resilience

- 12. The Power of Mentorship and Networking

- 13. Digital Tools and Technologies for Modern Entrepreneurs

- 14. Common Mistakes Every Entrepreneur Should Avoid

- 15. The Future of Entrepreneurship

- Conclusion

Introduction

Every great company began with a person who refused to accept the world exactly as it was. Entrepreneurship is not simply about building a business — it is about having the courage to see opportunity where others see obstacles, and the resilience to keep going when the path grows uncertain. From the technology giants of Silicon Valley to the social enterprises transforming communities in sub-Saharan Africa, entrepreneurs share one defining quality: they act. They turn vision into reality, and in doing so, they create jobs, drive innovation, and shape the future.

Whether you are a recent graduate wondering what to do with your ambition, a mid-career professional dreaming of something more meaningful, or an experienced executive looking to build something entirely your own, the entrepreneurial path is open to you. This guide covers everything you need to know: what entrepreneurship truly means, how to identify and validate an idea, how to plan and fund your venture, and how to build a business that can grow, adapt, and endure. It also addresses the mindset shifts, practical skills, and common pitfalls that determine whether a new business thrives or fades.

In this article, we will discuss the entrepreneurial mindset, identifying your idea, validating the market, building a business plan, choosing a legal structure, securing funding, building a team, launching your business, scaling for growth, managing risk, the role of mentorship and networking, digital tools for modern entrepreneurs, common mistakes to avoid, and the future of entrepreneurship.

1. The Entrepreneurial Mindset

Before any business plan is written or any product is built, entrepreneurship begins in the mind. The way you think about failure, risk, uncertainty, and opportunity will determine more about your eventual success than any single strategic decision. Entrepreneurs do not simply think differently about business — they think differently about life. They see setbacks as data, failure as feedback, and competition as a signal that a market exists.

The most important quality is not intelligence or creativity, though both help. It is what psychologist Carol Dweck calls a growth mindset: the belief that abilities can be developed through effort, learning, and persistence. Entrepreneurs with a growth mindset do not collapse when things go wrong. They ask what they can learn and what they can change. This orientation towards continuous improvement is, in practice, the defining psychological trait of people who build durable businesses.

Resilience sits alongside growth mindset as an essential quality. Entrepreneurship is not a smooth upward line. It is a series of peaks and valleys, pivots and corrections. The founders who succeed are rarely those with the best ideas at the outset. They are those who stayed committed to solving a real problem even as their original approach required revision. Resilience is not the absence of doubt or fear; it is the decision to keep moving despite them.

Alongside mindset, self-awareness matters enormously. The most effective entrepreneurs understand their own strengths and, crucially, their blind spots. They build teams and partnerships that complement their own capabilities. They seek feedback actively and are not defensive about criticism. This willingness to be wrong in the short term in service of being right over time is one of the clearest indicators of entrepreneurial potential.

2. Identifying Your Entrepreneurial Idea

The mythology of entrepreneurship often suggests that great ideas arrive as sudden flashes of inspiration. In reality, most successful businesses were built on patient observation, genuine frustration, or a deep understanding of a specific community or market. The best ideas solve real problems for real people — and the founders of those businesses often had a personal connection to the problem they were solving.

Start by looking at your own life. Where do you feel friction? What tasks take longer than they should? What products or services do you use that feel incomplete or overpriced? Personal frustration is one of the most reliable generators of business ideas, because the problem is immediately real to you and you are likely not alone in experiencing it. Many of the world's most successful consumer businesses were built by founders solving problems they had encountered themselves.

Look beyond your personal experience too. Spend time in communities, industries, and markets that interest you. Talk to people. Listen to complaints. Read industry reports. Pay attention to trends: what is changing in technology, demographics, regulation, or culture? Every major shift creates new needs, and where there are unmet needs, there are business opportunities. The circular economy, artificial intelligence, ageing populations, climate adaptation, and remote work are all generating significant entrepreneurial opportunities right now.

Once you have an idea, write it down clearly. A good business idea can usually be expressed in one or two sentences: who has a problem, what the problem is, and how your solution addresses it better than existing alternatives. If you cannot articulate that clearly, the idea may not yet be ready for the next stage.

3. Validating Your Idea Before You Build

One of the most costly mistakes an entrepreneur can make is investing significant time and money into a product or service before confirming that anyone actually wants it. According to CB Insights' analysis of startup post-mortems, the single most common reason startups fail is a lack of market need, accounting for approximately 42% of all closures. Validation is the process of testing your assumptions about the market before making large commitments.

Validation does not require a finished product. It requires honesty and curiosity. Speak to potential customers — not to pitch them, but to understand them. Ask open questions about how they currently solve the problem, what they find unsatisfying about existing solutions, and what they would be willing to pay for something better. If people engage enthusiastically and start asking when your product will be available, that is a strong signal. If they politely change the subject, that is equally important information.

Build a minimum viable product as soon as you can. This is not a polished, feature-rich product. It is the simplest version that allows real users to experience the core value of your solution. Early-stage platforms, landing pages, prototypes, or even manual workarounds can all serve as MVPs. The purpose is to generate real user behaviour data rather than relying on hypothetical surveys or assumptions.

Track what people actually do, not just what they say. Users may tell you they love your idea but fail to sign up when the product is available. Conversion rates, time spent, repeat usage, and willingness to pay are all more reliable indicators of product-market fit than verbal enthusiasm alone. Treat every interaction as a learning opportunity, and be prepared to adjust your idea significantly based on what you discover.

Venture into entrepreneurship's realm of opportunity and transformation. This guide escorts you through the process of constructing your business, from self-assessment to market entry, all while investigating the impact of degrees in the contemporary entrepreneurial arena.

4. Building a Business Plan

A business plan is not a formality for investors. It is a thinking tool for founders. The process of writing a business plan forces you to confront uncomfortable questions, make explicit the assumptions underlying your strategy, and identify the gaps in your knowledge. Businesses that operate with a clear plan consistently outperform those that do not, because planning builds discipline and creates a shared framework for decision-making.

A strong business plan covers several key areas. The executive summary provides a concise overview of the opportunity and your approach. The market analysis demonstrates that you understand the competitive landscape, the size of the addressable market, and the characteristics of your target customer. The product or service description explains what you are selling and why it is better than alternatives. The operational plan covers how you will deliver your offering at scale. The financial plan includes projected revenue, costs, cash flow, and the assumptions underlying those projections.

Be honest in your financial projections. Over-optimistic forecasts are among the most common weaknesses in early business plans and a frequent source of tension with investors. Ground your numbers in evidence: comparable businesses, industry benchmarks, customer willingness-to-pay data from your validation work. Show multiple scenarios — best case, base case, and a conservative case — so that readers and reviewers can assess how robust your model is under different conditions.

A business plan is also a living document. Update it as you learn more, as the market shifts, and as your assumptions are tested by reality. The discipline of regular review — monthly or quarterly — creates accountability and helps you identify when strategic course corrections are needed before small problems become large ones.

The Chartered Management Institute acknowledges that it’s essential for businesses to accurately represent their finances against a business plan that’s been tested for feasibility. This includes considering budgets against key aims and objectives, resourcing requirements, and systems implementation. A business plan needs to have a solid footing

The Chief Executive Officer (CEO) Leadership Program is an intensive and comprehensive course designed for aspiring and current CEOs who aim to enhance their leadership skills and drive organisational success. This program provides participants with the tools, frameworks, and strategies needed to lead complex organisations

5. Choosing the Right Legal Structure

The legal structure of your business has significant implications for liability, taxation, fundraising capacity, and operational flexibility. Choosing the wrong structure early on can create complications that are expensive and time-consuming to correct later. While the specific options available to you depend on the country in which you are operating, the fundamental choice between sole trader, partnership, limited liability company, and corporation applies across most jurisdictions.

Structure | Liability | Taxation | Best For |

Sole Trader / Sole Proprietor | Unlimited personal liability | Personal income tax | Early-stage, low-risk freelancers |

Partnership | Shared liability between partners | Pass-through taxation | Co-founder ventures without external funding |

Limited Liability Company (LLC) | Limited to investment | Flexible — can pass-through or corporate | Most small to medium businesses |

Private Limited Company (Ltd / Inc) | Limited to shares owned | Corporate tax rates | Scalable ventures seeking investment |

Public Limited Company (PLC) | Limited to shares | Corporate tax; shareholder obligations | Large-scale enterprises or IPO candidates |

For most early-stage entrepreneurs, a limited liability company or its local equivalent offers the best combination of personal liability protection and operational simplicity. If you are planning to raise external equity investment, however, investors will typically require a corporate structure that allows for the issuance of shares, preference rights, and convertible instruments. Seek legal advice early; the cost of an hour with a commercial solicitor is negligible compared to the cost of restructuring a business later.

6. Securing Funding for Your Venture

Access to capital is one of the most practical challenges every entrepreneur faces. The funding landscape is more diverse than ever, which means there are real options for founders at every stage and in every sector — but each option carries different implications for control, dilution, and expectation.

Bootstrapping — funding your business from personal savings and early revenue — is the most common starting point. It preserves complete ownership and forces early discipline about cost. Many highly successful businesses were built entirely on bootstrapped capital. The constraint is growth speed: without external investment, scaling requires that your business generate sufficient profit to fund its own expansion.

Angel investors are high-net-worth individuals who invest personal capital into early-stage businesses, typically in exchange for equity. They often bring valuable experience and networks alongside their investment. Venture capital firms invest pooled funds from institutional investors into high-growth startups, usually at later stages than angels. According to data compiled by Embroker, only 0.05% of startups ever receive venture capital funding — the vast majority of businesses are funded through personal savings, loans, and the businesses' own revenue.

Crowdfunding platforms allow entrepreneurs to raise capital from large numbers of individual backers, either as donations, pre-orders, or equity. Government grants, development finance institutions, and innovation funds are available in many countries for businesses operating in priority sectors such as clean technology, health, and export. Understanding which funding sources are appropriate for your specific business model, growth trajectory, and geographic context is an important early exercise.

Explore startup entrepreneurship—its drivers, benefits, and challenges. Uncover what fuels ambition and shapes the journey of new business founders.

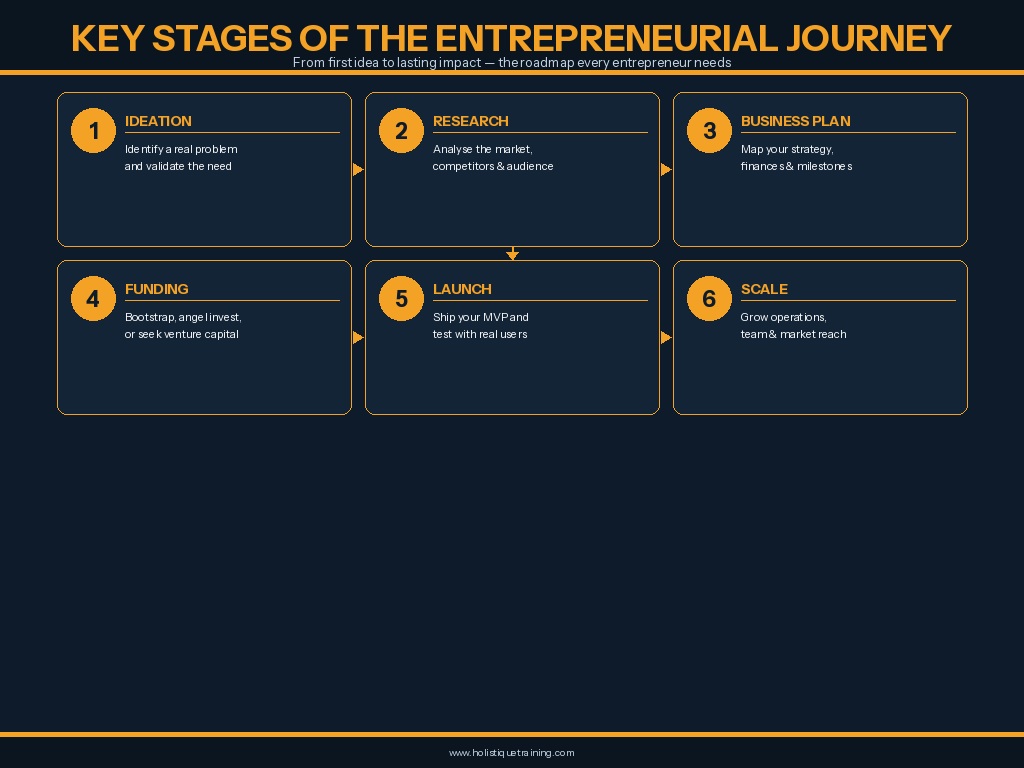

7. The Key Stages of the Entrepreneurial Journey

Entrepreneurship follows a recognisable arc — from the first spark of an idea to the establishment of a scaled and sustainable enterprise. Understanding where you are in that journey helps you make better decisions, set appropriate expectations, and seek the right kind of support at each stage. The infographic below illustrates the six core stages that most entrepreneurial journeys move through.

The ideation stage is where you crystallise the problem you are solving and the population you are serving. Research follows: deep market analysis, competitive intelligence, and customer discovery. A structured business plan converts that understanding into a strategic roadmap. Securing funding — whether bootstrapped or externally financed — gives you the resources to build. Launch involves getting your minimum viable product in front of real users and beginning to generate real data about how it performs. Scale is the phase where proven models are expanded: more customers, more markets, more revenue, with systems and teams capable of supporting that growth.

Not all businesses move through these stages in linear order, and some revisit earlier stages multiple times. A pivot — a structured change in product, market, or business model — is common and often necessary. The ability to recognise when a pivot is needed, and to execute it decisively, is one of the clearest markers of a capable entrepreneurial team.

8. Building and Leading Your Team

Very few great businesses are built by a single person. The quality of your team is arguably the single most important determinant of whether your venture succeeds, because everything else — your product, your strategy, your culture — is ultimately delivered by people. According to CB Insights' analysis of startup failures, team-related issues account for 23% of all shutdowns, making it the third most common cause of business failure after lack of market need and running out of cash.

In the earliest stages, your team may consist of a co-founder and a small group of generalists. Prioritise people who complement your own skills rather than replicate them. If you are a product builder, find someone who can sell. If you are commercially gifted, find someone with deep technical capability. The founding team sets the cultural template for everything that follows: the values you model in those early months will shape how the organisation behaves for years.

Hiring becomes increasingly complex as the business grows. Move from generalists to specialists as the demands of each function increase in sophistication. Be deliberate about culture: what behaviours are rewarded, how disagreements are resolved, what kind of psychological safety exists for people to raise concerns and propose ideas. Businesses that build strong cultures early find that talent retention, customer satisfaction, and innovation all improve as a direct consequence.

Stage | Team Priority | Key Hire |

Ideation | Co-founder alignment | Technical or commercial complement to founder |

Validation | Customer discovery | Sales or research lead |

Early Build | Product and operations | Engineer, designer, operations manager |

Launch | Growth and support | Marketing lead, customer success |

Scale | Functional leadership | Department heads (CFO, COO, CMO, etc.) |

9. Launching Your Business

The launch is a milestone, not a finish line. A good launch creates initial awareness, generates early customers, and produces the first wave of real-world feedback that will shape your product roadmap for months to come. A poor launch, however, does not necessarily mean the business is failing — it may simply mean that the initial positioning was off, the marketing channel was wrong, or the timing was suboptimal. Launch failures that are correctly diagnosed can be corrected quickly.

Before you launch, clarify your positioning. Who are you for, what do you do, and why are you better than the alternatives? Your positioning should be expressed consistently across your website, social media, sales materials, and customer conversations. Inconsistency confuses potential customers and dilutes the impact of your marketing spend.

Choose your launch channels deliberately. Digital marketing — search advertising, social media, content marketing, email — offers the ability to test messages and audiences cheaply before scaling what works. Earned media, partnerships, and communities can extend your reach without significant cost. If you are launching a B2B product, direct outreach and referrals are often more efficient than broad digital advertising in the early stages.

Set clear success metrics for the launch period. What does a successful first 30 days look like? How many users, sales, or sign-ups? What conversion rates are you targeting? Having explicit targets allows you to assess performance objectively rather than relying on gut feel, and it creates accountability for the decisions you make in response to early data.

10. Scaling Your Business for Growth

Scaling is often confused with growth. Growth means doing more of the same. Scaling means creating the systems, processes, and capabilities that allow the business to grow without a proportional increase in cost or complexity. A business that can acquire twice as many customers without twice as many staff or twice as much management attention is scaling. One that cannot is simply growing — and growth without scalability tends to break organisations.

The key to scaling is standardisation. As your business grows, document everything: customer onboarding, product delivery, financial reporting, team management, and decision-making processes. Standardised processes reduce errors, make training faster, and allow the business to grow with new people without losing quality or consistency. The companies that scale fastest are those that invest in operational infrastructure before they feel the urgent need for it.

Technology is a fundamental enabler of scale. Customer relationship management systems, enterprise resource planning software, marketing automation platforms, and data analytics tools all allow small teams to manage volumes of customers, transactions, and data that would have required large organisations a generation ago. The modern entrepreneur has access to technology at a cost that makes many previously unscalable business models entirely viable.

As you scale, revisit your business model regularly. What worked at ten customers may not work at a thousand. Pricing models, delivery mechanisms, support structures, and partnership strategies all need to evolve as the business grows. The founders who scale successfully tend to be those who remain as curious and adaptable at the growth stage as they were at the ideation stage.

Administrative professionals are essential to supporting an organisation's everyday operations. In addition to expertise in multitasking and meeting deadlines, you need to develop your interpersonal and management skills to contribute to the success of your team, your organisation, and yourself. This

11. Managing Risk and Building Resilience

Entrepreneurship is fundamentally an act of risk management. The entrepreneur does not eliminate risk — no one can — but identifies which risks to take deliberately, which to mitigate through planning, and which to transfer through insurance, contracts, or partnerships. Understanding the risk landscape of your specific business is an ongoing discipline, not a one-time exercise.

Financial risk is the most immediate for most early-stage businesses. Running out of cash is the second most common cause of startup failure, according to CB Insights. Maintaining a cash runway of at least six months — ideally twelve — gives you the time to respond to unexpected changes without being forced into desperate decisions. Monitor your burn rate weekly, maintain conservative revenue forecasts, and know your path to profitability well in advance of the point at which you will need to reach it.

Operational risk — the risk of things going wrong in the way you deliver your product or service — grows as the business scales. Building redundancy into critical systems, diversifying your supplier base, and ensuring that key knowledge is documented and distributed rather than held by a single individual are all essential risk management practices. Regulatory risk, reputational risk, and cybersecurity risk must also be assessed and managed as the business matures.

Resilience — the ability to absorb setbacks and recover quickly — is built through preparation, culture, and leadership. Entrepreneurs who model transparency and calm under pressure create organisations that can navigate adversity without losing momentum. The Global Entrepreneurship Monitor 2024/2025 report found that nearly half (49%) of respondents would not start a business due to fear of failure, up from 44% in 2019. Understanding risk clearly — and preparing for it systematically — is the most effective antidote to that fear.

12. The Power of Mentorship and Networking

No entrepreneur succeeds entirely alone. The businesses that grow fastest and survive longest are those whose founders actively seek out knowledge, relationships, and perspectives beyond their own experience. Mentorship and networking are not optional extras for the ambitious entrepreneur; they are strategic imperatives.

A good mentor — ideally someone who has built a business in a comparable sector or at a comparable stage — can save you from mistakes that would take months of painful experience to identify on your own. They offer pattern recognition that only comes from repeated exposure to entrepreneurial challenges. They can open doors to customers, investors, and talent. And they provide emotional support during the difficult periods that every entrepreneurial journey contains.

Networks compound over time. The relationship you build today with another founder, an investor, or a potential customer may not yield direct value for months or years. But when it does, the return can be enormous. Build your network deliberately and generously: share knowledge, make introductions, and support others without always expecting immediate reciprocation. Entrepreneurial communities that operate on reciprocity attract the most capable and collaborative participants.

13. Digital Tools and Technologies for Modern Entrepreneurs

The modern entrepreneur has access to a toolkit that would have seemed extraordinary a decade ago. Artificial intelligence, cloud computing, no-code platforms, and global logistics networks have removed many of the traditional barriers to starting and scaling a business. Understanding which tools can help you move faster, operate more efficiently, and compete more effectively is itself a competitive advantage.

For building and managing your product, tools like Notion, Figma, Webflow, and Bubble allow founders without extensive technical backgrounds to prototype, design, and even launch digital products. For customer relationship management, Salesforce, HubSpot, and Zoho provide powerful platforms that scale with your business. For financial management, accounting platforms like Xero and QuickBooks eliminate many of the manual processes that consumed founders' time in earlier eras.

Artificial intelligence is transforming what is possible for small teams. AI-powered writing, design, data analysis, customer service, and coding tools all allow solo founders and small teams to produce outputs that previously required much larger organisations. The entrepreneurs who will benefit most from AI are those who treat it as a genuine creative and operational partner, learning to prompt effectively and integrate it deeply into their workflows.

14. Common Mistakes Every Entrepreneur Should Avoid

The same patterns of failure appear with remarkable consistency across entrepreneurial ventures in every sector and geography. Understanding the most common mistakes gives you the opportunity to anticipate and avoid them, even if experience teaches the same lessons more vividly.

Common Mistake | Why It Happens | How to Avoid It |

Building without validating | Founder passion overrides market research | Talk to 50+ potential customers before building |

Scaling too early | Pressure to grow before foundations are solid | Confirm product-market fit before investing in growth |

Ignoring cash flow | Focus on revenue disguises burn rate problems | Monitor cash runway weekly, not monthly |

Hiring too fast | Growth excitement leads to premature team expansion | Hire for current need, not projected need |

Avoiding difficult conversations | Conflict aversion delays necessary pivots | Build a feedback culture from day one |

Underpricing | Fear of losing customers leads to unsustainable margins | Charge what the value justifies; test pricing early |

15. The Future of Entrepreneurship

Entrepreneurship is not a fixed activity. The nature of what it means to build a business is changing rapidly, shaped by technology, climate, demographic shifts, and evolving social expectations. The entrepreneurs who will thrive over the next decade are those who understand these forces and position their ventures to benefit from them.

Sustainability is moving from a niche concern to a mainstream business requirement. Consumers, investors, and regulators are all placing increasing emphasis on environmental and social performance. The entrepreneurs who integrate sustainability into their core business model — rather than treating it as an afterthought or marketing exercise — will find it a source of differentiation, resilience, and long-term competitive advantage.

The globalisation of talent and markets means that an entrepreneur in Lagos, Karachi, or Bogotá can build a product that competes globally from the first day of launch. Digital distribution, cloud infrastructure, and remote collaboration tools have dramatically reduced the geographic advantages that once made certain startup ecosystems dominant. The next generation of world-changing companies will be built in places that have not yet produced them.

Artificial intelligence will continue to reshape what entrepreneurship looks like at the team and operational level. Smaller teams will be able to accomplish more. The advantages of incumbency — data, distribution, brand recognition — will be challenged by AI-enabled newcomers who can match or exceed quality at a fraction of the cost. The entrepreneurial opportunity is enormous; the window to seize it is open.

Conclusion

Becoming an entrepreneur is one of the most demanding and one of the most rewarding choices a person can make. It requires clarity of purpose, intellectual honesty about the market, operational discipline, and the emotional resilience to persevere through uncertainty. It demands continuous learning, genuine curiosity about people and problems, and the courage to act before you have all the answers — because in entrepreneurship, you never will.

The good news is that none of the qualities required are fixed at birth. The growth mindset, the discipline of validation, the skills of financial management and team leadership — all of these can be learned, practised, and improved. The entrepreneurial journey is, at its core, a journey of personal development that happens to produce economic value as a by-product.

Start with a real problem. Talk to the people who experience it. Build the simplest possible solution and test it honestly. Plan carefully but hold your plan loosely. Build a team that complements your strengths and challenges your assumptions. And remember that the most important quality is not brilliance or luck — it is the willingness to begin.